How healthcare inflation can eat up a client’s retirement income

An Albert Einstein quote has morphed over time into “We will never be able to solve the problems of tomorrow with the thinking of today.”

This will resonate with financial professionals, since planning for the future requires moving beyond the here and now to imagine financial needs and challenges decades ahead. This is particularly important when thinking about healthcare costs in retirement.

Boston College’s Center for Retirement Research and HealthView Services both issued reports earlier this year showing healthcare expenses as a percentage of Social Security benefits.

The papers appeared to provide contradictory data. Boston College’s data showed that a 65-year-old couple would need 27% of their Social Security benefits to cover healthcare expenses in retirement. HealthView Service’s data showed that the same couple will require 84% of their Social Security benefits to cover their healthcare needs over their lifetimes.

The data highlights the difference between the relative costs of healthcare versus Social Security benefits today (technically, in the case of Boston College, from the period 2018-22), and throughout a couple’s entire retirement when inflation is considered (HealthView’s approach).

Both sets of data are consistent. HealthView Services reveals that for an average couple this year, around a third of their benefits will be needed to cover total retirement healthcare expenses, a modest increase over Boston College’s data from four years ago.

Inflation

Today’s thinking may lead clients to assume that the annual cost-of-living adjustment for Social Security, based on the Consumer Price Index for Urban Wage Earners and Clerical Workers, will ensure that healthcare expenses will continue to account for at least one-third of benefits going forward. That assumption would be a mistake.

Because the inflation rate for retirement healthcare costs is between 1 ½ and two times the CPI, these expenses will take up an increasing percentage of benefits. We have seen this over the last four decades. Actuarial and government data — the basis for our projections — show that this will continue in the future.

The 9.7% increase in the Medicare Part B premium for 2026 compared to a Social Security COLA of 2.8% reflects this trend. For additional context, Part D premiums alone have risen by around 50% over the last three to four years.

The Retirement Healthcare Costs Index

A decade ago, HealthView Services developed the Retirement Healthcare Costs Index to help advisors and retirees evaluate the impact of their healthcare expenses in retirement. By showing the percentage of Social Security benefits needed to cover healthcare expenses, the index helps advisors frame their impact with clients.

Since costs will vary based on a range of factors — including health conditions, state of residence, sex assignment at birth and modified adjusted gross income in retirement — it is imperative to run the numbers for individual clients based on their circumstances.

It is important to note that the index assumes that Social Security benefits will be paid out consistent with current promises. Each day that elected officials do not address the Social Security funding shortfall, the risk of cuts to future benefits grows.

For most Americans, higher-than-anticipated healthcare costs will have a significant impact on financial security in retirement. This requires advisors to use planning data that accounts for healthcare cost inflation.

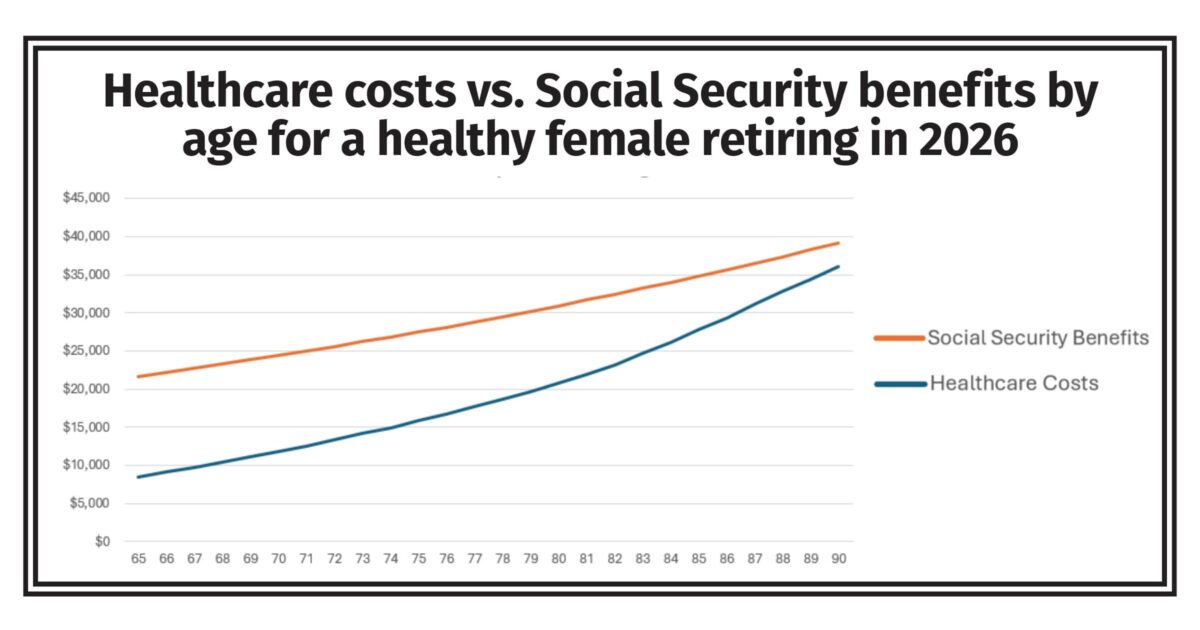

Case study

For a healthy 65-year-old woman retiring in 2026 with an average monthly Social Security Primary Insurance Amount of $2,071, the chart shows the impact of the differential between healthcare and Social Security inflation rates on the portion of benefits that will be required to address these needs.

We show average costs for premiums, including Medicare Part B, Medicare Part D, Medigap Plan G (a supplemental insurance plan) and dental insurance, as well as the additional out-of-pocket expenses (hospitalization, doctors, tests, prescriptions, vision, hearing and dental), to project total annual healthcare expenses. We assume she’ll receive Medicare Part A coverage for hospitalization at no cost in retirement, since she paid the FICA tax during her working career. We track these expenses versus her currently anticipated Social Security benefits.

In 2026, she will need 39% of her Social Security benefits to cover her projected healthcare costs. In 10 years, at age 75, she will need 58% of her Social Security benefits to meet her healthcare needs. This is based on the 6.3% average inflation rate for healthcare that reflects premium inflation, the Medigap age rating, increased utilization of services as she ages and 2.4% for Social Security COLAs.

At her life expectancy of 90, she is projected to require 92% of her Social Security benefits to cover healthcare. This does not include long-term care costs at the end of life. Over her lifetime, 67% of her total benefits will cover projected healthcare costs.

With more years of inflation driving costs higher, it should be no surprise that the Retirement Healthcare Cost Index shows that the percentage of lifetime Social Security benefits required to cover healthcare costs for a 50-year-old woman is even higher at 81%.

The financial professional’s role

Looking at healthcare costs in relation to Social Security or projected overall retirement income provides a way to frame these expenses and plan to account for the impact of healthcare inflation.

Running personalized numbers for each client provides a starting point for conversations about a range of solutions, including decumulation strategies to address healthcare needs.

Since Part B premiums are typically deducted from Social Security benefits, a good starting point for the retirement planning process is to show clients how their net annual benefits will change over time as Part B premiums increase.

In the case of a 50-year-old woman living to her actuarial projected longevity of age 90, she is expected to receive $1,092,000 in lifetime Social Security benefits, but $308,000 will be deducted to cover projected Part B premiums. Since her total lifetime projected healthcare costs will be $1,002,000, she will need to cover $694,000 from other sources of income.

While these are big numbers, setting aside $125,000 today in an insurance product with a 6% rate of return will be sufficient to address her future uncovered healthcare needs. Alternatively, increasing savings preretirement, allocating a portion of assets for healthcare, maximizing the potential benefits of health savings accounts and Roth IRAs, and implementing decumulation-focused investment strategies designed around healthcare all provide ways for advisors to maximize the efficiency of a retirement portfolio to address future needs.

The key takeaway from the data is that using a general inflation rate to project all retirement costs forward may put clients’ financial security at risk. Today, one-third of Social Security benefits will potentially be required to cover healthcare expenses.

But based on the differential between healthcare inflation and CPI-based Social Security COLAs, the retirement healthcare cost index shows that retirees will require an increasingly significant portion of their benefits to cover future healthcare needs. Since healthcare is one of the most significant expenses in retirement, planning for this expense cannot be left to chance.

Retirement healthcare is a challenge that requires a forward-thinking mindset that starts with reliable, personalized, long-term planning data that incorporates healthcare inflation into the equation as a starting point for retirement conversations and solutions.

Global economy ‘resilient’ in the wake of massive disruption

Why agents should take a second look at TV advertising

Advisor News

- How advisors can prepare clients for an uncertain retirement landscape

- Investors aren’t waiting out uncertainty

- Transamerica and Advo(k)ate Advisors launch pooled employer plan

- ‘I wish I’d met him sooner:’ Karlan Tucker remembered for integrity, faith

- Why women must be more engaged in investing

More Advisor NewsAnnuity News

- AM Best Revises Outlooks to Negative for Subsidiaries of Group 1001 Insurance Holdings, LLC

- Market-value adjusted annuities: Key considerations for advisors

- Private equity’s next play in insurance

- Immediate Care Plan: A new solution for funding LTC

- Delaware Life Launches a New Bonus Fixed Index Annuity Built for Growth, Protection, and Flexibility

More Annuity NewsHealth/Employee Benefits News

- Studies from Harvard University T.H. Chan School of Public Health Describe New Findings in Managed Care [Preconception, prenatal and postnatal exposure to gaseous air pollutants (NO2, O3) and neurodevelopmental disorders in children among …]: Managed Care

- Studies from Harvard T.H. Chan School of Public Health Further Understanding of Managed Care (Structural Racism-related State Laws and Healthcare Access Among Black, Latine, and White Us Adults): Managed Care

- Data on Managed Care Reported by Researchers at University of California Berkeley (Welfare Program Participation Among Us Farmworkers Evidence From Three National Surveys): Managed Care

- ON MEDICAID'S 61ST ANNIVERSARY, A REMINDER PENNSYLVANIA REPUBLICANS CONTINUE TO PUSH DEVASTATING HEALTHCARE CUTS

- ON 61ST ANNIVERSARY OF MEDICAID, 10,000 FEWER ALASKANS HAVE COVERAGE AFTER PASSAGE OF DAN SULLIVAN'S AGENDA

More Health/Employee Benefits NewsLife Insurance News

- AM Best Revises Outlooks to Negative for Subsidiaries of Group 1001 Insurance Holdings, LLC

- Court sides with Ameritas in denying $4M STOLI payout to Wells Fargo

- AM Best Removes From Under Review With Positive Implications and Upgrades Credit Ratings of The Fortegra Group, Inc.’s Insurance Subsidiaries

- Yancey Jr., Delos Harley

- Vincent Esparza CFP, CLU joins Wilde Wealth Management Group as Senior Wealth Advisor

More Life Insurance News