Annuity income: The new 401(k) standard?

TAMPA, Fla. -- The push to include annuity products in 401(k) plans resembles the early evolution of participant-directed investing, said Kent Peterson of Securian Financial Group.

That is, promising, but still in its formative stages.

Speaking on a LIMRA Life Insurance and Annuity Conference panel about retirement innovation, Peterson traced the industry’s transformation back to 1990. In those days, most workplace retirement plans were employer-directed and updated only quarterly.

“A lot of times, you didn't know what your balance was until the end of the quarter," he said. "It was an interesting time."

The shift in the 1990s toward daily valuation and participant control marked what he described as the “first generation” of recordkeeping. Today’s emerging guaranteed income products, usually annuities, are at a similar early stage, with significant barriers to adoption.

Among the biggest challenges: complexity, lack of transparency and limited understanding among fiduciaries responsible for overseeing retirement plans.

Advisors and plan sponsors repeatedly cite complexity as a key obstacle, panelists said, noting that many struggle to evaluate insurance-backed products or explain them to clients.

“They say it takes three times to explain it to me. As a financial advisor, how am I going to explain it to the plan sponsor?” said Peterson, senior vice president, institutional retirement at Securian.

Successful products will need to meet several criteria to gain wider acceptance. They must be transparent, portable between employers, and “modular” — meaning they can be separated from underlying investments if those investments are replaced.

That flexibility is critical in a heavily regulated environment governed by fiduciary standards under the Employee Retirement Income Security Act.

“There’s fiduciary friction when you put a product into a lineup that can’t be fired,” Peterson said.

New rules could help

The Department of Labor recently issued guidance aimed at clarifying how fiduciaries can evaluate such products, including the use of benchmarks and process-based standards. Panelists said the guidance could push providers to improve product design, though some expect further revisions.

Despite the challenges, industry data suggests momentum is building.

Assets in guaranteed income solutions within defined contribution plans now total in the billions, a small share of the roughly $14 trillion 401(k) market but a sign of growing favor.

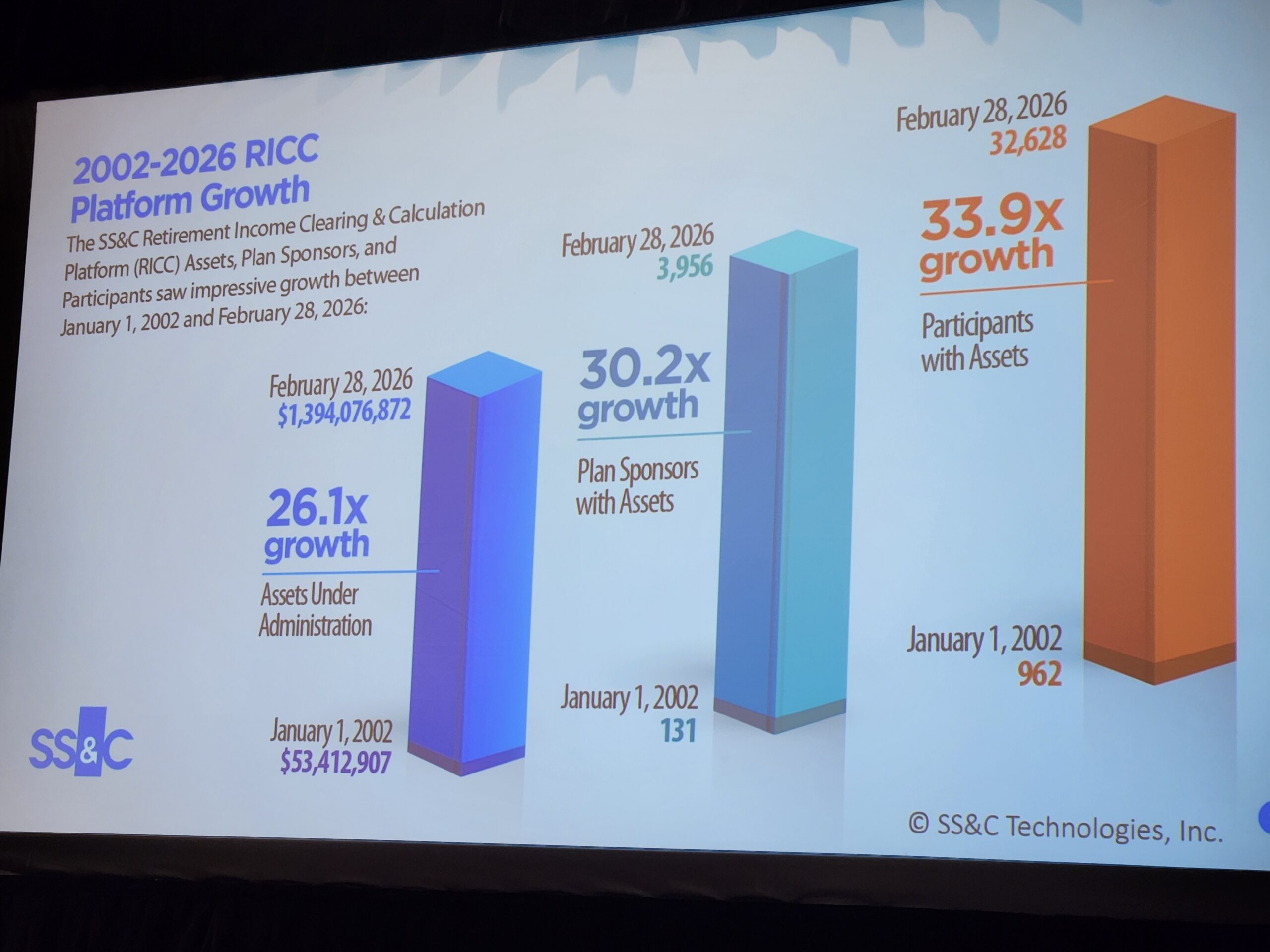

“I think there's still a misperception in the marketplace that this is kind of conceptual, that it hasn't happened yet, that participants aren't actively in these products, plans aren't using it," said Ryan Grosdidier, business development lead for retirement income solutions at SS&C Retirement Solutions. "That's not the case."

Grosdidier shared a slide on the growth SS&C experienced:

Panelists pointed to the passage of the SECURE Act as a turning point, spurring product development and easing some regulatory concerns about offering annuities in workplace plans.

They also highlighted increasing involvement from major asset managers, including Vanguard, as a signal that the market is maturing.

Still, barriers remain — particularly for smaller insurance companies seeking to enter the space. These include technological integration with recordkeeping platforms, distribution challenges and the need to compete with larger, established providers.

For now, speakers agreed, trust will be the deciding factor.

“You have to build trust with the plan sponsors," Peterson said. "You have to build trust with the plan advisors. And then, as you move up this chain, through adoption and retention, there will be great growth in the industry."

© Entire contents copyright 2026 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

Architecture plays a role in mitigating climate risk

OBBBA can give small-business clients opportunities for saving

Advisor News

- How much could failure to fund Social Security cost average Americans?

- How can more Americans achieve financial independence?

- Savers vs. spenders: How money management attitudes impact financial confidence

- Demonstrating the value of life insurance to Gen Z

- Poor money habits are a dealbreaker in a new relationship

More Advisor NewsAnnuity News

- Canvas steps into the direct-to-consumer market that has yet to take off

- The next growth phase in life/annuities depends on modernization

- CA judge certifies class action in teachers’ lawsuit over in-plan annuity fees

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Managing Director Joins ‘Target Topics’ Podcast to Discuss State of Delegated Underwriting Authority Enterprises Market

More Annuity NewsHealth/Employee Benefits News

- Covered California rates to jump nearly 10% as thousands struggle to afford coverage

- A Tale of Two Behavioral Health Systems, or How the State Border Determines Who Gets Access to Mental Healthcare

- Recent Findings from Iwate Medical University Provide New Insights into Science (Nonlinear Associations Between Sleep Duration and Incident LTCI Certification in Older Adults: Findings From the Iwate-Kenpoku Cohort Study): Science

- Researchers from Capital Medical University Detail New Studies and Findings in the Area of Managed Care (Factors Contributing To the Enrollment of Ambiguous Medical Insurance Cases: a Retrospective Study At a Tertiary Hospital In Beijing): Managed Care

- Studies from Cornell University Further Understanding of Managed Care (IRA Reforms To Medicare Part D Reinsurance Were Associated With Plan Exits And Higher Premiums, 2024-25): Managed Care

More Health/Employee Benefits NewsLife Insurance News

- USAA introduces Secure Start whole life program for children

- Best’s Market Segment Report: AM Best Maintains Stable Outlook on South Korea’s Non-Life Insurance Market

- Horace Mann Strengthens Customer Relationships and Accelerates Long-Term Growth Through Transactions with Medical Mutual of Ohio

- Regulators: ‘No firm conclusions’ from first offshore reinsurance filings

- Allianz Life Study Finds Americans Struggle to Shift From Retirement Saving to Spending

More Life Insurance News