Opportunities among emerging affluent investors

The individual annuity and retail retirement market centers on affluent investors who are retired or close to retirement. “Retirement investors” — workers and retirees aged 40 to 85 with at least $100,000 in household investable assets — control most of the nation’s wealth and make up the vast majority of individual annuity sales and individual retirement account rollovers.

While the financial services industry rightly concentrates on affluent retirement investors, another group warrants their attention. Emerging affluent investors are individuals aged 25-45 who are on track to become affluent later in their lives. They are not close to retirement, nor do they have enough wealth to qualify as “affluent,” yet they are critically important long-term prospects for the kinds of products and services the retirement industry offers. Moreover, each generation of Americans brings a distinctive perspective to financial issues based on their experiences during key life stages.

Future affluent investors may differ from current affluent investors in terms of outlook, preferences and priorities. By understanding emerging affluent investors now, financial professionals can build long-term relationships and trust, positioning themselves to help manage those investors wealth in the future.

Valued services

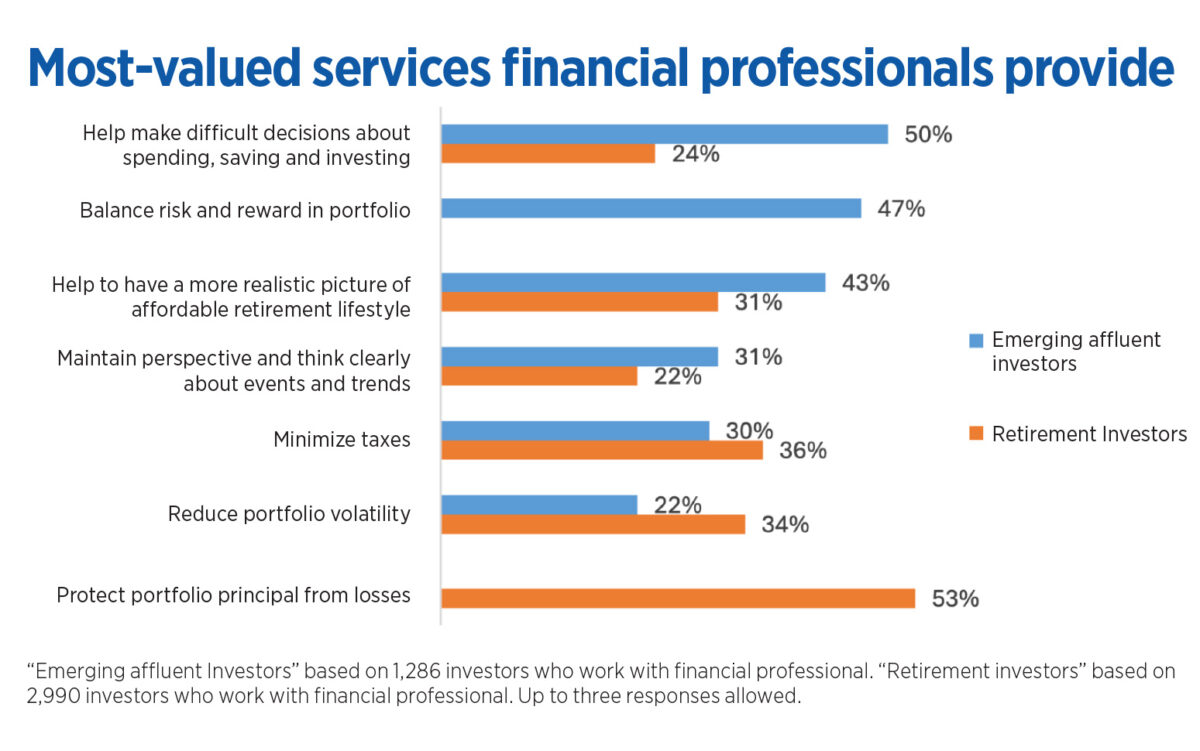

One of the ways that younger generations could be unlike their elders is in their reliance on financial professionals for help with household investment and financial decisions. For the most part, emerging affluent investor clients closely resemble retirement investor clients in terms of their reasons for working with a financial professional. Yet the two groups show significant differences in the value the place on the specific services that financial professionals provide to them.

Emerging affluent investors highly value fundamental services provided by their financial professional, such as offering guidance on difficult financial decisions and balancing risk and reward in their portfolios (see figure above). More specific services, such as those aimed at minimizing taxes or reducing portfolio volatility, were less commonly cited. Younger investors thus recognize they have less experience in selecting among financial choices or navigating tumultuous economic conditions, and they want their financial professional to offer their perspective and guidance even for basic decisions.

This pattern stands in contrast to the services most valued by retirement investors, who place relatively greater emphasis on principal protection and volatility reduction, as well as tax minimization. In addition, emerging affluent investors are more likely than their older counterparts to be discussing savings and debt reduction/elimination with their financial professional.

Long-term opportunities

Younger investors represent the future of the retirement industry. Establishing relationships with them early can yield long-term benefits for both clients and financial professionals. Our research shows that emerging affluent investors often look for professional guidance due to financial complexity, even before reaching common asset thresholds that have traditionally triggered advice seeking.

Providing financial education and services to younger people can help them make informed decisions, avoid debt and build a secure financial future. However, financial professionals cannot spend too much of their time educating clients about the basics of investments and financial decisions, and they need to be strategic about accommodating such demands given their time constraints and their firm’s business models. Finding the right balance between providing these highly valued services to their younger clients and time management will be critically important.

Social Security Fairness Act is an opportunity for professional advice

The opportunity in the Canadian life market

Advisor News

- Investors aren’t waiting out uncertainty

- Transamerica and Advo(k)ate Advisors launch pooled employer plan

- ‘I wish I’d met him sooner:’ Karlan Tucker remembered for integrity, faith

- Why women must be more engaged in investing

- SEC moves to simplify electronic delivery of investor communications

More Advisor NewsAnnuity News

- Immediate Care Plan: A new solution for funding LTC

- Delaware Life Launches a New Bonus Fixed Index Annuity Built for Growth, Protection, and Flexibility

- LIMRA: Annuity sales set new quarterly record with $123.9B in Q2

- CANNEX names Gary Baker as its new CEO

- Corebridge adds options to its Power Series of indexed annuities

More Annuity NewsHealth/Employee Benefits News

- EDITORIAL: Colorado's latest Medicaid pratfall

- Eight-Clinic Primary Care Group Leverages North Carolina's Health Information Exchange to Drive Down Medicare and Medicaid Costs

- EDITORIAL: Colorado’s latest Medicaid pratfall

- Immediate Care Plan: A new solution for funding LTC

- LTCi innovations that protect your client’s independence

More Health/Employee Benefits NewsLife Insurance News

- Trademark Application for “DIGITAL ADVISOR SUCCESS HUB” Filed by Jackson National Life Insurance Company: Jackson National Life Insurance Company

- AM Best Revises Issuer Credit Rating Outlook to Stable for Members of Tennessee Farmers Insurance Companies

- Unum Group Reports Second Quarter 2026 Results

- Delaware Life Launches a New Bonus Fixed Index Annuity Built for Growth, Protection, and Flexibility

- LIMRA predicts strong life and annuity sales for the rest of 2026

More Life Insurance News