As insurtech investment slows, future remains cloudy

Insurtech startups arrived in a big way in recent years, propagated by millions of dollars in startup investment. The promise of insurtech has been to provide insurance faster and easier — and cheaper — relying on big data, more accurate risk assessment, technology such as telematics, and convenient apps. Investment in insurtech has slowed recently, though, and the industry may not be delivering on its initial promise.

Insurtech experienced an investment high in 2021 of $14.4 billion across 644 deals, according to Boston Consulting Group. Insurtech in Q2 of 2022 has been on course to be about 50% of the investment seen in the previous year. According to GlobalData, the value of global investments in insurtech fell by a staggering 79.6% in 2021.

“These trends are likely due to a combination of factors,” said Ben Carey-Evans, senior analyst at GlobalData, adding, “The investment into the sector has dried up somewhat.”

Insurtech has made inroads into the insurance industry, however, despite the declining valuations and reduced investments.

According to the recently released J.D. Power 2022 U.S. Home Insurance Study, “Overall, nearly one-fourth (23%) of home insurance customers are aware of insurtech offerings from companies like Lemonade, Hippo, Kin, Openly, Jetty and Trove. Among homeowners not currently insured by Lemonade but aware of the brand, 34% say they ‘definitely will’ or ‘probably will’ purchase from Lemonade if it is available in their state.”

“I think the future of insurtech investing will be with those that are designed for insurance distributors — agents, brokers, etc. — rather than those that are too focused on the direct-to-consumer market,” said Mike Brown, director of communications at Breeze, an insurtech that specializes in disability and critical illness insurance. Breeze received $10 million in series A funding in 2021.

“It’s become clear that the insurance market is a tough one to crack for new companies,” said Brown, adding, “There are just too many legacy companies and insurance professionals with too many strong relationships. It’s difficult to reach buyers … you need the agents and the brokers; they are the veins of the industry. The insurtechs that will win going forward are those that have designed streamlined online platforms that make it easier for agents and brokers to sell a product.”

‘Opportunity for new entrants’

“There is definitely opportunity for new entrants in the market, especially ones who excel at improving the customer journey and streamlining the entire digital experience,” said Eileen Potter, solution marketing leader for the insurance industry, ABBYY. “Chief among them is making onboarding easier so customers complete the entire process via their smartphone,” said Potter, adding, “This includes automatic document processing with mobile capture, identity proofing, and affirming of IDs and supporting documents — and using process intelligence to ensure the digital experience is smooth.”

“I also think there will be continued innovation in insurtechs that are created in incubators run by established insurers,” said Potter. “This enables them to market-test new products and innovate with new distribution channels. This will also give them the opportunity to use new technologies on a smaller scale before trying them out in other parts of their organizations. It’s definitely a faster and less risky way to road-test ways to use artifical intelligence, low-code/no-code and other emerging technologies in their operations.”

Potter cited Lemonade and Hippo as examples of insurtechs that are likely to succeed.

“They’ve both made similar moves with respect to making executive hires from within more established corners of the industry,” Potter said, adding, “Ultimately, I feel like the combination of innovative ideas from industry newcomers who feel unencumbered by ‘the way we’ve always done things’ combined with the business acumen of insurance veterans will be what separates insurtechs who are a flash in the pan from those who will succeed over time.”

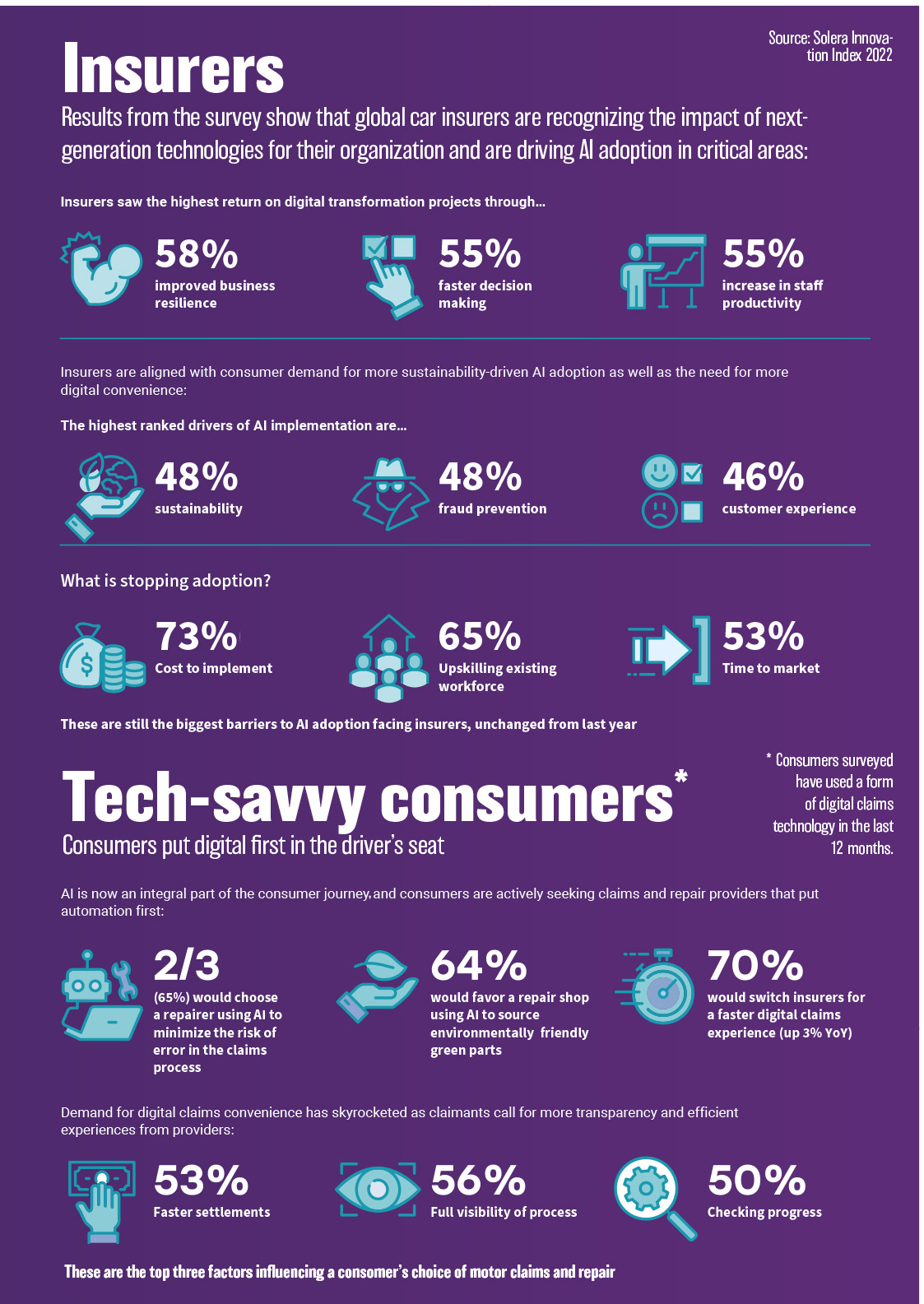

Bill Brower, vice president industry relations and vehicle claims at Solera, has a long history with traditional carriers, having worked at Liberty Mutual and Nationwide. He believes that consumers, especially after the pandemic, want to see more ease of use and convenience. “This idea of automating claims is growing in popularity with customers,” he said.

In their Innovation Index 2022 report, Solera found that 49% of tech-savvy consumers surveyed would prefer self-service when it comes to vehicle claims. “Also, 79% said they would trust automotive claims powered entirely by AI,” he said.

Consumers seek digital convenience

Since COVID-19, Brower said, consumers have become accustomed to using digital services. “They’re saying “If I’m using Amazon, if I’m using Uber, if I’m using some of these restaurant apps, they’re very easy, they’re very intuitive, and I love this. Why can’t I do more with insurance?”

He added that with carriers facing financial pressures due to inflation, workforce turnover (“the great resignation”) and supply chain issues, a move to more self-service and automation in the insurance industry is likely.

Dennis Winkler, insurance industry director with global technology research and advisory firm ISG, says that investment in insurtech has decreased for a couple of reasons.

“Leading into the pandemic, the availability of cheap capital led venture capital and private equity firms to look for new opportunities for investment returns,” Winkler explained. “In recent years, the insurance industry has been viewed as a soft target ripe for disruption. That led to a huge ramp-up in investment in insurtechs. As a result, we’re coming off a near-term high-water mark.

“The market is seeing lower valuations in the tech sector overall, and insurtech valuations are also being impacted by rising interest rates — and the fact that most insurtechs are not delivering ROI or even making money,” Winkler said. “In addition, opportunities for realizing gains on investments through initial public offerings and merger, acquisition and divestiture have diminished. An example of this lack of profitability is Lemonade, one of the higher-profile insurtechs, which lost $56 million in Q1 and $68 million in Q2.”

Winkler said insurtechs that offer complementary — rather than competitive — products to current carriers have a great opportunity to continue to fill gaps with carriers. Carriers, said Winkler, “know it is better, cheaper and faster to buy these services and software than try to build on their own. There is always risk with a tech startup, but insurtechs should see a better-than-typical share of winners versus losers.”

Winkler said insurtechs competing for insurance business need to make “bold growth and diversification moves” like Lemonade did with its July acquisition of Metromile, which brought with it licenses to sell auto insurance in 49 states. “And with Lemonade instantly adding Metromile’s data and algorithms, it gave them a competitive advantage that other auto insurance carriers will take years to build,” he said.

“We must look beyond insurtechs attempting to compete as full carriers to those that are solving specific industrywide problems or challenges, which legacy carriers don’t have the time, priority or ROI to solve themselves,” Winkler said. “The more niche and simultaneously universal the problem, the increased likelihood of success,” he said, adding, “Those insurtechs that can fill these voids, while achieving near-term profitability to enable future growth, will be the long-term winners.”

‘Financial planning is for everyone’ — With Osmar Garcia

Can ‘regtech’ help producers stay compliant with new rules?

Advisor News

- Demonstrating the value of life insurance to Gen Z

- Poor money habits are a dealbreaker in a new relationship

- DC plan sponsors see opportunity in alternatives

- The American Dream: Redefined as financial stability

- Partial annuitization: How advisors can help clients balance income, growth

More Advisor NewsAnnuity News

- CA judge certifies class action in teachers’ lawsuit over in-plan annuity fees

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Managing Director Joins ‘Target Topics’ Podcast to Discuss State of Delegated Underwriting Authority Enterprises Market

- KBRA Assigns Rating to TruSpire Retirement Insurance Company

- Partial annuitization: How advisors can help clients balance income, growth

More Annuity NewsHealth/Employee Benefits News

- CEO: Medicaid work requirements will hurt Iowa healthcare

- Copay assistance is meant to defray patient drug costs. Some insurers keep it instead

- Amid claims of 'playing politics,' Auburn council amends city manager's contract

- OCWNY to hold seminar for disability beneficiaries Friday

- Atrium pushes back after State Health Plan leaves healthcare network out of Tier 1

More Health/Employee Benefits NewsLife Insurance News

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Upgrades Credit Ratings of Sagicor Financial Company Ltd. and Most of Its Subsidiaries

- Trust, technology and the future of claims

- New York Life Launches an Indemnity Benefit for its Asset Flex Long-Term Care Insurance Solution

- AM Best Affirms Credit Ratings of DB Insurance Co., Ltd.

More Life Insurance News