Tech Seen As Top Challenge In Life Insurance Industry, LIMRA Says

As COVID-19 prompted life insurance companies to accelerate their digital adoption to ensure continuity of business and serve their customers, it exposed the challenges of life insurers’ legacy systems, siloed operations and the continued need to modernize.

As a result, life insurance executives cited technology as both the top challenge facing their companies and the external force driving change in the industry, according to the latest C-suite life insurance executive survey by LIMRA and Boston Consulting Group (BCG)

The 2021 study surveyed more than 400 C-suite life insurance executives across 50 countries to identify their greatest challenges and conditions that affect their business strategies.

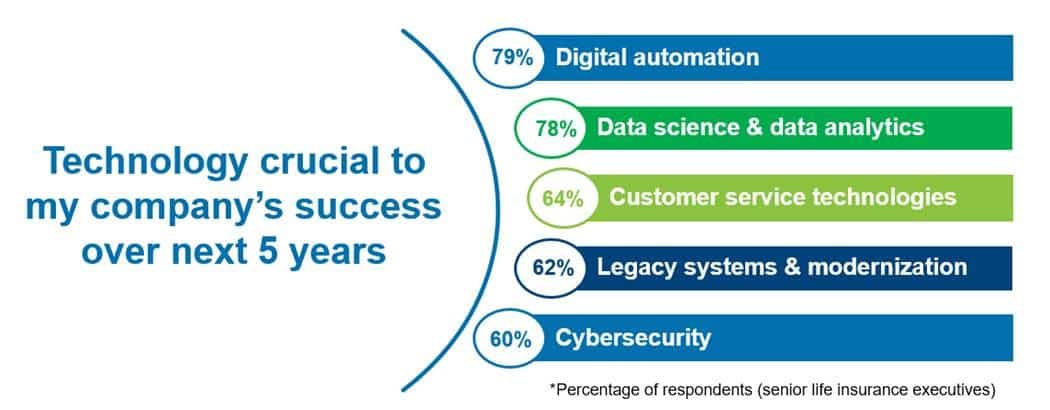

Nearly 4 in 10 executives said technology was their company’s greatest internal challenge — twice as many as in 2019 when the survey was last conducted. Executives surveyed said digital automation and data science and analytics were the top technologies needed to ensure their companies’ progress in marketing, distribution and customer experience over the next five years. Six in 10 respondents said investments in customer service technologies, modernizing legacy systems, and mitigating cybersecurity threats would be crucial to being competitive.

Other top challenges, like low interest rates and regulation, reflect the significant headwinds facing the industry and amplify the need to manage risks in the current environment. Additional priorities, such as growth and new ways of working, demonstrate how insurers are preparing for a future in which they move faster and are more responsive to customer, advisor and employee needs.

“The pace of change has accelerated in our industry and across the world, requiring life insurers to adjust their strategies to not only to meet current demands of today’s customers but also to ensure competitiveness in the decades to come,” said Alison Salka, Ph.D., senior vice president and director of LIMRA Research. “What has been a consistent challenge for the industry is the long-term, ultra-low interest rates. LIMRA studies show the industry has adapted to this ‘new normal’ by adjusting how they manage investments, assets and liabilities, or shifting their product portfolio to focus their growth strategies on protection products that are inherently less interest-rate sensitive.”

Future Of Work

COVID-19 also significantly shifted companies’ positions on the future of work. In addition to introducing the need for remote and hybrid work arrangements, COVID-19 also highlighted the need to adapt to the ever-growing, digitally based customer engagement. Two thirds of executives surveyed said embracing digital innovation would be most important to the future of work in the industry.

“The pandemic exacerbated the existing war for talent in the life insurance space, especially in the digital domain. To attract and retain talent, companies will need to make substantial investments in new technology and re-skilling current employees to capitalize on the capacity made available by the automation or elimination of manual processes,” noted BCG Managing Director and Partner Rob Sims.

The study revealed this workforce transformation will require meaningful changes in how employees are managed. Sixty percent of executives say the biggest challenges associated with change management will be cultural.

“Another often overlooked aspect of these changes is how they will impact companies’ cultural and management styles,” Sims says. “As companies strive to build an increasingly diverse, technology-empowered workforce, leaders will need to balance the best ways to leverage people and technologies to create the greatest efficiencies and engagement.”

The study provides three recommendations to help drive growth:

Expanding distribution models. Life insurers should not only expand into new models that bring life insurance to customers where they bank, shop, work or travel but they also must reimagine how advisors interact with customers and provide them the training and digital tools needed to support this.

Evolving value propositions and products. While persistent ultra-low interest rates have required life insurers to shift their portfolio to products that require less capital and minimize risk, companies should develop personalized solutions that add value in a customer’s daily life, creating greater loyalty and new opportunities.

Taking new approaches to engagement. Insurers are exploring new customer engagement approaches to tap into growth opportunities. From health and well-being products to rewards programs (such as Vitality or Dacadoo), worksite well-being programs, voluntary benefits and use of social media, companies can leverage these new strategies to capture more data and learn about customer preferences and refine their offerings.

To download the report, visit: What’s On the Minds of Life Insurance Executives: Responding to the Moment, Looking to the Future.

Combined Insurance Announces ‘Reinforce Your Workforce’ Initiative

Insurers Continue To Flirt With Electronic Health Records

Advisor News

- Americans aren’t turning retirement plans into action, LIMRA finds

- Ashley Hinson ‘death tax’ story collides with truth

- How advisors can prepare clients for an uncertain retirement landscape

- Investors aren’t waiting out uncertainty

- Transamerica and Advo(k)ate Advisors launch pooled employer plan

More Advisor NewsAnnuity News

- Jackson Financial CEO caps 40-year career with blockbuster Q2

- Lumos Insurance introduces the Immediate Care Plan to help families fund long-term care

- NAIC regulators begin consensus phase on annuity illustration overhaul

- AM Best Revises Outlooks to Negative for Subsidiaries of Group 1001 Insurance Holdings, LLC

- Market-value adjusted annuities: Key considerations for advisors

More Annuity NewsHealth/Employee Benefits News

- OCI PRESS RELEASE, AUGUST 5, 2026, BE AWARE OF ALTERNATIVE HEALTH INSURANCE PLANS

- HINSON INTRODUCES BILL TO HOLD BIG HEALTH INSURANCE ACCOUNTABLE

- Another 102 jobs cut as UCare liquidation continues

- California nearly achieved universal healthcare. Now, millions are losing coverage

- New York state made $21.6M in improper Medicaid payments

More Health/Employee Benefits NewsLife Insurance News

- Don't keep checks with clerical errors

- The insurance distributor that builds its own software will win the next decade

- iA Financial Group Reports Second Quarter Results

- Supporting small businesses starts with smarter benefits conversations

- Judge again tosses Penn Mutual whole life lawsuit alleging tax scam

More Life Insurance News