When Term Life Insurance Scores A Touchdown

By David Szeremet

The University of Alabama’s head football coach, Nick Saban, is stockpiling success. He has led teams to five national championships – four as coach with the Crimson Tide and one when he coached at Louisiana State University. He has two AP Coach of the Year and four Southeastern Conference Coach of the Year honors to his credit. And there is even chatter about erecting a statue in his honor.

So what do you get for the coach who has it all? Term life insurance, of course.

In June 2014, The University of Alabama and Nick Saban agreed to a contract extension which runs through 2020. Because he is an employee of a public university, his contract extension was made available to the public. It includes, among other things, a term life insurance fringe benefit. Here is how it works.

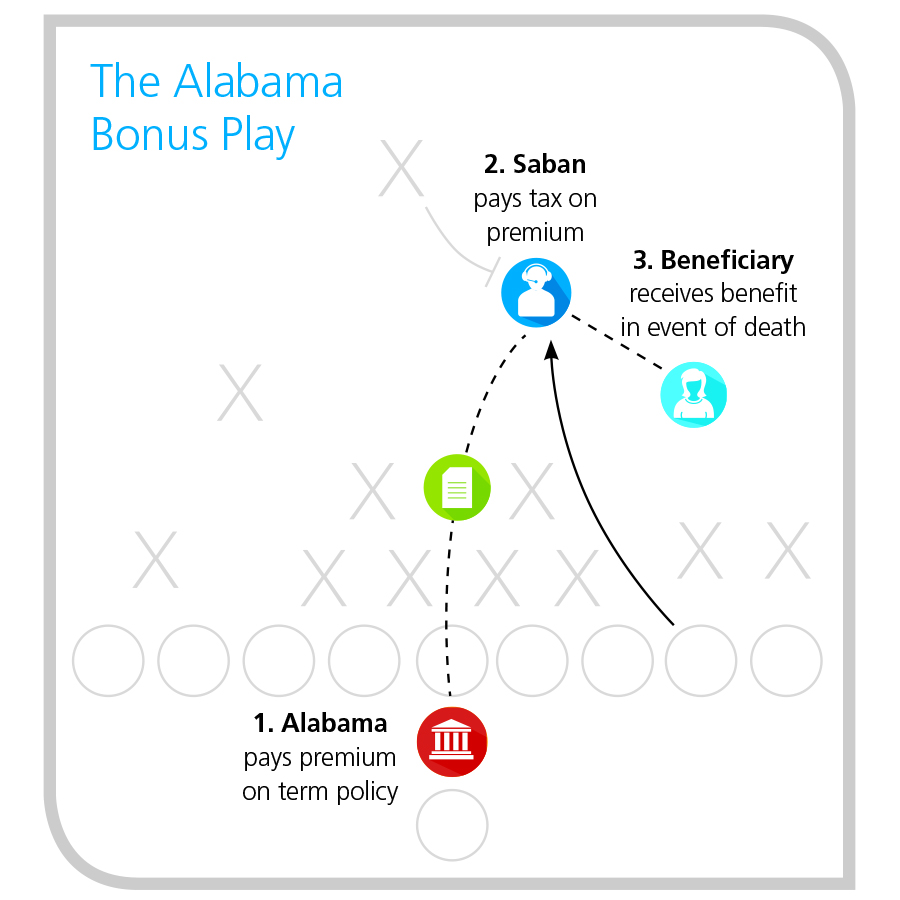

- The University of Alabama buys a $5 million term life policy on his behalf.

- Saban owns the life insurance policy and selects his beneficiary.

- While the employment contract is in effect, the university will pay each annual policy premium on Saban’s behalf.

- In the event of Saban’s death, the death benefit pays income-tax-free to his beneficiary.

The annual premium paid by the university is treated as taxable compensation to Saban. In essence, it is a retention bonus payment. The university is using the life insurance bonus as a compensation “sweetener” to retain and reward Saban.

Although the Saban case involves a college football coach, the term insurance bonus concept is commonly used in the business community. Think of Saban as a key employee of The University of Alabama’s football program. The term insurance bonus is one of his fringe benefits. This concept is appropriate for executives, officers, managers or key employees where a benefit above and beyond (or instead of) group term insurance is desired.

A term life insurance bonus delivers six primary benefits:

- An affordable fringe benefit (depending on age, health and other underwriting factors).

- Income tax-free death benefit protection.

- A portable benefit.

- Potential for a conversion feature to provide permanent, lifetime protection (depending on the policy.)

- The most death benefit protection at the lowest price (during the level term period).

- A simple concept to understand.

A term life insurance bonus can be established for a single participant (such as the Saban case) or for a group or class of employees. In a typical plan, select management-level employees are offered the term insurance fringe benefit.

Going for two

Because the term insurance bonus payment is considered taxable income, an employer may choose to offer a “double bonus.” Under a double bonus, an additional payment is made to cover the income tax exposure to the executive. This ensures that the executive does not have to reach into their own pocket (or the funding mechanism) to pay the tax.

What about permanent life insurance?

Permanent life insurance takes the bonus concept to the next level. Adding cash value to the equation gives the key employee another powerful reason to excel and stick with the employer for the long run. After all, cash is king. The cash value can be tapped as a tax-appropriate rainy day fund or retirement supplement.

Taking home the trophy

As the Saban case demonstrates, term life insurance can be an attractive fringe benefit. Virtually any business entity can benefit from the concept and it should not be overlooked. Business owners could learn from The University of Alabama and apply the same concept to their key employees.

Preparing for next season

Not to be outdone, Dabo Swinney, the coaching rival Saban lost to in the 2017 National Championship game, also has a $5 million term life insurance policy benefit as part of his contract with the Clemson Tigers (Swinney's contract was also made public.) Yet another winning reason to consider a term life insurance policy when looking to retain and reward key people.

David Szeremet, J.D., CLU, ChFC, is second vice president, advanced planning, at Ohio National Financial Services. He may be contacted at [email protected].

DOL Rule Confusion Leads to Wait-and-See Approach

eApps Make Inroads, Reduce Cycle Times

Advisor News

- How can more Americans achieve financial independence?

- Savers vs. spenders: How money management attitudes impact financial confidence

- Demonstrating the value of life insurance to Gen Z

- Poor money habits are a dealbreaker in a new relationship

- DC plan sponsors see opportunity in alternatives

More Advisor NewsAnnuity News

- The next growth phase in life/annuities depends on modernization

- CA judge certifies class action in teachers’ lawsuit over in-plan annuity fees

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Managing Director Joins ‘Target Topics’ Podcast to Discuss State of Delegated Underwriting Authority Enterprises Market

- KBRA Assigns Rating to TruSpire Retirement Insurance Company

More Annuity NewsHealth/Employee Benefits News

- Findings from Yonsei University Advance Knowledge in Demography (Different Understandings of Scientific Research in the Use of De-identified Personal Sensitive Data: South Korea, in Comparative Perspectives): Science – Demography

- Data on Influenza Vaccines Discussed by Researchers at University of Lucerne (Keep Reminding Me To Get My Flu Shot): Immunization and Public Health – Influenza Vaccines

- Bobby Harrison: Rising insurance exchange costs bad for working poor

- New Managed Care Findings from Brown University Reported (Prior Authorization In Medicare Advantage: Beneficiary Exposure And Plan Disenrollment In 2021): Managed Care

- Findings on Managed Care Detailed by Researchers at Renal Research Institute (AI-Driven Interventions for Imminent Hospital Admissions in Patients with End-Stage Kidney Disease: A Medicare and EMR-Based Analysis): Managed Care

More Health/Employee Benefits NewsProperty and Casualty News

- Wright National Flood Insurance Company announces agreement with First Insurance Co. of Hawaii: Wright National Flood Insurance Company

- American Integrity Founder and CEO Bob Ritchie Named PropertyCasualty360’s 2026 Thought Leader of the Year

- Federato Research: 91% of P&C Leaders Report Real-Time Portfolio Control, Only 27% of Underwriters Say the Same

- High cost of home insurance may drive voter turnout for midterms

- Secretary of State says insurance reforms are not political

More Property and Casualty News