Why advisors historically underuse RILAs in planning

Introduced to the market in 2010, registered index-linked annuities are long-term savings products that limit risk exposure and provide tax-deferred growth potential.

RILAs are often viewed as a mix between a fixed indexed annuity and a variable annuity because they have greater growth potential than a fixed indexed annuity but lower potential return and risk than a variable annuity. RILAs are a great asset to any retirement portfolio because they offer flexibility through customizable risk exposure and the greatest potential for growth of any risk-managed product.

Although increased market volatility driven by global events such as the pandemic has spiked a rise in the market share of RILAs, they are complex and still relatively new, representing only about a quarter of overall annuity sales. Further education of advisors by wholesalers on RILAs will ensure that concerns about costs and other misconceptions are cleared up and that advisors can provide their clients with the best tools possible to set them up for success.

Another factor that historically has limited the growth of RILAs is how new they are. Most financial advisors are over the age of 50. For these advisors, RILAs have existed for only a small portion of their career. Sticking to the tried-and-true methods when advising a client on how to invest their money is understandable. But especially in times of financial insecurity, not providing investors with a complete picture of the products available has limited the growth of RILAs and general awareness of their benefits.

Annuities provide the financial stability that many Americans so desperately need by allowing tax-deferred growth and offering the option to have a guaranteed source of income in retirement. But there is a wide range of annuity products available, each with its own unique characteristics. Fixed indexed annuities present the lowest risk to investors but are usually overlooked due to the low growth potential that comes with this level of exposure.

At the other end of the spectrum are variable annuities, which, in these volatile times, offer a level of risk many investors do not have the financial security to afford. RILAs strike a balance between risk and return that makes them the perfect product for 2022.

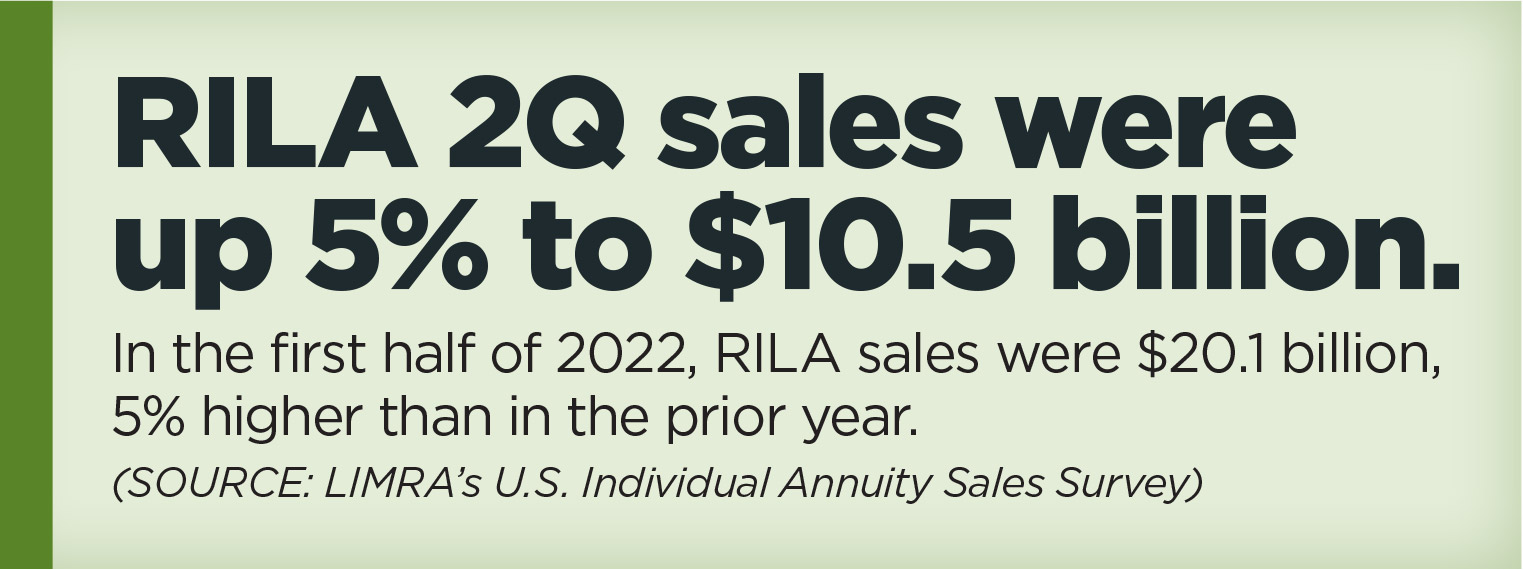

While still underused products, RILAs have dramatically increased in popularity over the past two years. According to the Secure Retirement Institute, total 2020 sales of RILAs were estimated to be at $24.1 billion (as of December 2020, final figures pending), up 38.5% over 2019 sales of $17.4 billion. Sales in 2019 were up 55% from 2018, and the forecast indicates continued growth in the area.

Expected sales growth

As more people become aware of the benefits of RILAs and understand why they are so attractive during times of volatility, there is an expectation that the growth in sales will continue. In fact, LIMRA expects RILA sales to grow as much as 50% this year, and the RILA market, which now makes up one-fourth of all variable annuities sold, to expand through 2025.

CUNA Mutual Group was the third organization to offer RILAs in 2013, and in recent years, they have started to become a major driver of growth for the organization. In March, we had our best month ever of annuities sales, and RILAs now represent 90% of CUNA Mutual Group’s 2021 deposits and 70% of our assets under management.

Another reason for the continued growth in RILA sales and annuities overall is the increase in average life expectancy. People need their savings to stretch further and last longer to accommodate an extended retirement often filled with rising health care costs. What’s more, a decline in defined benefit plans has left people without the safety nets that they have grown accustomed to. The combination of growth potential and risk protections that RILAs offer is ideal for many who are grappling with the financial issues that come with aging, such as the fear of outliving their retirement savings.

Since the market uncertainty is likely to continue in the coming years, there must be an industry shift in the narrative, not just around RILAS but also around annuities as a whole. For many, a guaranteed income product is a key pillar in a sustainable retirement plan.

People in general are not good at thinking beyond the short term, and when you take that into consideration, along with the current uncertainty of international affairs, rising inflation and the drastic shift away from defined benefit plans, it’s clear that not enough people are thinking beyond immediate accumulation.

To combat the gap between need and preparedness, the advisor industry could benefit from an industrywide, legislation-savvy consortium of experts who understand products and regulation and can advocate for constructive solutions.

Despite the resistance from some advisors, RILAs will continue to increase in popularity in the coming years. Recently introduced legislation that would make it easier for Americans to understand and access them could further accelerate their rise. It is up to the industry to communicate their benefits to all advisors, especially younger ones, who might be more open to expanding their offerings and educating Americans on the benefits of guaranteed income in retirement. This will ensure that people have the knowledge and access they need to build a secure financial future.

ACLI conference wraps up with a look at 2023’s regulatory landscape

Financially empower your female clients

Advisor News

- The overlooked retirement security risk that must be addressed

- What advisors should know about hedge funds in retirement planning

- Retirement control is top success measure for middle class, ACLI says

- Industry groups applaud House passage of Financial Exploitation Prevention Act

- Younger workers more likely to be eligible for a retirement plan after changing jobs

More Advisor NewsAnnuity News

- MassMutual Ranks No. 100 on the 2026 Fortune 500® List

- What’s fueling record annuity growth?

- Jackson Named InvestmentNews 2026 Annuities Provider of the Year

- State Farm’s agency overhaul: What distribution can learn

- IRI, ACLI express support for CLEAR Forms Act

More Annuity NewsHealth/Employee Benefits News

- Nation's first state-run long-term care insurance program about to launch in WA

- NH Dems decry Medicaid premium increases

- CVS Pharmacy, Inc. Trademark Application for “AETNA” Filed: CVS Pharmacy Inc.

- Anthem to cut Medicaid coverage for Meridian Health Services

- Kobach sues Kansas employee insurer Aetna for 'misappropriating' state funds

More Health/Employee Benefits NewsLife Insurance News

- NAIFA praises House committee approval of Clarity for Compensation Act

- PHL Variable liquidation pushed out to 2027, Connecticut regulators say

- ‘Recession-Proof’ Insurance Is Trending. Safety Net or Scam?

- Winged Keel Group Expands National Presence and PPLI Leadership, Welcomes SBSI, Inc. (dba NFP Insurance Solutions)

- MassMutual Ranks No. 100 on the 2026 Fortune 500® List

More Life Insurance News