RILAs: Still a teenager and already a leader

Registered index-linked annuities were introduced in 2010 during a historically low-interest-rate environment. Since then, RILAs have grown from $0 to $65.4 billion in sales in 2024 and from one company to 23 companies offering the product. Only 15 years old, RILA products continue to evolve and mature, addressing clients’ needs.

RILAs appeal to more than just clients — they’re less capital-intensive for insurers, making them especially attractive to product manufacturers. Meanwhile, traditional variable annuities — once all the rage — have declined from $183.7 billion in 2007 to just $60.9 billion in 2024, roughly a third of their former sales volume.

RILAs offer a new value proposition: a blend of market participation and downside protection, supported by features such as caps, buffers and participation rates that help define a more predictable range of outcomes within a financial plan.

We’ve all heard about the importance of being “asset allocated,” but “asset location” — where assets are held, such as in an annuity — is also important. With modern advisor platforms, integrating products such as RILAs into their practice is easier now than in days past.

Although RILAs are still maturing, four new products were launched in 2024 alone, the most in any one year.

Whether investors are members of Generation X — who may not feel confident about their retirement readiness — or members of the baby boomer generation, which has more people entering retirement this year than ever before, they may be asking themselves three essential questions.

1. How much of your retirement savings can you afford to lose?

2. How much of the market upside would you like to participate in?

3. How important are guarantees right now?

While these questions can apply across other annuity products, RILAs stand out by addressing a need that has gone unmet in the annuity space; they offer a solution for those seeking greater market participation than traditional spread-based protection products, while still wanting some level of downside protection.

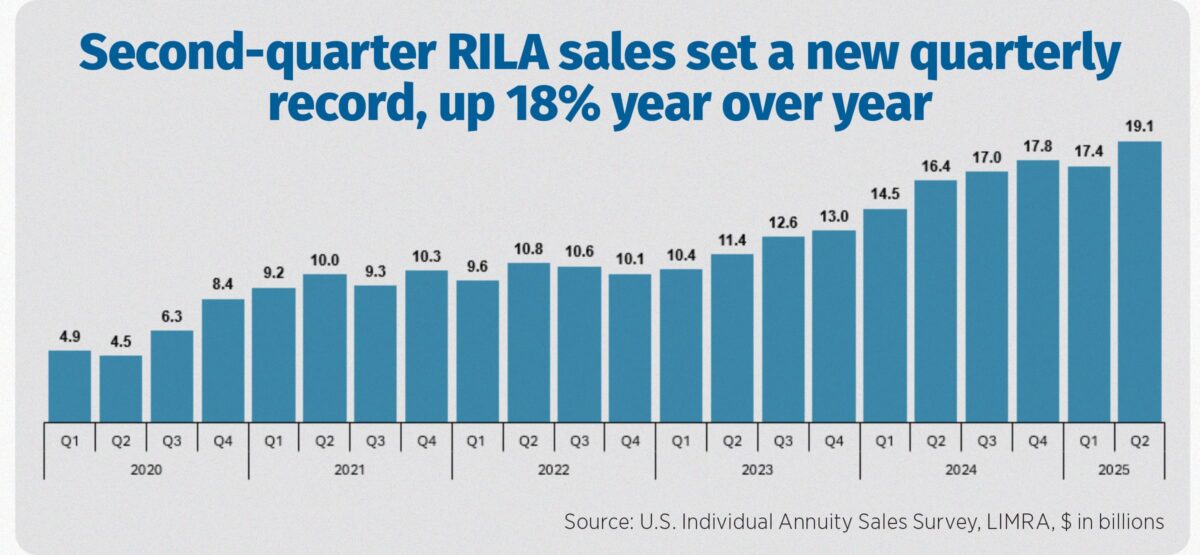

RILA sales surged in early 2020 as nervous investors — coming off a decade-long bull run and then in a pandemic — faced a sudden 30% market drop in just under a month. That sharp decline may have prompted nervous investors to ask, “How can I protect the savings I’ve built over the past decade and still grow my assets — without the fear of loss?” Demand for RILAs surged; since Q1 2020, through Q2 2025, we’ve seen 15 record-breaking quarters (out of 22) with more than a quarter-trillion dollars in RILA sales during this period.

Going forward, if the economy shifts into a lower interest rate environment, RILAs may prove more resilient than traditional fixed products. Fixed annuities are highly reactive to declining interest rates, while RILAs can be argued to be in a better position to withstand a decrease in rates (after all, they were designed in a low-rate environment).

With more education, continued innovation, new entrants, broader distribution and favorable regulation, RILAs seem poised for continued growth, aligned with evolving retirement needs. LIMRA’s current forecast has RILA sales growing $64 billion to $69 billion in 2026 and $64 billion to $72 billion in 2027.

Wholesalers often say, “It’s not what it is, but what it does.” What a RILA does is give your clients the opportunity to earn more than the strongest fixed annuities while protecting the downside of their investment like a structured note. It grows tax-deferred and offers the potential to generate an income stream ensuring clients don’t run out of money before they run out of life. With that combination of growth, protection and income, along with educational tools and technology to integrate into a holistic financial plan, it’s hard to imagine these value propositions fading anytime soon.

Will we need AI to monitor AI?

Fixed annuities give clients more money to spend in retirement

Advisor News

- SEC nears settlement with accused scammer Tai Lopez

- The 3 things that shrink your Social Security income

- Proposed legislation takes aim at Social Security shortfall

- The overlooked retirement security risk that must be addressed

- What advisors should know about hedge funds in retirement planning

More Advisor NewsAnnuity News

- Globe Life Inc. (NYSE: GL) Highlighted for Surprising Price Action

- Trademark Application for “EMPOWER YOUR MONEY” Filed by Empower Annuity Insurance Company of America: Empower Annuity Insurance Company of America

- Built-in guaranteed annuities: What advisors should know

- Malibu Life Holdings Completes Acquisition of TruSpire, Establishing Malibu USA and Accelerating Entry into the U.S. Retail Annuity Market

- Why job boards are failing insurance agencies

More Annuity NewsHealth/Employee Benefits News

- UnitedHealthcare launches spending account benefit

- Afternoon Briefing: Health insurers propose double-digit-percentage price increases

- Health insurers propose double-digit-percentage price increases for Illinois exchange plans

- Anthem Establishes Coverage of C2N Diagnostics’ PrecivityAD2® Blood Test for Alzheimer’s Disease Evaluation

- Reynolds creates Iowa Medicaid fraud task force

More Health/Employee Benefits NewsLife Insurance News

- AM Best Revises Outlooks to Stable for Missouri Farm Bureau Group’s Members and Farm Bureau Life Insurance Company of Missouri

- Globe Life Inc. (NYSE: GL) Highlighted for Surprising Price Action

- AM Best Assigns Credit Ratings to China Ping An Insurance (Hong Kong) Company Limited

- Reliance Matrix Expands Employee Navigator Integration with New Evidence of Insurability (EOI) API Enhancement

- How AI is changing the insurance claims process and what it means for accident victims

More Life Insurance News