Advisor input crucial to the annuity-buying decision

An investor may have many reasons for choosing whether to buy a deferred annuity when it’s offered. For example, some investors purchase annuities to generate lifetime-guaranteed income, others to accumulate assets and others to protect their principal. Non-buyers may refrain from purchasing deferred annuities offered to them because of fundamental objections to the product or feeling that their financial situation does not require a deferred annuity.

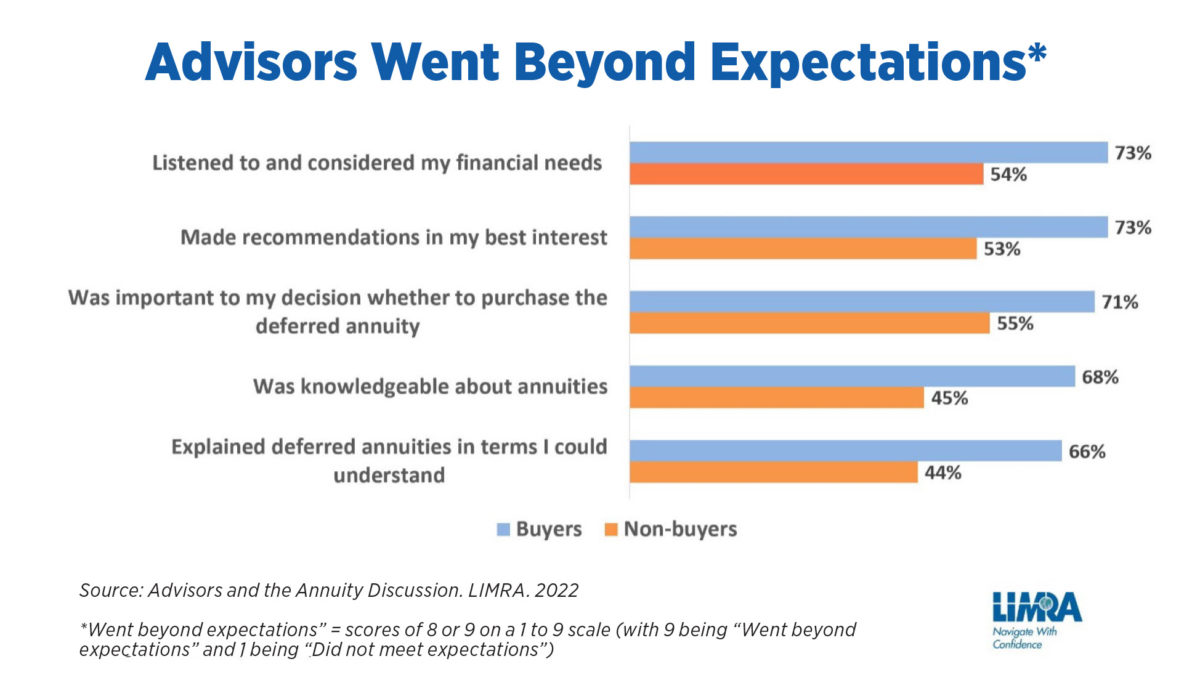

Recent LIMRA research shows clients’ financial advisors are also critically important to these purchase decisions. The specific actions taken by advisors can help or harm their probability of closing an annuity sale. Moreover, clients’ experiences working with their advisors when discussing deferred annuities have important ramifications for the advisors’ practices’ future success.

LIMRA surveyed more than 900 investors, all of whom were aged 45 to 80, had household investable assets of $100,000 or more, and had met with their advisors within the past three years and discussed deferred annuities. Participants were asked to assess their advisors’ performance during these interactions. Across a range of measures, investors who decided to buy deferred annuities rated their advisors more favorably than non-buyers did.

Advisors who listened to their clients and ensured they understood the annuity products, demonstrated strong annuity knowledge themselves, and made recommendations perceived as being in the best interests of their clients tended to have a better chance at completing a sale.

In addition, buyers were significantly more likely than non-buyers to be satisfied with their advisors, to be willing to undergo the same process again if the need arises, and to recommend their advisor to family or friends. As referrals are usually the lifeblood of future business development, it is essential that advisors strive to treat every interaction with clients as an opportunity to demonstrate their value.

Could the advisors of the non-buyers have done something differently that would have resulted in sales? Yes. Our research shows that most non-buyers (58%) feel that their advisors could have. According to non-buyers, the top improvement advisors could make is increased communication. If advisors can provide better explanations of the advantages and benefits of the deferred annuity product, the product’s fees, how the deferred annuity would fit into the portfolio, and the differences between deferred annuities and other types of annuities, a sale would be more likely.

Training on deferred annuity products and listening to clients could help more people feel comfortable with investing in these products.

Instructing advisors on the deferred annuity value proposition and its unique sales process could help increase sales. Having fine-tuned listening skills, especially during the needs analysis phase of the sales process, is critical. More education to help advisors understand how deferred annuities fit into formal retirement plans for managing income, expenses and assets in retirement would also be valuable.

Advisors should also be prepared to meet clients at their level of understanding about deferred annuities, which is likely to come from a variety of information sources beyond the advisor. They need to acknowledge that some clients will come into the meeting with their own (perhaps strongly felt) ideas about annuities based on the resources they have consulted. Being able to address a wide range of common objections will be essential for success.

Annuities cast a light when things seem dim

Help clients understand rising long-term care costs

Advisor News

- Demonstrating the value of life insurance to Gen Z

- Poor money habits are a dealbreaker in a new relationship

- DC plan sponsors see opportunity in alternatives

- The American Dream: Redefined as financial stability

- Partial annuitization: How advisors can help clients balance income, growth

More Advisor NewsAnnuity News

- CA judge certifies class action in teachers’ lawsuit over in-plan annuity fees

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Managing Director Joins ‘Target Topics’ Podcast to Discuss State of Delegated Underwriting Authority Enterprises Market

- KBRA Assigns Rating to TruSpire Retirement Insurance Company

- Partial annuitization: How advisors can help clients balance income, growth

More Annuity NewsHealth/Employee Benefits News

- Map: Where Obamacare Enrollment Is Falling

- Data on CDC and FDA Detailed by Researchers at University of New Hampshire (Long Covid Among Adults With Pre-existing Disabilities: Evidence From the 2022 National Health Interview Survey): CDC and FDA

- Digging deep: Who's funding Skagit's 2026 legislative, county races

- Atrium’s WakeMed acquisition faces new hurdle after State Health Plan decision

- New Arizona law provides clarity regarding firefighters’ health insurance

More Health/Employee Benefits NewsLife Insurance News

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Upgrades Credit Ratings of Sagicor Financial Company Ltd. and Most of Its Subsidiaries

- Trust, technology and the future of claims

- New York Life Launches an Indemnity Benefit for its Asset Flex Long-Term Care Insurance Solution

- AM Best Affirms Credit Ratings of DB Insurance Co., Ltd.

More Life Insurance News