Charitable gift annuities gaining in popularity

Charitable gift annuities are one of the simplest ways of giving but one of the most overlooked.

That was the word from two members of PNC Institutional Asset Management’s planned giving solutions group, who gave a webinar advising financial professionals of the ins and outs of this financial and philanthropic tool.

CGAs are gaining in popularity with donor prospects as they work with the charitable organizations of their choice, said Chip Giese, senior regional manager.

“A CGA starts in the heart and it starts with a gift,” said Chris McGurn, director. “It’s an easy-to-understand, one-page contract.”

Donors have several reasons to create a CGA, he said. Reasons include helping a favorite cause, easy to understand and establish, providing fixed income for life, providing a charitable gift deduction and reduction or bypass of capital gains on gifts of appreciated assets.

A CGA is an agreement between a donor and a nonprofit organization that provides the donor with a fixed income stream for life. The donor makes the gift, receives lifetime income and the organization receives the remainder of the funds in the annuity after the donor’s death.

How a CGA works

McGurn explained that in exchange for an irrevocable gift of cash, securities or other assets, the charity agrees to pay one or two annuitants named in the contract a fixed sum each year for life. The payments are backed by the charity’s general resources. The older the designated annuitants are at the time the gift is made, the greater the fixed payments the charity can agree to pay. In most cases, part of each payment is tax free, increasing each payment’s after-tax value. If the donor gives appreciated property, they will pay capital gains tax on only part of the appreciation. If the donor names themself as an annuitant, the capital gains tax can be spread out over many years instead of having it all come due in the year the gift is made.

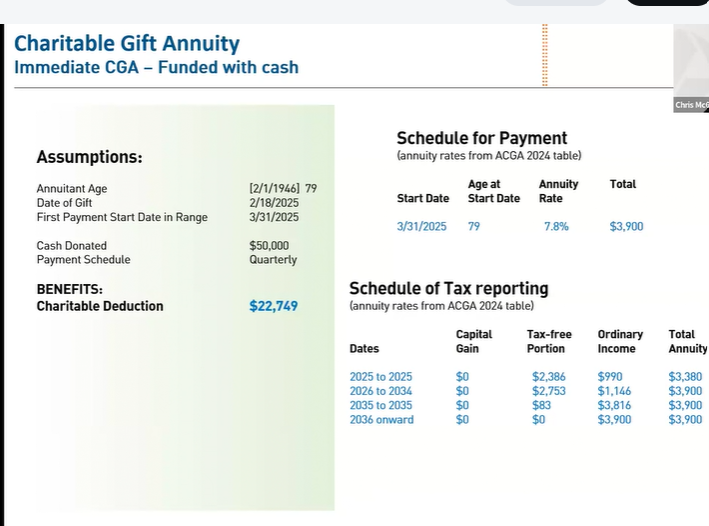

He provided a scenario in which a 79-year-old woman funds a CGA with $50,000 in cash. The payments and tax schedule would be as follows.

Giese noted that beginning in 2023, SECURE 2.0 expanded the definition of qualified charitable distributions to include distributions to create CGAs and charitable remainder trusts.

SECURE 2.0 allows a one-time maximum transfer of $54,000 in exchange with a charity for a CGA or a qualified CRT. The new QCD can be done only once during the individual retirement account owner’s lifetime and must occur within a single calendar year.

Each spouse may contribute up to $54,000 to a joint CGA from their respective IRAs. SECURE 2.0 specifies that at least one of the CGA beneficiaries must be at least age 70 ½ and the CGA must have a payout rate of at least 5%, which effectively places a lower limit on the spouse’s age.

QCDs can be made directly from an IRA – a one-time election of up to $54,000 to pass from IRA to charity in exchange for a CGA or a CRT, Giese said.

Stocks or mutual funds also can be used

A CGA also can be funded through stock or mutual funds, McGurn said. The stock must go directly from the donor’s stock account into the charity’s CGA account.

Donors may choose to create a deferred or a flexible deferred CGA, he said. This option allows the donor to choose when to take payments and is good for younger donors or for donors who want more flexibility and control.

A donor also can fund annual giving through a CGA. The donor can take the payment received from the CGA and donate all or part of it back to the charity, allowing an additional income tax deduction.

Donors also can use a CGA to fund an endowment to the charity, allowing for annual giving to continue.

© Entire contents copyright 2025 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

Should financial advisors use AI? An expert weighs in

Cross-selling LTD insurance to life insurance customers

Advisor News

- How can more Americans achieve financial independence?

- Savers vs. spenders: How money management attitudes impact financial confidence

- Demonstrating the value of life insurance to Gen Z

- Poor money habits are a dealbreaker in a new relationship

- DC plan sponsors see opportunity in alternatives

More Advisor NewsAnnuity News

- The next growth phase in life/annuities depends on modernization

- CA judge certifies class action in teachers’ lawsuit over in-plan annuity fees

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Managing Director Joins ‘Target Topics’ Podcast to Discuss State of Delegated Underwriting Authority Enterprises Market

- KBRA Assigns Rating to TruSpire Retirement Insurance Company

More Annuity NewsHealth/Employee Benefits News

- Findings from Yonsei University Advance Knowledge in Demography (Different Understandings of Scientific Research in the Use of De-identified Personal Sensitive Data: South Korea, in Comparative Perspectives): Science – Demography

- Data on Influenza Vaccines Discussed by Researchers at University of Lucerne (Keep Reminding Me To Get My Flu Shot): Immunization and Public Health – Influenza Vaccines

- Bobby Harrison: Rising insurance exchange costs bad for working poor

- New Managed Care Findings from Brown University Reported (Prior Authorization In Medicare Advantage: Beneficiary Exposure And Plan Disenrollment In 2021): Managed Care

- Findings on Managed Care Detailed by Researchers at Renal Research Institute (AI-Driven Interventions for Imminent Hospital Admissions in Patients with End-Stage Kidney Disease: A Medicare and EMR-Based Analysis): Managed Care

More Health/Employee Benefits NewsLife Insurance News

- Best’s Market Segment Report: AM Best Maintains Stable Outlook on South Korea’s Non-Life Insurance Market

- Horace Mann Strengthens Customer Relationships and Accelerates Long-Term Growth Through Transactions with Medical Mutual of Ohio

- Regulators: ‘No firm conclusions’ from first offshore reinsurance filings

- Allianz Life Study Finds Americans Struggle to Shift From Retirement Saving to Spending

- The next growth phase in life/annuities depends on modernization

More Life Insurance News