Advisors play critical role in retirement planning

LIMRA’s 2023 Retirement Investors Survey shows that ongoing guidance from financial advisors remains essential as Americans approach and enter retirement. Changes in the way retirees generate income suggest an even more important role for financial advisors in the years to come.

Although most current retirees rely primarily on guaranteed sources like Social Security and pensions for income, the survey highlights room for improvements that advisors are uniquely positioned to address. Around a quarter of retirees surveyed this year do not receive sufficient guaranteed lifetime income to cover basic living costs without tapping into their savings. Although this proportion has remained similar for more than a decade, the long-term trend away from traditional defined benefit pensions suggests that future retirees will have greater challenges in generating guaranteed income. Current pre-retirees agree, as less than half believe they will have sufficient guaranteed income sources in retirement.

For the sizable minority of retirees who report shortfalls between guaranteed income and basic costs, withdrawals from savings are a common approach. However, this approach risks depleting assets before death, due to unknown life spans. Advisors can demonstrate more sustainable drawdown techniques or guaranteed income substitutes to preserve peace of mind in retirement.

Although annuities present an appealing strategy for addressing income gaps, fewer than 1 in 5 retirees receive annuity income. Among those receiving distributions from qualified accounts, only a small minority do so through guaranteed lifetime payments. Advisors are well positioned to expand appropriate annuity use by explaining how different annuity options can enhance financial resilience in retirement, especially as an increasing number of defined contribution plans begin to offer them.

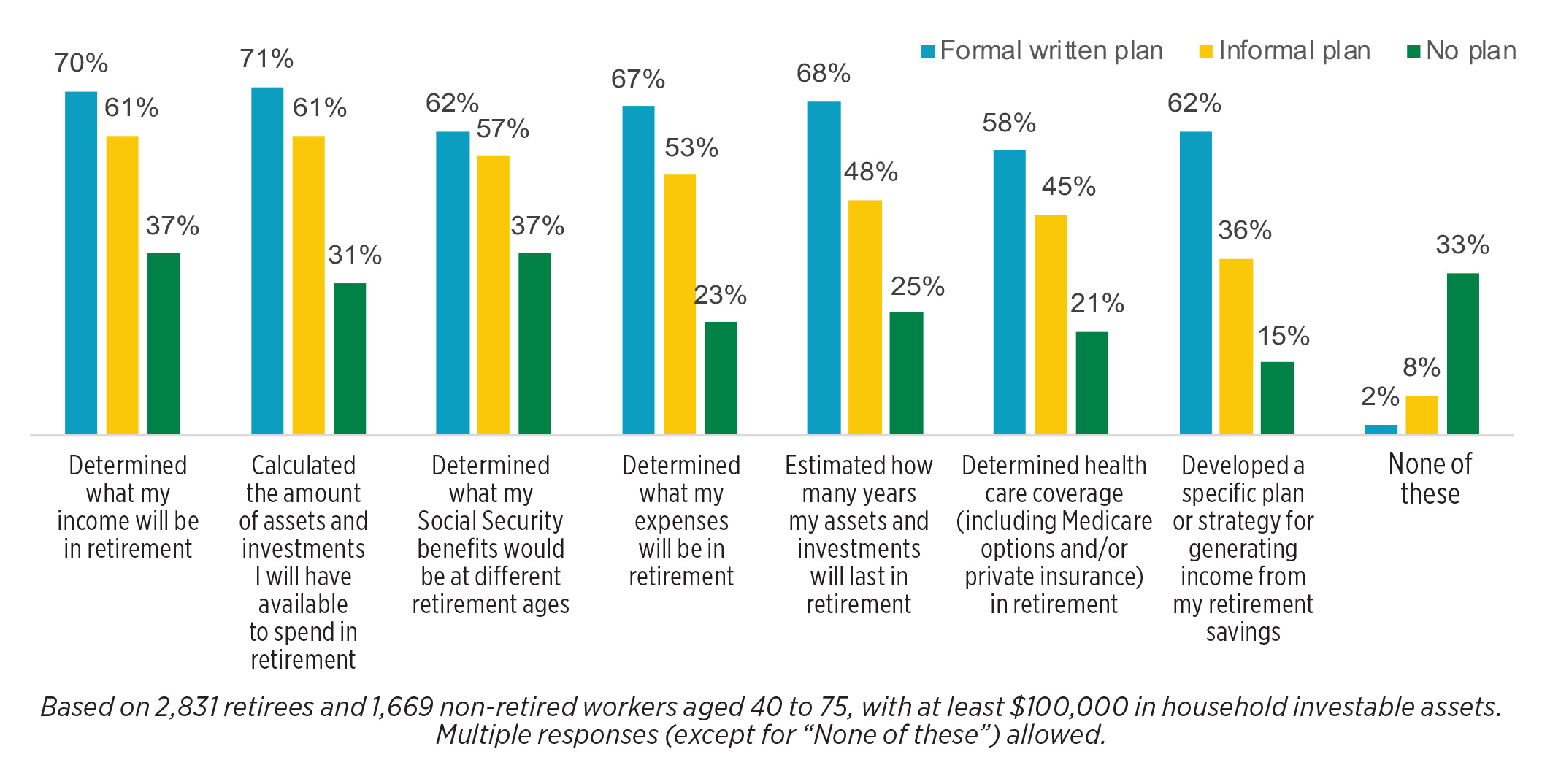

The research also indicates that working with a financial advisor correlates with more positive retirement experiences. About 60% of investors report they typically consult with an advisor on financial decisions, with higher percentages reported among investors who have more wealth. Advisors play a key role in creating a comprehensive, formal written plan for managing income, assets and expenses throughout retirement. Among investors who have these plans and are working with advisors, 94% of plans were created with an advisor’s help, suggesting that most investors are not willing or able to develop a truly comprehensive plan on their own.

Having a formal written plan is associated with completing key retirement planning activities, as opposed to having informal plans or no plan for retirement. When advisors develop formal written retirement plans for clients, retirees tend to rely on more varied, balanced sources of income as well as strategies such as annuitization that provide reassurance and stability in retirement. The ongoing value of advice is clear as personal responsibility for finances grows.

Planning for retirement timing is another crucial step that advisors can assist with. On average, current retirees report retiring around age 62, with the most common ages being 65 and 62. Younger retirements are aligned with benefit eligibility, while others retire as soon as they feel financially secure. Pre-retiree workers also signal an ongoing need for advice. Although most plan to retire by age 65, more than one-quarter envision working part time after age 65, which could be an unrealistic assumption given that few current retirees report earnings. Advisors can help clients determine whether projected resources truly support their desired retirement timelines based on individual circumstances.

As guaranteed income sources evolve and both retirees and workers transition to self-directed retirement models, advisor guidance on optimizing Social Security, annuitizing balances, managing nonqualified and qualified savings, and developing individualized income strategies becomes more imperative. Ongoing retirement education and support will remain important for clients of all stages, given the changing needs highlighted in LIMRA research.

Investors bullish on AI as a financial advisor tool

Catching up with the consumer in 2024

Advisor News

- What advisors should know about hedge funds in retirement planning

- Retirement control is top success measure for middle class, ACLI says

- Industry groups applaud House passage of Financial Exploitation Prevention Act

- Younger workers more likely to be eligible for a retirement plan after changing jobs

- Bank of America community event unpacks sales tax hike, small business struggles

More Advisor NewsAnnuity News

- Jackson Named InvestmentNews 2026 Annuities Provider of the Year

- State Farm’s agency overhaul: What distribution can learn

- IRI, ACLI express support for CLEAR Forms Act

- A new era at the Federal Reserve

- Globe Life Inc. (NYSE: GL) Making Surprising Moves in Tuesday Session

More Annuity NewsHealth/Employee Benefits News

- Pa., N.J. and Del. join multistate lawsuit against Trump administration over Medicaid work requirements

- Study Results from UNC Gillings School of Global Public Health Broaden Understanding of Managed Care (Days at Home among Children by Medical Complexity, Public/Private Insurance, and Urban/Rural Residence): Managed Care

- Reports from New York University (NYU) Add New Data to Findings in Managed Care (HealthySteps Comprehensive Services and Preventive Care: A Medicaid Claims Analysis): Managed Care

- 15 Maryland laws taking effect July 1 that you should know

- States take Trump administration to court over Medicaid rule

More Health/Employee Benefits NewsLife Insurance News

- Never stop learning: A lesson for the next generation of advisors

- Jackson Named InvestmentNews 2026 Annuities Provider of the Year

- Corebridge adds index strategies, growth potential to Max Accumulator+ III

- Estate planning 2.0: How ILITs can create liquidity

- AM Best Affirms Credit Ratings of Misr Insurance Company

More Life Insurance News