LIMRA/SOA study: Fixed-rate deferred annuitants are not surrendering early

Insurance companies generally prefer that annuity contract holders do not surrender their contracts.

While a surrender charge penalty would apply, and some of those who surrender an annuity are doing so to buy another annuity, insurers prefer the stability of a long-term contract holder.

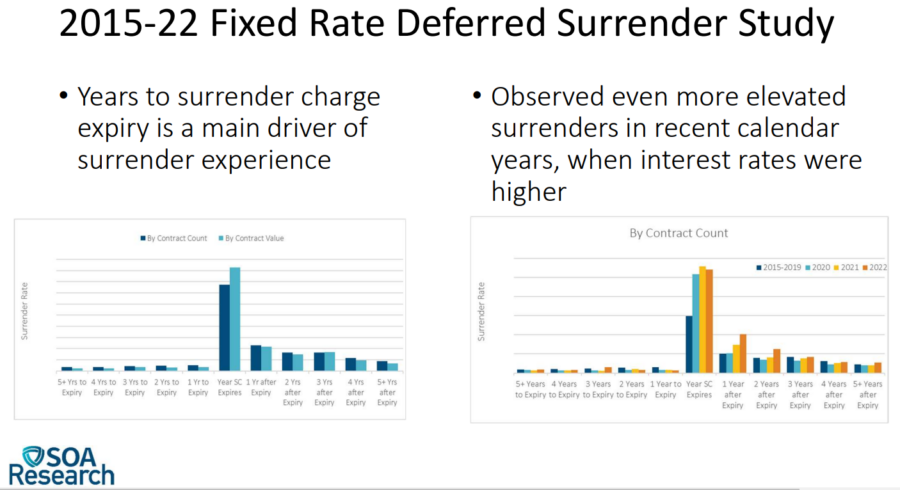

A new study by the Society of Actuaries and LIMRA found that most fixed-rate deferred annuity owners are at least waiting until their surrender charge period is up before surrendering. The two organizations jointly studied fixed-rate deferred annuity surrenders covering 2015 through 2022.

Dale Hall, managing director of research for the SOA, shared the data with insurance regulators Sunday during the National Association of Insurance Commissioners' summer meeting in Chicago. Hall presented to the Life Actuarial Task Force.

"In the previous studies, I think you'd see higher levels of contract surrenders even two years to expiry, one year to expiry of the surrender charge," Hall explained. "It seems like more and more of that focus is now in the year the surrender charge. ... Maybe it's more information or guidance, or policyholders just more apt to hold on to the contract to the full time when there's a much lower if no surrender charge."

Advisors often counsel patience to avoid a surrender situation.

Surrender rates by both contract count and contract value peaked in the year the surrender charge expired, at a rate of 38.6% by contract count and 46.3% by contract value, the study found. After that year, surrender rates remained elevated since there continued to be no surrender charge in the successive years.

Twenty-three companies contributed data to the current study, encompassing approximately 45% of fixed-rate deferred annuity market share during 2015-2022, SOA said. The study contains about 13.4 million contract count exposed, $1 trillion in contract value and more than 900,000 surrenders.

Higher surrender rates

Surrender rates in 2020, 2021 and 2022 were "significantly higher" in the year the surrender charge expired compared to surrender rates in 2015-2019, SOA reported. Surrender rates by contract count in the year the surrender charge expired were 51.7% for 2020, 55.7% for 2021, 54% for 2022 and 29.7% for 2015-2019; surrender rates by contract value in the year the surrender charge expired were 62.8% for 2020, 66.5% for 2021, 66% for 2022 and 33.7% for 2015-2019.

"Surrenders became much a little bit more prominent, relatively, in the more recent environment, obviously driven a lot by strong movements in interest rates and strong opportunities, perhaps for higher accredited rates coming out of that in those particular environments," Hall said.

Some additional highlights from the LIMRA/SOA study of surrenders:

• There was more nonqualified experience in the study, with 57.6% of contracts, compared to

traditional and Roth IRA experience.

• Females represented a larger percentage of the study in force than males in all market types

(traditional IRA, nonqualified, and Roth IRA), with females making up between 54-57% of

contracts depending on market type.

• The career agent distribution channel dominated the FRDA market for traditional IRA and Roth IRA market types, with 38.8% and 72.3% of contracts, respectively. The bank/savings and loan distribution channel had the largest percentage of contracts in the nonqualified market type, with 23.7% of contracts.

• The surrender rates by both contract count and contract value were relatively stable across

attained age groups 60-64 and older. The surrender rates for attained ages under 60 were the

lowest of all attained age groups.

• Surrender rates by individual contract year show "shocks" in the surrender rates in contract years 4, 6, 8 and 11, which correspond with common surrender charge periods of 3, 5, 7 and 10 years.

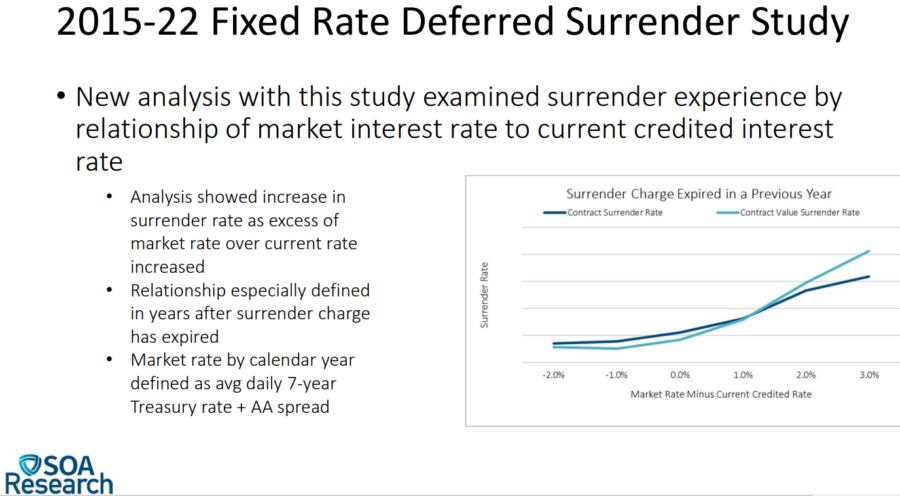

• When examined by grouped calendar years of study experience, calendar year group 2015-2017 experienced much lower surrender rates overall compared to the experience for calendar year group 2018-2022. The highest "shock" surrender rate occurred in contract year 6 for calendar year group 2018-2022, with surrender rate by contract count of 33.4% and surrender rate by contract value of 40.3%. In comparison, the surrender rate for calendar year group 2015-2017 in contract year 6 was 10.2% by contract count and 10.6% by contract value.

• When examined by individual contract year and surrender charge expiry timing, contract year 6 had the highest surrender rate by far for contracts in the year the surrender charge expired, at 59.1% by contract count and 68.7% by contract value.

© Entire contents copyright 2024 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

California to fast track rate review process in bid to improve insurance crisis

STLDI plans banned in Illinois: What advisors must know

Advisor News

- How can more Americans achieve financial independence?

- Savers vs. spenders: How money management attitudes impact financial confidence

- Demonstrating the value of life insurance to Gen Z

- Poor money habits are a dealbreaker in a new relationship

- DC plan sponsors see opportunity in alternatives

More Advisor NewsAnnuity News

- The next growth phase in life/annuities depends on modernization

- CA judge certifies class action in teachers’ lawsuit over in-plan annuity fees

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Managing Director Joins ‘Target Topics’ Podcast to Discuss State of Delegated Underwriting Authority Enterprises Market

- KBRA Assigns Rating to TruSpire Retirement Insurance Company

More Annuity NewsHealth/Employee Benefits News

- Findings from Yonsei University Advance Knowledge in Demography (Different Understandings of Scientific Research in the Use of De-identified Personal Sensitive Data: South Korea, in Comparative Perspectives): Science – Demography

- Data on Influenza Vaccines Discussed by Researchers at University of Lucerne (Keep Reminding Me To Get My Flu Shot): Immunization and Public Health – Influenza Vaccines

- Bobby Harrison: Rising insurance exchange costs bad for working poor

- New Managed Care Findings from Brown University Reported (Prior Authorization In Medicare Advantage: Beneficiary Exposure And Plan Disenrollment In 2021): Managed Care

- Findings on Managed Care Detailed by Researchers at Renal Research Institute (AI-Driven Interventions for Imminent Hospital Admissions in Patients with End-Stage Kidney Disease: A Medicare and EMR-Based Analysis): Managed Care

More Health/Employee Benefits NewsLife Insurance News

- Best’s Market Segment Report: AM Best Maintains Stable Outlook on South Korea’s Non-Life Insurance Market

- Horace Mann Strengthens Customer Relationships and Accelerates Long-Term Growth Through Transactions with Medical Mutual of Ohio

- Regulators: ‘No firm conclusions’ from first offshore reinsurance filings

- Allianz Life Study Finds Americans Struggle to Shift From Retirement Saving to Spending

- The next growth phase in life/annuities depends on modernization

More Life Insurance News