Now really is the time to invest in online ecosystems

It’s no secret that the COVID-19 pandemic brought immense changes to all Americans’ lives. For many, one of those changes was a heightened awareness of the need to protect their families against unforeseen circumstances. This significantly increased their intent to purchase life insurance.

This heightened awareness of life insurance — and how it can provide financial security for families — did translate into increased sales in 2022. According to the 2023 Insurance Barometer study, conducted by LIMRA and Life Happens, slightly more than half (52%) of American adults say they own some form of life insurance coverage (individual, employer sponsored, etc.). This is up from 50% in the 2022 Insurance Barometer study.

As we move into what I’m tentatively calling the “post-pandemic” world, what now? What are some of the lasting effects the pandemic will have on our industry and how advisors work?

I am not in the business of predictive sales models, but I am in the business of measuring consumer attitudes and behaviors — specifically concerning all things life insurance.

There are two seismic shifts occurring that will have a profound effect on the way we do business:

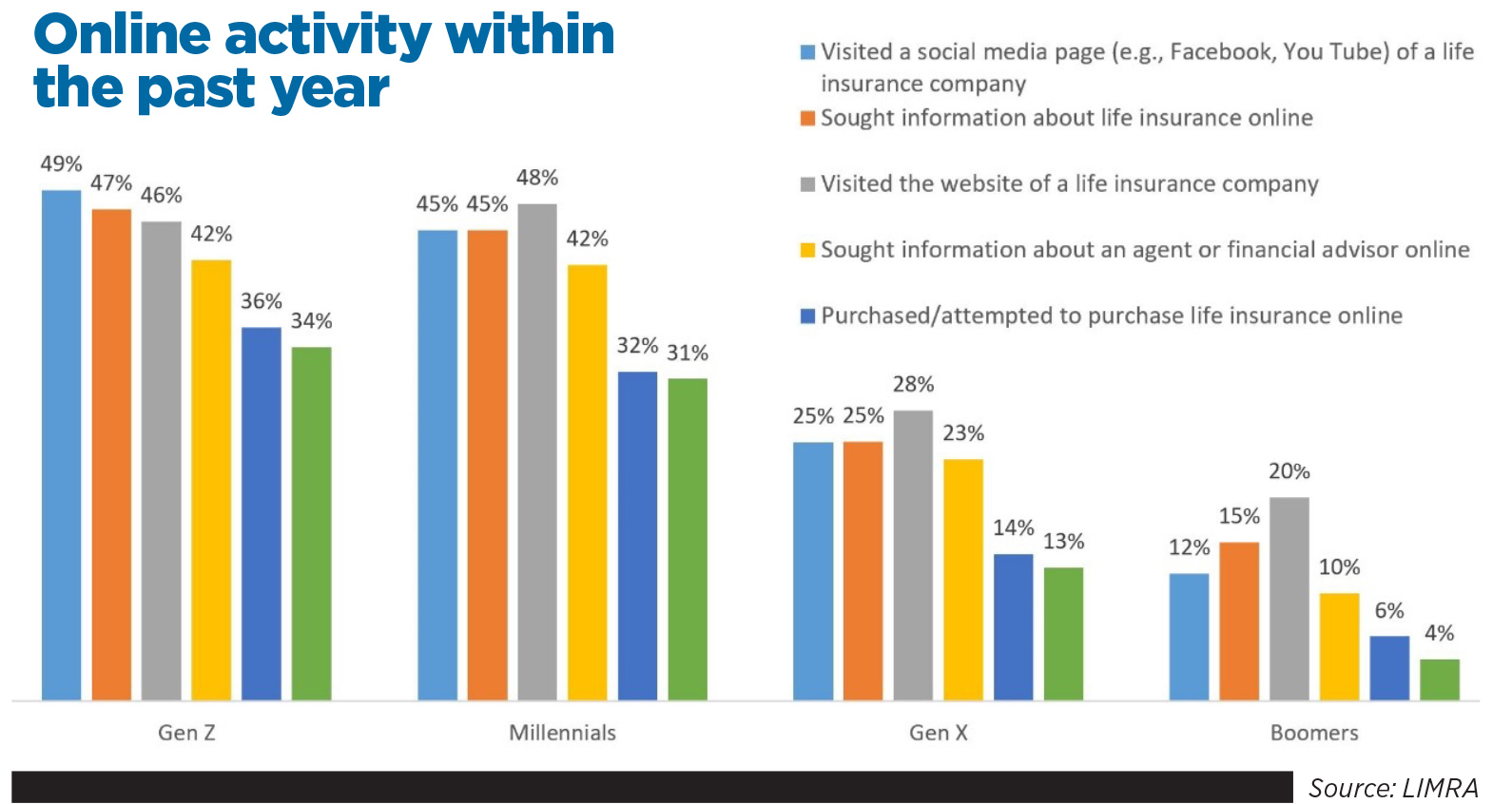

» Millennial and Generation Z consumers who grew up with access to the internet are at or approaching the ideal age to seriously think about individual life insurance policies.

» The pandemic forced almost all of us into online consumerism and transactions.

Every company has a website, and many have a social media presence. But is it enough?

Historically, the majority of Americans have preferred to purchase life insurance in person with an agent or advisor. As the use of technology has become nearly ubiquitous and people have grown accustomed to conducting meetings and transactions online, this trend has shifted. In 2011, 64% of consumers said they preferred to buy in person; by 2020, only 41% felt this way.

In 2022, that number dropped to 33%.

Conversely, the idea of shopping and purchasing entirely online has gained in popularity every year — exacerbated by the pandemic. When we look at the generational differences, this shift becomes more pronounced. When the 8,185 Barometer study respondents were asked how the internet would factor into their buying process, only 5% of those under 40 said it would not have an impact at all.

It’s important to note that of those who indicated they had sought information about, purchased or attempted to purchase life insurance online, more than 60% said that they used a comparison tool such as SelectQuote or AccuQuote to better understand what they were shopping for.

As you can see, younger generations rely on the internet for information gathering and shopping.

Participating in online meetings via video software and apps has become part of their daily lives.

Just as with other industries, financial services companies and financial professionals must make a concerted effort to become more accessible online.

Consumers most often mentioned the need for life insurers to be “more personable” online.

Although “easier navigation” and “better comparison charts” are necessary, features such as live chat with knowledgeable staff and “policy quotes with clear explanations” speak to the expectation that online shopping and sales will replace face-to-face meetings in the future.

None of this should come as a shock to the life insurance industry or financial professionals. But it should spur discussion and potential investment for many. This shift is happening faster than many of us could have anticipated. It is safe to say that not keeping up with online technology may result in missed opportunities and sales.

Consumers routinely purchase houses, cars and fresh vegetables online. Many doctor’s visits now occur online. Why should buying life insurance be any different?

Disability income insurance in a gig economy

Life insurance companies ready for analysts to pick apart Q1 earnings

Advisor News

- How can more Americans achieve financial independence?

- Savers vs. spenders: How money management attitudes impact financial confidence

- Demonstrating the value of life insurance to Gen Z

- Poor money habits are a dealbreaker in a new relationship

- DC plan sponsors see opportunity in alternatives

More Advisor NewsAnnuity News

- The next growth phase in life/annuities depends on modernization

- CA judge certifies class action in teachers’ lawsuit over in-plan annuity fees

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Managing Director Joins ‘Target Topics’ Podcast to Discuss State of Delegated Underwriting Authority Enterprises Market

- KBRA Assigns Rating to TruSpire Retirement Insurance Company

More Annuity NewsHealth/Employee Benefits News

- People with this Medicare plan could soon go out-of-network at UHealth hospitals

- Findings from Yonsei University Advance Knowledge in Demography (Different Understandings of Scientific Research in the Use of De-identified Personal Sensitive Data: South Korea, in Comparative Perspectives): Science – Demography

- Data on Influenza Vaccines Discussed by Researchers at University of Lucerne (Keep Reminding Me To Get My Flu Shot): Immunization and Public Health – Influenza Vaccines

- Bobby Harrison: Rising insurance exchange costs bad for working poor

- New Managed Care Findings from Brown University Reported (Prior Authorization In Medicare Advantage: Beneficiary Exposure And Plan Disenrollment In 2021): Managed Care

More Health/Employee Benefits NewsLife Insurance News

- Best’s Market Segment Report: AM Best Maintains Stable Outlook on South Korea’s Non-Life Insurance Market

- Horace Mann Strengthens Customer Relationships and Accelerates Long-Term Growth Through Transactions with Medical Mutual of Ohio

- Regulators: ‘No firm conclusions’ from first offshore reinsurance filings

- Allianz Life Study Finds Americans Struggle to Shift From Retirement Saving to Spending

- The next growth phase in life/annuities depends on modernization

More Life Insurance News