Legacy Planning with Deferred Annuities

Using a Revocable Trust to Give the Gift of a Guaranteed Income

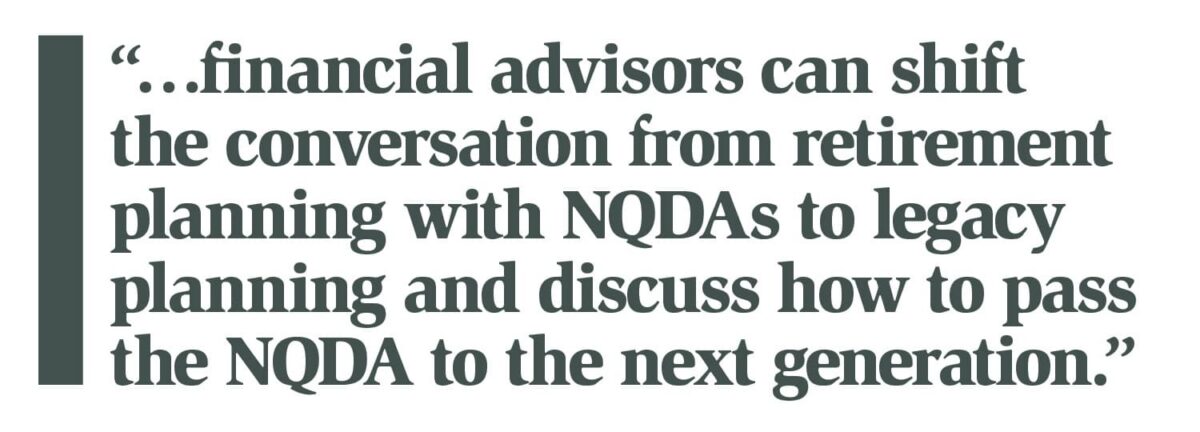

Two of the most common reasons retirees and pre-retirees engage a financial professional are to assess their level of retirement savings and to learn about options to save and invest outside of their employer-sponsored retirement plan.1 For those retirees who planned ahead and previously purchased a non-qualified deferred annuity (NQDA), some may find themselves in the enviable position of not needing their NQDA for their own retirement security. With these fortunate individuals, financial advisors can shift the conversation from retirement planning with NQDAs to legacy planning and discuss how to pass the NQDA to the next generation.

Imagine a parent (Suzy) who purchased an NQDA in her 50s for $100,000. Now in her 70s, Suzy has been happily retired for a few years and does not anticipate needing to access the nearly $265,000 in her NQDA. Suzy has two children, Mark and Mindy. Mindy is a public high school teacher and has access to a pension plan and has also saved for retirement through voluntary contributions to an employer plan. Mark has been an entrepreneur all of his life and has a spattering of thinly funded retirement accounts and IRAs with multiple custodians. After discussing the options with her financial professional, Suzy decides that the NQDA would better serve its purpose of providing guaranteed income in retirement for Mark.2

Imagine a parent (Suzy) who purchased an NQDA in her 50s for $100,000. Now in her 70s, Suzy has been happily retired for a few years and does not anticipate needing to access the nearly $265,000 in her NQDA. Suzy has two children, Mark and Mindy. Mindy is a public high school teacher and has access to a pension plan and has also saved for retirement through voluntary contributions to an employer plan. Mark has been an entrepreneur all of his life and has a spattering of thinly funded retirement accounts and IRAs with multiple custodians. After discussing the options with her financial professional, Suzy decides that the NQDA would better serve its purpose of providing guaranteed income in retirement for Mark.2

As the owner and annuitant of her NQDA, Suzy has a couple of different options to achieve her objective. Let’s explore a potentially tax efficient way for Suzy to make the transfer of her NQDA to her son, Mark.3

First, Suzy would fill out the appropriate paperwork at the insurance carrier to change the annuitant of the contract to Mark. By making Mark the annuitant, his life will ultimately be determinative of any future life-contingent annuity payout benefits provided by the NQDA so that future payments can provide him with lifetime income in retirement and so that, after the second step, only Mark’s death would trigger a death benefit.

Second, Suzy would change the owner (and beneficiary) of the NQDA contract to her revocable living trust (RLT). It is important that Suzy complete these steps in this order because many NQDAs do not allow an annuitant change when the annuity contract is owned by a non-natural person, like a trust. If allowed, an annuitant change when the annuity contract is owned by a non-natural person would require the NQDA to begin distributions or lose the tax deferral for its accumulated earnings.4 Note that generally there is neither income tax nor transfer tax consequences when an individual transfers an asset into or out of their RLT.5

Ultimately, as the trustee of her RLT, Suzy remains in control of the NQDA during her life — maintaining access to its account value in case she’s ever in a pinch or if her plans change. Further, Suzy could authorize a successor trustee to exercise ownership rights over the NQDA in case she is incapacitated in the future. For example, the successor trustee could change the investment allocations in Suzy’s fixed-indexed annuity (FIA) or registered index-linked

annuity (RILA) as the successor trustee deemed prudent.

Assuming that Mark is alive, Suzy’s death will not trigger a death benefit. This is because it is the life of the annuitant (Mark) that determines whether a death benefit is payable. The NQDA remains intact. Also, at Suzy’s death, her RLT will become an irrevocable, non-grantor trust. At this point, the NQDA is still owned by the trust, the trust is still the beneficiary of the NQDA, and Mark is still the annuitant.

Assuming Mark is a trust beneficiary, or a member of a class of trust beneficiaries, and certain other trust provisions are present, the successor trustee of the trust can make an in-kind distribution of the NQDA to Mark, allowing him to become the new owner of the annuity contract.6 Ideally, the terms of the trust will grant the trustee the discretion to distribute trust principal to Mark and the authority to make distributions of assets in-kind (which virtually all trustees will have).

If mandatory distributions depend on the age of a trust beneficiary, the trustee will have to ascertain whether/when distribution of the entire NQDA would be possible. If discretionary distributions are limited to a HEMS (health, education, maintenance, or support) standard, the in-kind distribution of the NQDA may not be permitted.7

In most cases, the in-kind distribution of the NQDA from the trust to Mark should not be a taxable transaction, and the investment in the contract immediately prior to the distribution will be Mark’s carryover basis in the annuity contract. The taxation of non-grantor trusts can be a fairly intimidating topic. However, in-kind distributions of assets from such trusts are a little less so. In Private Letter Ruling (PLR) 1999050151, the Internal Revenue Service found that an in-kind distribution of a NQDA from an irrevocable, non-grantor trust to a trust beneficiary was not a transfer of an annuity contract “without full and adequate consideration” and thus was not taxable.8

As the new owner of the NQDA, Mark should name an appropriate beneficiary and will be able to exercise all the rights of ownership.

Mark has inherited a valuable and versatile asset to aid him in his retirement, which can be annuitized to provide income for him for life based on his age and his life expectancy. It’s a wonderful gift to have received from his mother.9 And, depending on the type of NQDA and the success of Mark’s investment choices, the value of his NQDA will likely far surpass the $265,000 contract value at the time Suzy transfers it to her trust, and play a significant role in allowing Mark to achieve a safe and secure financial future.

The wealth transfer potential of NQDAs should not be overlooked. Suzy and her advisor were able to accomplish a valuable shift in the function of the NQDA in her overall financial plan: From retirement asset to legacy asset, and, in so doing, will provide a meaningful and substantial gift to her son. The ability to impact the financial security of multiple generations with a single asset is a gift that is worth giving, and one that will hopefully serve to reinforce family financial values that include responsibility, prudence, and generosity.

Find out more

To learn more about how we can help, visit

www.massmutualascend.com.

1. Employee Benefit Research Institute/Greenwald Retirement Confidence Survey 2025.

2. Note, if Suzy is currently married and has ever lived in a community property state during her marriage, spousal consent may be required to name a beneficiary other than her spouse.

3. This article assumes that Suzy has an “owner-driven” annuity contract. An “annuitant-driven” annuity contract may have different considerations. This article also assumes that the NQDA does not have a living benefit rider or death benefit rider that would be negatively affected by the proposed use of the NQDA. It is also important to ascertain with the insurance carrier that certain contract changes are allowable as different carriers may have different practices.

4. See I.R.C. § 72(s)(7).

5. See Rev. Rul. 85-13, 1985-1 C.B. 184.

6. If a charitable organization is also a beneficiary of the trust, an attorney should be consulted to determine whether the NQDA is eligible for tax deferral after Suzy’s death. See IRC 72(u)(1).

7. The trustee of the now irrevocable non-grantor trust should seek the opinion and guidance of an attorney to resolve the various legal, tax, and factual issues presented by making an in-kind distribution of a NQDA contract.

8. Although other taxpayers cannot rely upon PLRs, they do provide insight into the position of the IRS on various issues.

9. Alternatively, Mark may decide to name his spouse as a joint owner and/or as a joint annuitant and thus achieve other valuable planning objectives.

Rethinking the Return on Time

Adapt or Die – HNW and UHNW Clients Need Intentional Coordination

Advisor News

- Guaranteed income streams help preserve assets later in retirement

- Economic pressures make boomerang living the new normal

- Pay or Die: The scare tactics behind LA County’s Measure ER tax increase

- How to listen to what your client isn’t saying

- Strong underwriting: what it means for insurers and advisors

More Advisor NewsAnnuity News

- Guaranteed income streams help preserve assets later in retirement

- MassMutual turns 175, Marking Generations of Delivering on its Commitments

- ALIRT Insurance Research: U.S. Life Insurance Industry In Transition

- My Annuity Store Launches a Free AI Annuity Research Assistant Trained on 146 Carrier Brochures and Live Annuity Rates

- Ameritas settles with Navy vet in lawsuit over disputed annuity sale

More Annuity NewsHealth/Employee Benefits News

- The Medicare rules agents would repeal tomorrow

- FACT CHECK: ASHLEY HINSON VOTED TO SPIKE HEALTH INSURANCE COSTS, CUT VA FUNDING WHILE HER NET WORTH IN CONGRESS SOARED

- Judge rules some evidence admissible in Luigi Mangione murder case

- New cap on split costs for patients

- Researchers from University of South Carolina Provide Details of New Studies and Findings in the Area of Opioids (Trends in Medicaid managed care benefits for opioid use disorder treatment, 2015-2019): Opioids

More Health/Employee Benefits NewsLife Insurance News

- $150M+ asset sale payout distributed to Greg Lindberg policyholders

- Best’s Market Segment Report: AM Best Revises Outlook on France’s Non-Life Insurance Segment to Stable from Negative, Reflecting Top-line Growth, Technical Profitability

- Pacific Life Launches New Flagship Variable Universal Life Insurance Product

- NAIFA launches “NAIFA Cares” initiative to help build long-term financial security for children

- The fiduciary standard for life insurance is here

More Life Insurance News