RILAs Take The FIA Road In This Crisis

Consumers are rushing to safety as they did early in the Great Recession, but they are running toward different products during this economic downturn – and that trend is likely to continue even in this ultralow rate environment.

That is one of the projections to expect from Todd Giesing, senior director, annuity research, Secure Retirement Institute, and Teddy Panaitisor, senior research analyst, SRI, during their session, “The Sky Is Falling – How Plunging Financial Markets Affect The Annuity Market” scheduled for Tuesday afternoon during LIMRA’s Life & Retirement Virtual Conference.

Although the title refers to plunging equity markets, the researchers said they would be focusing on what is happening with products now and projecting into the next few years if things remain fairly constant.

They see a softening annuity market for the rest of this year and next, with slow growth in 2022.

“We expect sales to be down in the 8% to 15% range for 2020 compared to 2019,” Giesing said. “What's interesting is this puts us in the same impact as we saw from the financial crisis in 2008. In 2009, where I believe sales were down 10 or 11%. When you start looking at the individual products, this is where we'll see some differences.”

One of those key differences is in variable annuities.

“It's much different today than it was in 2007, 2008, 2009,” Giesing said. “Actually, it was all variable annuities -- 72% of all sales in 2007. At the end of 2019, variable annuities only accounted for 42% of the share. The carriers have diversified their business.”

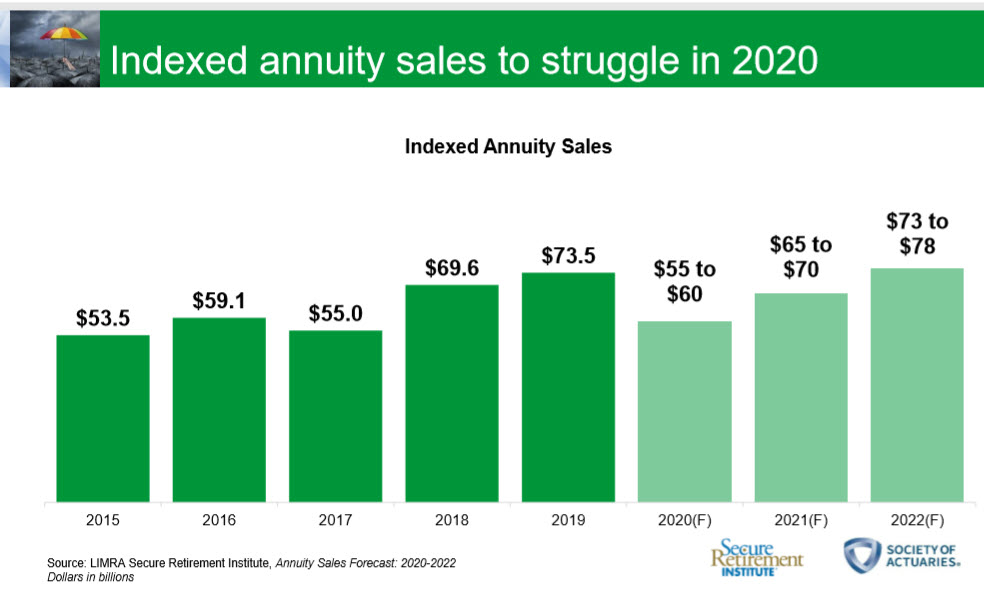

“We expect indexed annuities to be down 20 to 25%,” Giesing said. “There are many factors going on but it's basically difficult pricing environment for indexed annuities, which is making alternative solutions such as fixed rate deferred and registered indexed linked annuities more popular.”

FIAs require a longer holding period of at least several years, so consumers would be stuck with the low-rate product while other assets such as equities perform far better. Fixed-rate deferred annuities benefit by having the option of shorter durations of a few years.

“We expect fixed-rate deferred products to maintain or even grow slightly from last year,” Giesing said. “And last year was the highest year for fixed-rate deferred sale since the financial crisis. That’s the theme of protection. It's going to show up in fixed-rate deferred even though they're highly sensitive to interest rate changes.”

Even though the products’ rates are low, they serve as a safe place for consumers to land amid all the uncertainty.

“I think all of this is just putting individuals in a spot where they're just saying I just give me safety for a year or two or three,” Giesing said. “And for a portion of my money, we'll figure out in a couple of years what we're going to do from a longer term planning perspective.”

Other products with longer durations have not been faring as well.

“Income annuities are struggling because of the low interest rate environment and the pricing is way down on these products, and because they're irrevocable,” Giesing said. “We're under the assumption that advisors and clients are going to take a wait and see mentality, wait and see if things get better in six months or a year and then make the purchase at that point.”

Steven A. Morelli is editor-in-chief for InsuranceNewsNet. He has more than 25 years of experience as a reporter and editor for newspapers and magazines. He was also vice president of communications for an insurance agents’ association. Steve can be reached at [email protected].

© Entire contents copyright 2020 by InsuranceNewsNet. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.

Black Basketball Pro Turned Advisor Worried About ‘Clear Color Line’

Class Action Filed Against 11 Insurers For Pandemic Claim Denials

Advisor News

- How advisors can prepare clients for an uncertain retirement landscape

- Investors aren’t waiting out uncertainty

- Transamerica and Advo(k)ate Advisors launch pooled employer plan

- ‘I wish I’d met him sooner:’ Karlan Tucker remembered for integrity, faith

- Why women must be more engaged in investing

More Advisor NewsHealth/Employee Benefits News

- NEPA sees health insurance enrollment drop after enhanced subsidy cuts

- Abbott seeks thinner, cheaper health plans

- New Findings in Managed Care Described from Creighton University School of Medicine (Barriers beyond Medicaid: A Midwest study on pancreatic surgery access in the post-Affordable Care Act era): Managed Care

- Abbott’s 'Keep Texas Affordable' plan: Lower housing costs, new health insurance plan

- 1 in 4 American workers report staying in unwanted jobs for health insurance: West Health Institute

More Health/Employee Benefits NewsLife Insurance News

- Judge again tosses Penn Mutual whole life lawsuit alleging tax scam

- Declined by a machine? The end of the unexplainable no

- AM Best Revises Outlooks to Negative for Subsidiaries of Group 1001 Insurance Holdings, LLC

- Court sides with Ameritas in denying $4M STOLI payout to Wells Fargo

- AM Best Removes From Under Review With Positive Implications and Upgrades Credit Ratings of The Fortegra Group, Inc.’s Insurance Subsidiaries

More Life Insurance NewsProperty and Casualty News

- Abbott seeks thinner, cheaper health plans

- ADAMS, SNEED TO STUDY RISING HOMEOWNERS INSURANCE COSTS

- TDCI shares insurance tips for back-to-school season

- Travel insurance, entry rules and permits: here's what travelers miss when planning a dream vacation

- Everspan Group Expands Leadership Team with Three Senior Appointments

More Property and Casualty News