Would you rather purchase items retail or wholesale?

You’re a business owner, and you’re considering purchasing life insurance. How do you wish to pay the premium? You generally have three options:

1. Write a personal check.

2. Have your business pay the premium.

3. Have your qualified plan write the check.

Of these options, only option 3 allows a tax deduction for the insurance premium through contributions to the plan. When you purchase business or personal property, do you want to purchase it retail or wholesale?

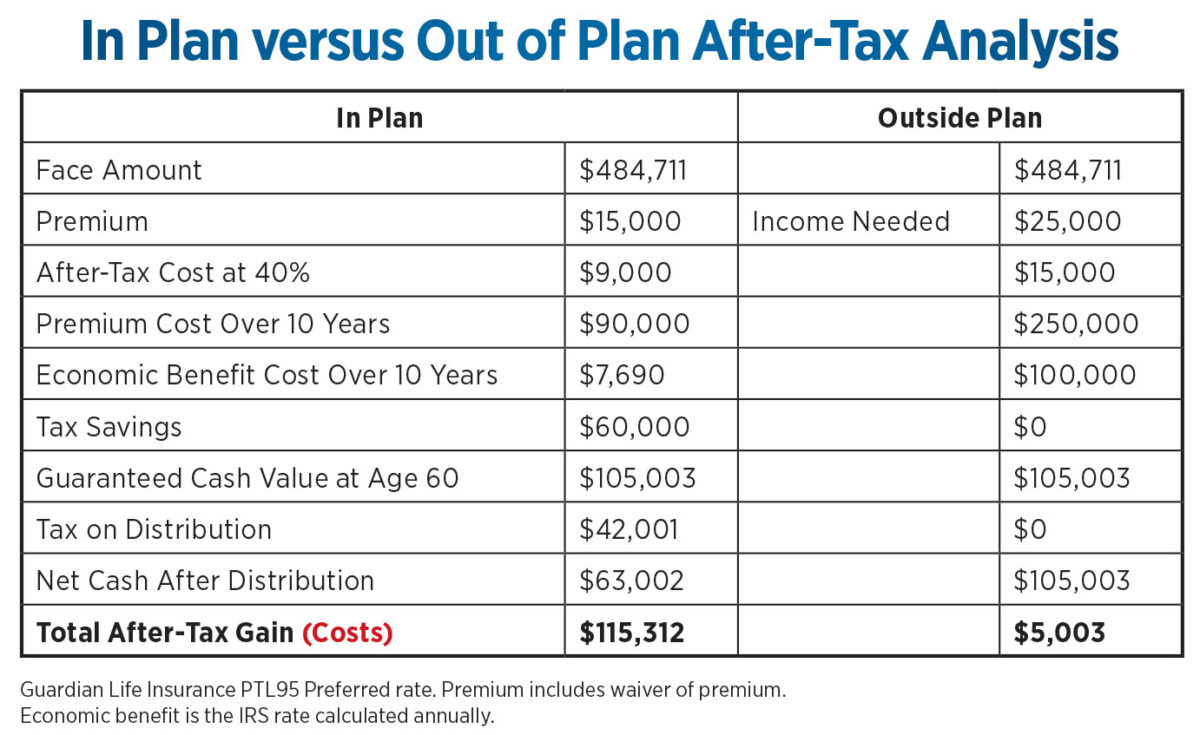

Now the question is, “How do you wish to pay the premium?” Using after-tax or tax-deductible dollars? Let’s look at the math. You own a closely held business, you’re 51 years old, in a 40% tax bracket, looking to retire in 10 years and considering purchasing $484,711 of permanent life insurance. (See chart below.)

The premium for death benefit is $15,000; in a 40% tax bracket, you would need to earn $25,000 to pay the premium. Considering the premium is in a qualified plan, contributions to the plan, within limits, are tax deductible; therefore, the after-tax cost of the premium is $9,000.

A portion of the premium that is not tax deductible represents the pure death benefit, or the current economic benefit stated as the one-year term rate for the amount at risk (face amount minus cash value times the stated year’s rate). For example, the first-year economic benefit cost is $1,220; taxed at 40%, this individual would pay $488 for $484,711 of death benefit.

Fast-forward 10 years. This policy has the potential for dividends; however, we will review only the guaranteed values in this article. The guaranteed value in 10 years is $105,300. A qualified plan has several exit strategies for life insurance that are beyond the scope of this article; I will focus on only one strategy, which is taking a distribution of the policy. I will also assume the fair market value of the policy is the cash value.

Considering the tax savings, the economic benefit cost, the cash value and tax upon distribution, over the course of 10 years, you would be better off by $110,309 having your qualified plan pay the premiums with tax-deductible dollars. Factoring in the tax savings and taking a distribution of the policy from the plan, you would net $115,312, whereas if you paid for the life insurance with after-tax dollars, you would net $5,003.

But what if you die while the life insurance is in the plan? After all, you needed the death benefit to begin with, you were looking for an alternative to pay the premium and using tax-deductible dollars made sense in your situation.

For our example, death occurs in year 10. The impact on your beneficiary would be $379,708 ($484,711 minus the cash value of $105,003), which would pass income-tax free to your beneficiary. The $105,003 of cash value plus your other investments in the plan would be a taxable distribution, which may be transferred to an individual retirement account to further delay taxes and continue tax-deferred growth.

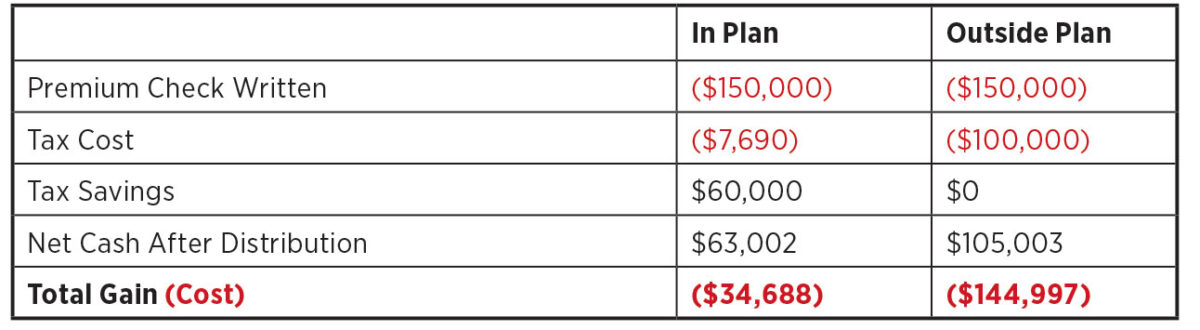

Let’s look at the math from another perspective, the actual premium inside the plan versus the premium being paid outside the plan. (See chart below.)

For $484,711 of permanent death benefit, the total premium cost over the 10-year period for this 51-year-old is $34,688 ($3,469 per year) for a permanent policy. This represents the annual cost of the premium plus the tax cost (economic benefit), minus the tax savings and the net after-tax distribution — as opposed to $144,987 ($14,499 per year) for the same policy.

For this article, we considered paying the tax from the policy, which is one option. To maintain the full policy’s death benefit and cash value, the tax could have been paid with other discretionary dollars. I usually recommend setting up a sinking fund with the tax savings from the deduction to the plan and using that fund to offset the taxable distribution.

Incorporating life insurance in the investment lineup is a fiduciary consideration and therefore must be for the benefit of all participants and their beneficiaries.

Do the math. How do you want to pay for the insurance?

The Power of Persuasion — with Lynne Franklin

Building a bridge — With Deshawn Peterson

Advisor News

- Americans aren’t turning retirement plans into action, LIMRA finds

- Ashley Hinson ‘death tax’ story collides with truth

- How advisors can prepare clients for an uncertain retirement landscape

- Investors aren’t waiting out uncertainty

- Transamerica and Advo(k)ate Advisors launch pooled employer plan

More Advisor NewsAnnuity News

- California teachers settle class-action lawsuit over in-plan annuity fees

- Jackson Financial CEO caps 40-year career with blockbuster Q2

- Lumos Insurance introduces the Immediate Care Plan to help families fund long-term care

- NAIC regulators begin consensus phase on annuity illustration overhaul

- AM Best Revises Outlooks to Negative for Subsidiaries of Group 1001 Insurance Holdings, LLC

More Annuity NewsHealth/Employee Benefits News

- AHF Optimistic About New Senate Bill to Protect 340B Program from Greedy PhRMA and Health Insurers

- Why Gen Z turns everything – even murder – into a joke

- California nearly achieved universal health care. Now, millions are losing coverage.

- Vote delayed on school employee health plan

NJ school employees' health care plan vote delayed amid 34% rate hike

- Financial planning could solve the looming Medicaid disaster

More Health/Employee Benefits NewsLife Insurance News

- ‘Uniquely positioned’: Equitable outlines future post-Corebridge merger

- Don't keep checks with clerical errors

- The insurance distributor that builds its own software will win the next decade

- iA Financial Group Reports Second Quarter Results

- Supporting small businesses starts with smarter benefits conversations

More Life Insurance News