The Annuity Evolution: New Rules, Smarter Tech

The annuity industry is undergoing rapid change, driven by evolving regulation, advances in technology and artificial intelligence, and ongoing consolidation among distributors and carriers.

Together, these forces are redefining how products are designed, sold and experienced by consumers.

This period of intense evolution is being driven by technology and the potential for a faster annuity-buying process in a society that has come to expect rapid service. But the life and annuity industry is not known for quick change.

Market competition and the enormous potential of artificial intelligence are forcing change upon companies both big and small.

Meanwhile, the bottom-line numbers reflect a vibrant industry. The final annual data from LIMRA showed that total U.S. retail annuity sales reached a record $464.1 billion in 2025, representing a 7% year-over-year increase.

Speaking during LIMRA’s recent Life Insurance and Annuity Conference, Paul Garofoli, regional sales director of individual annuities at The Standard, used a baseball analogy to describe the pace of change.

“I think we’re between second and third base,” Garofoli said.

More like first base, countered Thomas Bumbolow, head of distribution and business development at American Life.

“I think the opportunity around distributing different products, if you will, through similar distribution channels will create efficiencies and improve margins across the board,” he said. “So, I think we’re just getting started.”

Regulation: Ongoing pressure and shifting standards

Regulation continues to influence nearly every aspect of the annuity market, particularly around sales practices, disclosures and fiduciary responsibility. Efforts tied to the Department of Labor’s fiduciary rulemaking attempts and the broader “best interest” standard have pushed firms to strengthen compliance, documentation and oversight.

This has had a ripple effect across distribution. Broker-dealers and insurers have had to decide whether to build internal compliance capabilities or partner with third-party organizations. In many cases, that decision has fueled consolidation, as firms acquire insurance marketing organizations or other distributors to control the client experience and reduce regulatory risk.

Roughly 45% of annuity sales now flow through independent broker-dealers and insurance marketing organizations, reflecting the broader move away from captive distribution.

At the same time, regulators are increasingly focused on suitability, replacement activity and transparency — especially as annuity exchanges rise. This scrutiny is forcing firms to rethink incentives and ensure recommendations are clearly aligned with client outcomes.

As of April, the DOL has officially removed the 2024 Retirement Security Rule and has restored the longstanding 1975 “five-part test” for determining fiduciary status. The DOL currently has no plans to re-propose a direct replacement for the Biden-era rule that would broadly expand the fiduciary definition.

Instead, the department has shifted its focus toward new regulatory frameworks and guidance aimed at providing fiduciaries with more flexibility and specific “safe harbors” for plan investments.

‘They want to go out and sell’

Industry consolidation accelerated after regulatory changes, said Stephanie Bartruff, executive vice president of institutional sales and distribution for Annexus Group, including the DOL’s former fiduciary rule efforts. Firms responded by either acquiring distribution networks or outsourcing back-office support.

The result, Bartruff explained, is a hybrid model where firms must balance centralized operations with maintaining relationships across multiple carriers and channels. It is at times a difficult collaboration, she noted.

Ryan Hinchey, senior vice president of product innovation at AmeriLife, noted that consolidation is driving significant acquisition activity, with firms seeking efficiencies by absorbing smaller distributors and centralizing administrative functions.

AmeriLife is one of the biggest acquirers, having added more than 100 acquisitions on the health side and 30 on the wealth side, Hinchey said.

“These are entrepreneurs, and they want to go out and sell,” he said. “So, can we make them more effective by letting them sell and taking care of everything else?”

As this issue went to press, the National Association of Insurance Commissioners was working on a pair of significant potential rule changes.

Updating the Annuity Buyer’s Guide. The newly created Annuity Buyer’s Guide Working Group is reviewing draft changes meant to update the guide, last updated in 2013. Since then, new product innovations such as registered index-linked annuities have surged to the top of sales charts.

Proposed revisions focus on providing a more balanced view of annuity benefits and risks. Key additions include sections on:

» Market value adjustments and their impact on withdrawals.

» Guaranteed living benefits beyond simple withdrawal riders.» Persistency bonuses and other complex product features not covered in the 2013 version.

Industry trade representatives are unhappy with the language and general tenor of the draft changes.

“The tone and tenor of the guide is perhaps unnecessarily negative,” said Pam Heinrich, general counsel and director of government affairs for the National Association for Fixed Annuities, during a recent working group call.

The guide is delivered “after they’ve already chosen to purchase and apply for an annuity contract,” she added, noting that current “best interest” standards adopted in most states already require disclosures and conversations before a sale. Those standards were not in place when the buyer’s guide was initially adopted.

Indexed annuity illustrations. Another newly renamed NAIC group, the Life Insurance and Annuities Illustrations Working Group, is working on tweaking the rules to rein in annuity illustrations that ballooned to as high as 27%.

Regulators question whether consumers are receiving an accurate picture of potential performance at the point of sale.

The working group is debating whether to build on existing rules — particularly Model Regulation 245, which governs annuity illustrations — or pursue a more comprehensive overhaul.

Some industry trade groups support broader adoption of the current model across states as a near-term step to improve consistency.

Others, including several regulators and consumer advocates, argued that the model is outdated and insufficient to address current concerns. They called for more fundamental changes, including limits on the use of historical data, clearer disclosures of non-guaranteed elements and greater use of visual tools to improve consumer understanding.

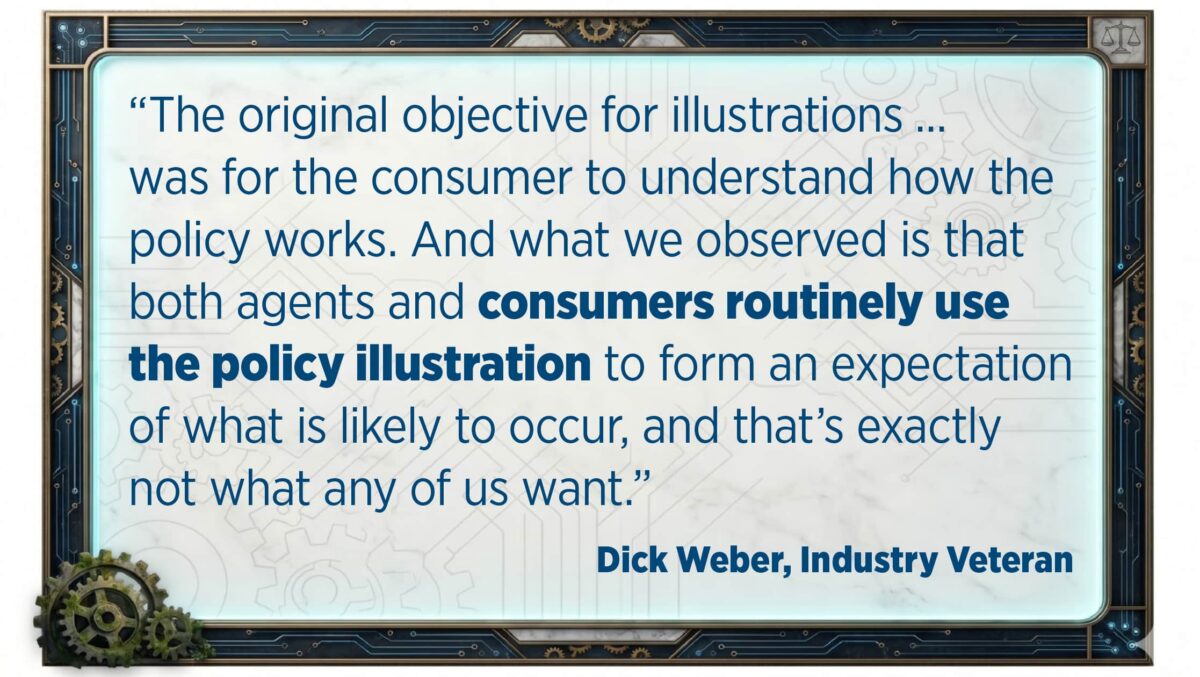

“The original objective for illustrations ... was for the consumer to understand how the policy works,” said industry veteran Dick Weber during a recent call. “And what we observed is that both agents and consumers routinely use the policy illustration to form an expectation of what is likely to occur, and that’s exactly not what any of us want.”

Technology and AI: From product to experience

Technology is rapidly becoming a defining competitive factor in the annuity space. Historically known for complex products and paper-heavy processes, the industry is now investing heavily in digital platforms to simplify everything from product design to policy administration.

Ease of use, digital capabilities and the overall client experience are increasingly critical, especially for younger investors.

“There’s more need now than ever for product managers to really understand the entire ecosystem in which their product is going to market,” said Aaron Murphy, associate vice president of variable annuity business development at Nationwide, “including the distribution strategies, the marketing strategy behind it, and what the experience is.”

Improving the purchasing process, often seen as cumbersome compared with digital investment platforms, will be key to attracting new customers, he added during a LIMRA session.

Modern systems are enabling more modular product development, allowing insurers to customize features without rebuilding products from scratch. At the point of sale, digital tools are streamlining applications, improving speed and reducing friction — a critical shift as consumers grow accustomed to fast, intuitive financial platforms.

The 2020 COVID-19 disruption accelerated the adoption of digital tools such as electronic applications, e-signatures and online policy delivery. Those changes have largely persisted even as in-person meetings and events returned.

“The idea that we would do anything but e-sign for the large majority of the business, that hasn’t gone away at all,” said Sky Opila, head of business development and growth at Zinnia.

Despite progress, the industry still faces friction in onboarding and servicing, often tied to legacy systems that lack real-time integration. Experiences can vary widely depending on the distribution channel, with bank and institutional platforms generally offering more seamless transactions than independent channels.

“It’s kind of a mixed bag,” Garofoli said. “There are still agents who want to get a hard copy of the policy and want to deliver it and go old school.”

AI continues to play a larger role as well.

Many annuity sellers are using AI to help agents build an entire sales process in minutes, offering case design comparisons and automated “product translation” into plain English for clients.

Zinnia provides a digital platform for life and annuity sellers that features automated document summaries and prefilled forms to eliminate “not in good order” errors.

Some firms report that more than half of applications can now be processed without human intervention, reducing errors and turnaround times.

“Workflow automation is an exciting term that’s real with AI right now,” Opila said.

Consolidation and competition

Consolidation has been one of the most visible trends in the annuity market, particularly among distributors. Large firms have acquired smaller insurance marketing organizations and broker-dealers to gain scale, expand distribution and centralize operations.

This trend has created both opportunities and challenges. Larger distributors can negotiate more effectively with carriers and demand tailored products, but they also introduce more competition within their platforms.

Carriers face increased competition within expanded product shelves and greater demands for customized solutions.

Larger distributors are leveraging their scale to negotiate tailored products, Murphy noted, while also operating distinct internal channels that require different strategies.

“It has created some unique challenges,” he said, including questions about how legacy agreements apply when distribution firms merge or acquire new business.

Despite rising demand for personalized products, experts caution against excessive customization, citing cost and complexity. Many carriers are instead using technology to modify existing products for specific distribution partners, rather than building entirely new offerings.

“You can’t do complete customization of everything,” Murphy said. “But I think there is a way to do a lot more personalization of the products than ever before.”

Modern systems allow for modular product design, enabling faster adjustments without lengthy development cycles, Hinchey added.

For carriers, this means competing not just on product features, but also on relationships, service and the ability to deliver customized solutions at scale. At the same time, smaller and newer entrants are entering the market with fresh capital and modern technology, intensifying competition further.

The result is a more complex ecosystem in which differentiation is harder to achieve. In some segments, products risk becoming commoditized, pushing firms to compete on pricing, innovation timing or distribution strategy rather than core design.

A changing industry landscape

Taken together, these forces are pushing the annuity industry toward a more integrated, client-focused model. Firms are moving beyond standalone product sales toward broader financial solutions while investing in technology and partnerships to stay competitive.

Even as annuity sales reach record levels, the industry faces a critical challenge: expanding beyond existing customers and educating new ones. How effectively firms respond to regulatory demands, embrace technology and navigate consolidation will shape the next phase of growth.

Annuity executives agree on one point, however: Humans will not be phased out of the process.

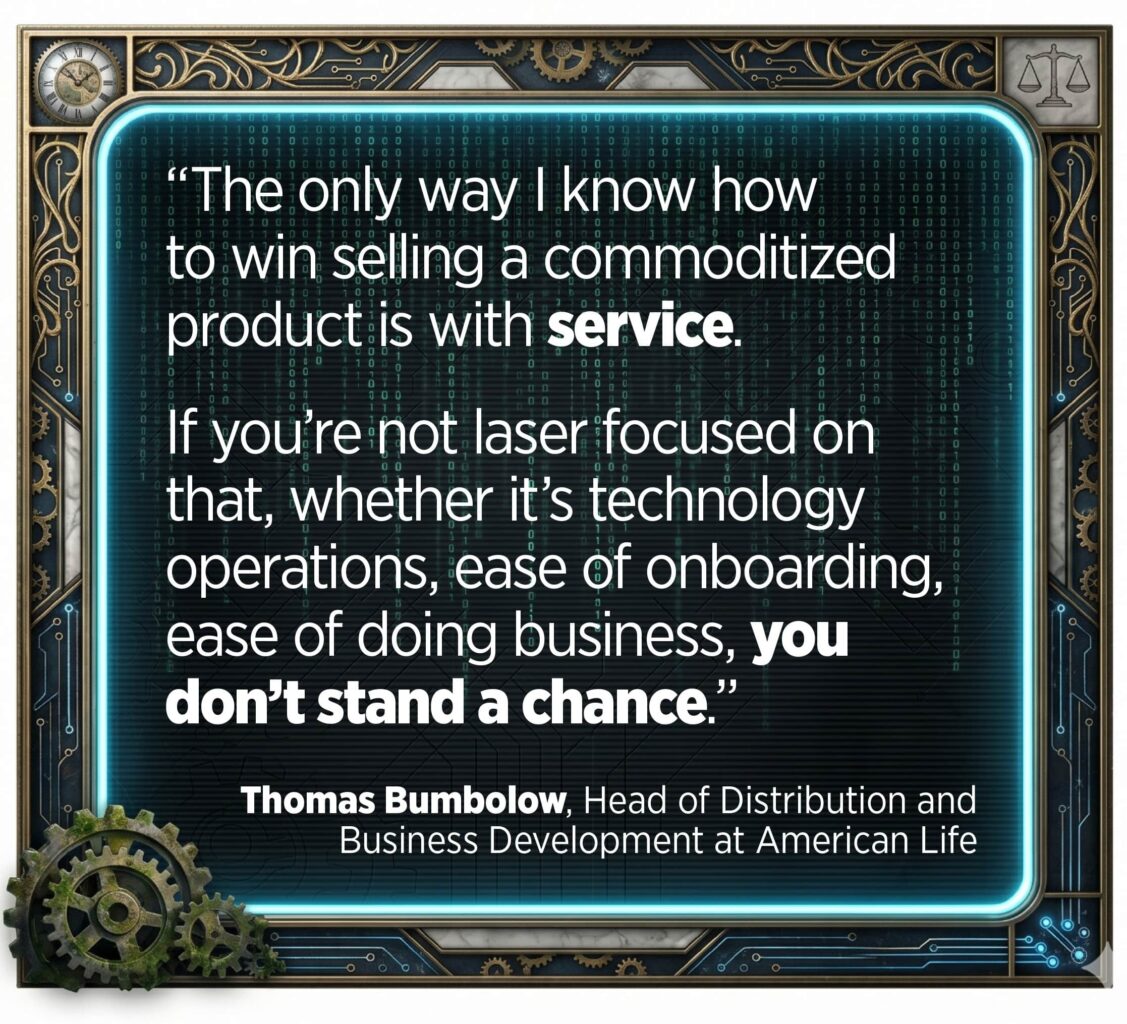

With annuities often viewed as commoditized products, Bumbolow emphasized that service, including ease of onboarding and ongoing support, is critical to winning and retaining business.

“The only way I know how to win selling a commoditized product is with service,” he said. “If you’re not laser focused on that, whether it’s technology operations, ease of onboarding, ease of doing business, you don’t stand a chance.”

Annuities at the speed of a cheetah — With Mark Zesbaugh

Setting the record straight on premium-financed IUL

Advisor News

- Nearly half of nonretirees doubt they will fully retire

- How much could failure to fund Social Security cost average Americans?

- How can more Americans achieve financial independence?

- Savers vs. spenders: How money management attitudes impact financial confidence

- Demonstrating the value of life insurance to Gen Z

More Advisor NewsAnnuity News

- Jackson CEO Laura Prieskorn to retire at the end of 2026

- Has your annuity been reinsured in the Cayman Islands? Here’s why it matters

- DOL slams pension risk transfer lawsuit as ‘opportunistic’ litigation

- AM Best Affirms Credit Ratings of New York Life Insurance Company and Its Subsidiaries

- Advisors don’t have an annuity problem; they have an integration problem.

More Annuity NewsHealth/Employee Benefits News

- New dashboard tracks Kansas Affordable Care Act enrollment by legislative district, county

- ICYMI – CANDIDATE COOPER NOW TRYING TO BLAME HIS HEALTH INSURANCE PALS FOR GOVERNOR COOPER'S 57% INCREASE IN HEALTHCARE COSTS IN NC

- Business People: Edric Funk to take over as Toro Co. CEO

- Insurers propose premium increases for ACA customers in Iowa

- How Does New CareScout Long-Term Care Insurance Policy Compare In Cost

More Health/Employee Benefits NewsLife Insurance News

- Best’s Market Segment Report: AM Best Maintains Stable Outlook on Vietnam’s Non-Life Insurance Segment

- AM Best Comments on Credit Ratings of Horace Mann Educators Corporation and Its Subsidiaries Following Announced Transaction with Medical Mutual of Ohio

- AM Best Affirms Credit Ratings of Hanwha General Insurance Company Limited

- Globe Life boosts Q2 earnings, eyes AI shift for long-term growth

- ATTORNEY GENERAL BRENNA BIRD LEADS FIGHT TO PROTECT IOWA PENSIONS

More Life Insurance News