Could COVID-19 Lead To Higher Life Insurance Sales?

The effect of the COVID-19 pandemic on Americans is immeasurable. Our health and well-being concerns became all-consuming over the course of the last 18 or more months. As vaccines are now widely available and many people have begun to venture out in public, financial advisors and life insurance agents have begun face-to-face meetings with their clients again.

But what about gaining new business? What has the pandemic done in terms of life insurance awareness and purchase intent? LIMRA and Life Happens fielded their 11th annual Insurance Barometer study in January during the height of the “second wave” of the pandemic in much of the U.S.

Historically, the majority of Americans have preferred to purchase life insurance in person with an agent or advisor. As use of technology has become nearly ubiquitous and people have grown accustomed to conducting meetings and transactions online, this trend has shifted. In 2011, 64% of consumers said they preferred to buy in person; by 2020, just 41% felt this way. It is not surprising that the preference for online purchasing nearly doubled from 17% in 2011 to 29% in 2020.

During the pandemic, more Americans of all ages became accustomed to transacting online. Life insurance and other similar products can be confusing for prospective clients, and face-to-face is still the most preferred method of finalizing such purchases. It is clear, however, that the industry must adapt to the changing channel and distribution landscape.

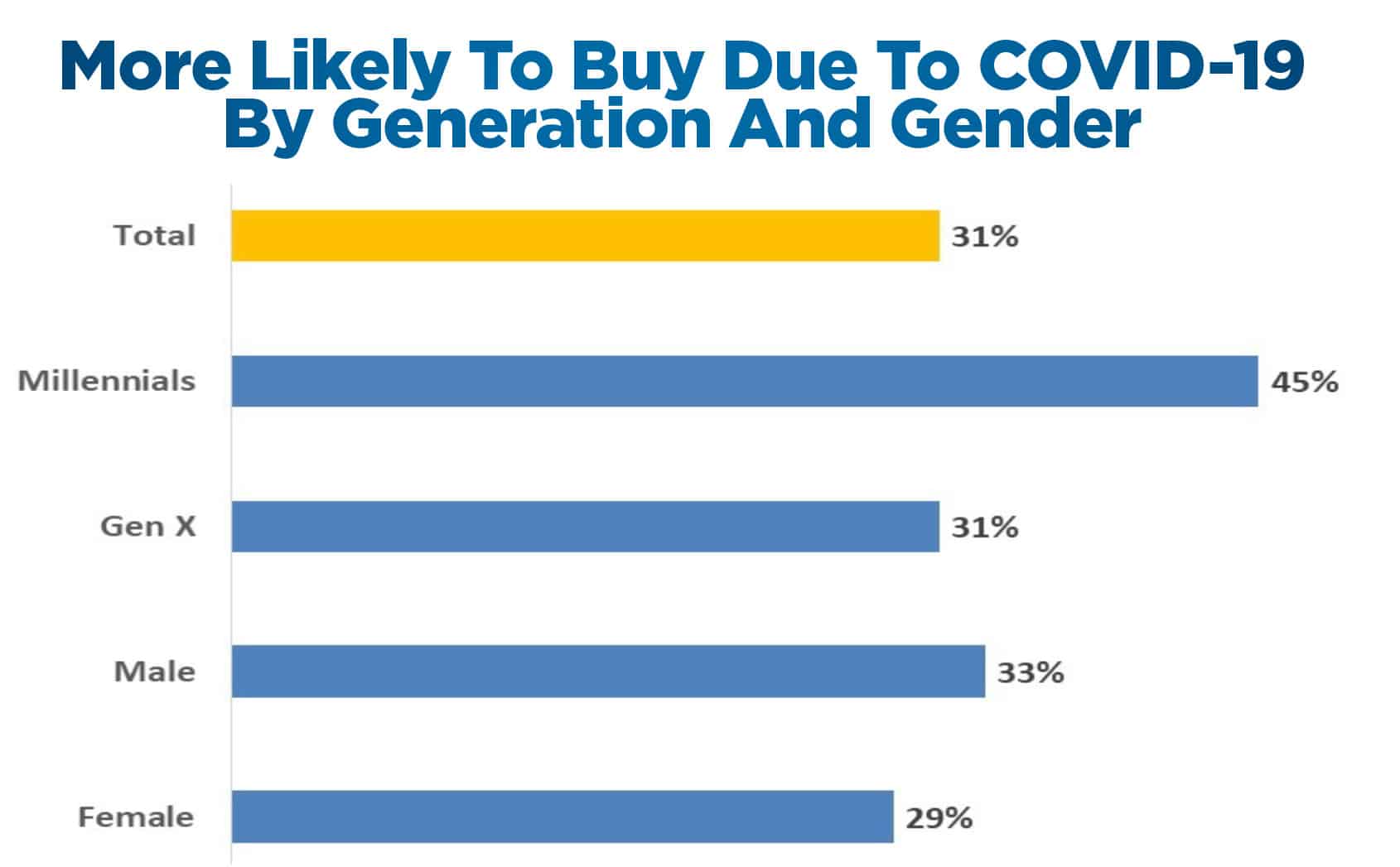

Life events such as births, marriages, job changes and deaths of family and friends prompt people to consider purchasing life insurance. The COVID-19 pandemic is a life event that all of us have experienced at the same time, over an extended period. The pandemic lifted the likelihood of buying life insurance for many consumers; almost one in three (31%) said they were more likely to buy because of the pandemic.

Two-thirds of those surveyed said they personally knew someone who had tested positive for COVID-19. Of those individuals, the likelihood of obtaining life insurance in 2021, at 33%, was nearly the same as it was for the entire respondent pool. For those who tested positive themselves, that number rose to 42%. This shows that it is often personal experience — whether starting a family or battling a dangerous virus — that drives life insurance sales.

Of course, purchase intent does not equate to sales. Even the most well-intentioned consumer may have some perceptions about life insurance and the industry that put roadblocks in their way.

More than half of the survey’s respondents (53%) admit they are unsure what product they would need or how much coverage to purchase. Nearly half (45%) stated that they have simply put off purchasing, and more than a third (36%) believe they would not qualify for coverage.

These are significant obstacles for the industry and indicate the need for compelling communications to help consumers build appreciation for the broad value proposition that life insurance offers.

According to the 2021 Insurance Barometer, slightly more than half (52%) of American adults own some form of life insurance coverage (e.g., individual, employer sponsored), which is a decline of two points from 2020. This marks the lowest level of self-reported ownership to date in the 11 years of this study. Perhaps with online purchasing increasing before the pandemic and so many more people now comfortable conducting business and transactions online, the life insurance industry could be looking at higher sales as it navigates this post-pandemic world.

Advisors Are Helping Clients Grow Greener

The Five W’s Of Creating A Memorable Family Reunion

Advisor News

- Business owners may be overlooking a key part of their financial picture

- How smart investments prepare clients for inflation

- Amid slew of corporate tax ideas, Newsom chose one likely to hit people’s premiums

- The biggest risk to your clients’ financial plans isn’t market volatility

- Initiative looks at how caregiving impacts workplace benefits

More Advisor NewsAnnuity News

- Best’s Special Report: U.S. Life/Annuity Industry Sees Bottom-Line Growth Despite 18% Decline in Total Income in First-Quarter 2026

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- Fortitude Re Completes $500 Million FABN Issuance

- Reframing retirement income for greater certainty

- Jackson Introduces Dow Jones Industrial Average Index Option, Flexible Premiums, Six-Year Rate Guarantee in Latest Registered Index-Linked Annuity Launch

More Annuity NewsHealth/Employee Benefits News

- A Swansea woman's health insurance saga: Breast cancer leads to bankruptcy

- SEN. OSSOFF WORKING ACROSS THE AISLE TO LOWER HEALTH CARE COSTS FOR MILITARY FAMILIES

- Inovaare Expands AI-Native BPaaS for U.S. Health Plans, Defining the Third Generation of Payer Operations

- AuguStar Life enhances its suite of living benefits

- Final rules for Medicaid work requirements are out. Here's what you need to know.

More Health/Employee Benefits NewsLife Insurance News

- Greg Lindberg slams ‘vindictiveness’ in fight for prison computer access

- Best’s Special Report: U.S. Life/Annuity Industry Sees Bottom-Line Growth Despite 18% Decline in Total Income in First-Quarter 2026

- AuguStar Life enhances its suite of living benefits

- Lobbyist argues Iowa insurance regulator gives too much voice to Wall Street

- Appeals court rejects investor payouts in latest decision against STOLI

More Life Insurance News