Regulators give insurers a break on reporting interest rate losses

State insurance regulators voted Sunday to adopt a key rule change on how insurers report interest rate-related losses.

An industry trade group lobbied for the rule change, which Reuters reports will free up hundreds of millions of dollars that insurers can use to write new policies or reinvest in business innovation.

The change is to the interest maintenance reserve [IMR], an accounting standard that helps carriers smooth their annual income across market conditions, according to a recent Conning report. IMR is a reserve held according to standard accounting principles to deal with fluctuations in the interest rate.

Now the 30-year-old IMR standard is traversing rough terrain in an environment of rapidly rising interest rates. Carriers’ IMR balances can drop further as they trade their old bonds for new. This erodes their interest maintenance reserve into negative territory, which is not allowed under IMR standards. It’s a particular problem for public companies accountable to shareholder demands.

Reuters reports that at least 23% of life insurers rated by credit ratings agency Fitch stand to benefit, because their IMR reserves were negative as of the end of December.

The change, as adopted by the Statutory Accounting Principles Working Group, will allow insurers to realize some of their losses over time rather than immediately. The working group is part of the National Association of Insurance Commissioners, which held their summer meeting over the weekend in Seattle.

IMR changes will expire at the end of 2025 unless a long-term solution is adopted, regulators said.

"We'd really like to thank regulators for working with us on an interim solution to not disincentive prudent investment or risk management activity until a longer-term solution can be finalized," said Mike Reese of Northwestern Mutual, who represented the American Council of Life Insurers.

ACLI lobbied the working group for the rules change.

Interest rate impact

The Conning report, released this spring, highlighted the difficulties insurers are having with IMR.

“A desire to avoid having negative IMR may make insurers increasingly reluctant to trade as they seek to minimize losses and even forgo opportunities that could benefit their long-term economic value,” according to the Conning report, “As Rates Rise, Investment Strategies Must Meet IMR Challenges.” “It has become abundantly clear that accounting for IMR is now a vital constraint that insurers must incorporate when managing their portfolios and setting investment strategy, adding another level of complexity to the process.”

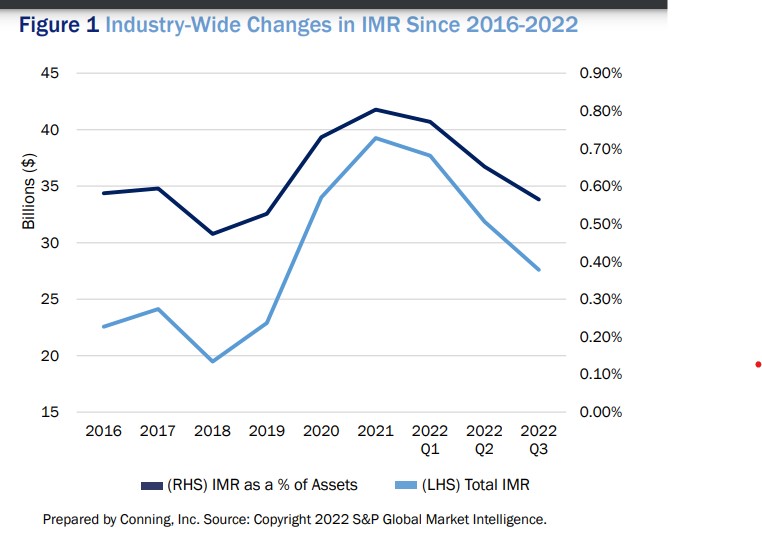

Even in the low-interest rate environment, things were going well for carriers’ interest maintenance reserves. Between 2018 and 2021, the industry’s IMR doubled from $19.5 billion to $39.3 billion, according to Conning.

Rising interest rates in 2022 choked off that increase and is eating into the reserve. Last year, 61 carriers went from a positive IMR to zero.

“Many insurers risk their IMR balances shrinking further or even turning negative should they continue to sell bonds in pursuit of higher yields,” according to the article.

Senior Editor John Hilton covered business and other beats in more than 20 years of daily journalism. John may be reached at [email protected]. Follow him on Twitter @INNJohnH.

© Entire contents copyright 2023 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

Annuities: Maximizing retirement income in 2023 and beyond

New York state proposes rules for pharmacy benefit managers

Advisor News

- How can more Americans achieve financial independence?

- Savers vs. spenders: How money management attitudes impact financial confidence

- Demonstrating the value of life insurance to Gen Z

- Poor money habits are a dealbreaker in a new relationship

- DC plan sponsors see opportunity in alternatives

More Advisor NewsAnnuity News

- CA judge certifies class action in teachers’ lawsuit over in-plan annuity fees

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Managing Director Joins ‘Target Topics’ Podcast to Discuss State of Delegated Underwriting Authority Enterprises Market

- KBRA Assigns Rating to TruSpire Retirement Insurance Company

- Partial annuitization: How advisors can help clients balance income, growth

More Annuity NewsHealth/Employee Benefits News

- They harvest the nation’s food, but a new rule may strip them of health insurance

- NEW DATA SHOWS 5 MILLION AMERICANS LOST HEALTHCARE THANKS TO GARRITY-BACKED CUTS

- Get Your Kids Ready to Go Back-to-School with Affordable Health Coverage

- STACY GARRITY SUPPORTS SKYROCKETING HEALTHCARE COSTS AND 160,000 PENNSYLVANIANS LOSING THEIR HEALTHCARE

- NEW DATA: ROB BRESNAHAN-BACKED HEALTHCARE CUTS CAUSE MORE THAN 10,100 PENNSYLVANIANS IN NEPA TO DROP INSURANCE COVERAGE

More Health/Employee Benefits NewsLife Insurance News

- How can more Americans achieve financial independence?

- AM Best Assigns Credit Ratings to MAAGAP Insurance Inc.

- Critical care riders: the living benefit more clients should understand

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Upgrades Credit Ratings of Sagicor Financial Company Ltd. and Most of Its Subsidiaries

More Life Insurance News