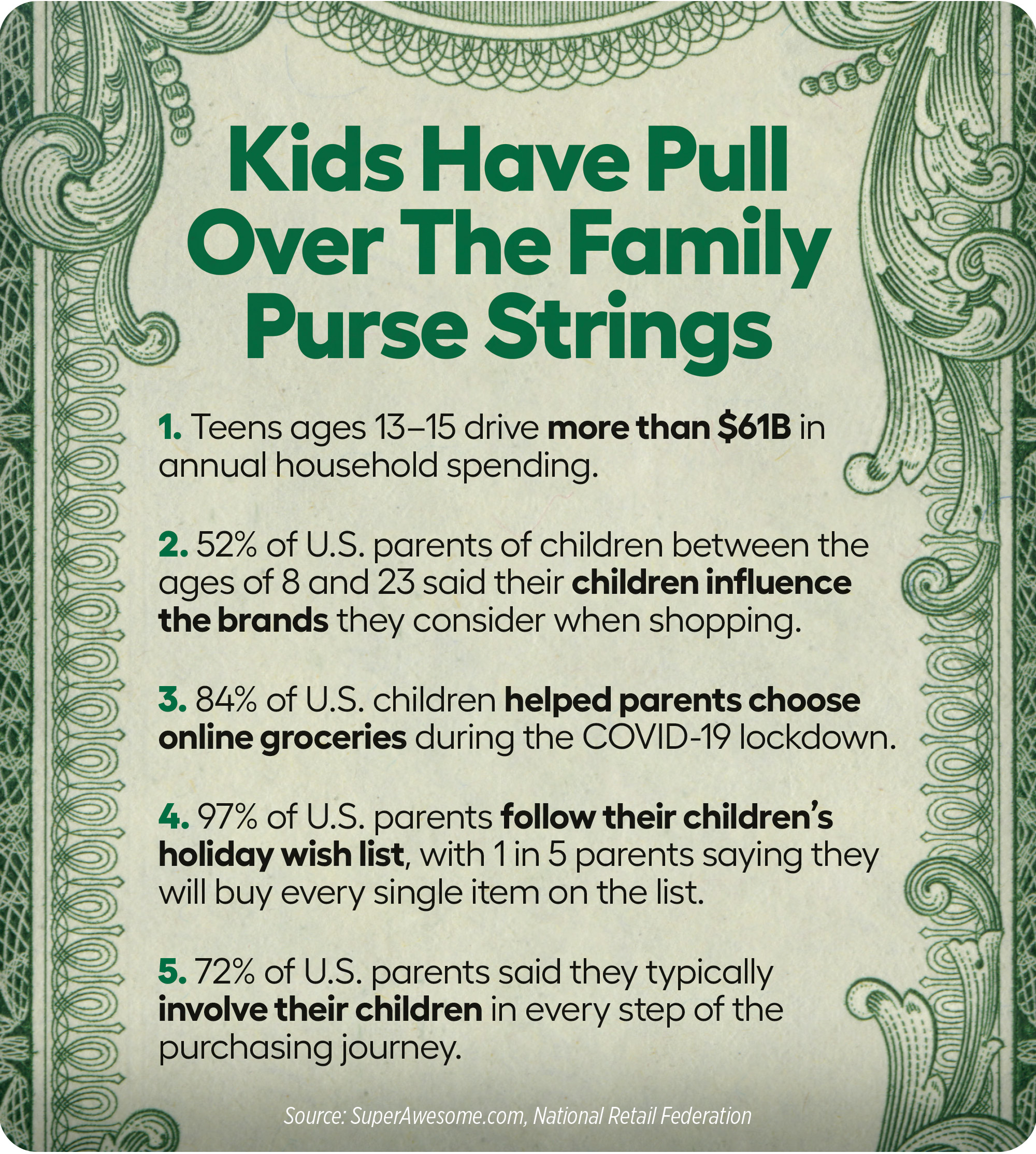

You Helped Your Clients Build A Budget — But What About Their Kids?

Part of our job as advisors is educating clients on good financial strategies, including helping them determine and maintain a budget. But who’s educating their kids?

Just as sure as budgeting is a key to financial success, it’s a topic that’s often avoided, even at the adult level. If you can find a way to help your clients sew the concept of budgeting into their kids’ brains, their children will grow up with a healthy attitude on the subject and will have a much better chance at achieving a secure financial future. Plus, by empowering your clients who are parents to have this beneficial conversation with their children, you’ll cultivate greater client trust, securing longer-term clients.

Beginning The Conversation

Tweens (ages 8-12) are at the age where the concept of budgeting starts to make sense. Introducing them to your actual household budget is a crucial first step in helping them understand what money is and what money does. It’s a natural next step to then move to establishing their own micro budgets.

Before introducing the budget conversations, your client will want to first explain the differences between income and expenses. In a child’s world, income can be described as any form of inflow from allowance or part-time jobs such as caddying, mowing the lawn or babysitting. On the other hand, expenses are outflows for goods and services such as toys, books, clothes and food.

With that foundation, your client is now ready to define budgeting and why it’s important. Parents can start with the simple explanation of: “Budgeting is the way our family decides what our financial priorities are, and it helps us spend in order of greatest importance based on our financial situation. Done right, this allocation of money gives us the ability to spend without guilt, assuming we’ve included adequate saving as part of our plan.”

From there, they’ll be able to break down how budgeting helps their family determine financial priorities (such as food or school tuition) while still allowing them to spend money on nonnecessities (such as toys or a family vacation). Sharing which items are financial priorities — such as food, clothes and shelter — compared with nonnecessities is helpful too.

Establishing The Budget

After your client has defined what a budget is, they can then take the child through the steps of building their own budget. Having the child make a personalized budget allows them to think through all the expenses that are attributable to only them and go through their own process. Here is an easy process for parents to kick the conversation off with their children:

1. Brainstorm the categories of outflows. First, advise your client to ask the child to brainstorm a list of all their personal expenses. This may include clothes, food, tutoring and sports. Let the child struggle through the list over a few days and try to add to the initial brainstormed list over the course of a week. Ask the child to assign costs to each expense. They might struggle with knowing how much things cost, so you can guide them along the way.

2. Finalize the category list. Next, your client can help the child think through the categories that might have been left out. Help them get familiar with everything that is spent on them or that they spend.

3. Tweak and formalize the revised budget. This is typically when your client should introduce the idea of needs versus wants, otherwise known as the distinction between fixed versus discretionary expenses. A fun way to introduce this idea naturally is via the needs-versus-wants game during car trips. Play the game by identifying stores, billboards, or commercial trucks that you pass that represent different companies that distribute all sorts of things: restaurant foods, plumbing supplies, accounting services, etc. For example, the parent identifies a supermarket and asks, “Is food a need or a want?” Eventually you’ll start a debate when you see a McDonald’s, which serves food, which is a need — but do you “need” to eat out at a restaurant?

The Bottom Line

When children are participating in spending and budgeting, it gives them an understanding of how much items cost, promotes ownership, and enhances gratitude for purchases made by them and members of their family. By helping your client introduce the idea of a budget to their children and having them establish their own personal budget, they can begin shaping a brighter financial future for their kids.

In addition, clients will appreciate the value you place on one of the most important parts of their life — their kids. Empowering your clients with child-friendly strategies serves to deepen their trust in you as an advisor and affirm the interest you give their lives beyond their finances.

How Will Caregiving Impact A Career Or A Business?

How Brokers Can Support Overtaxed HR Teams

Advisor News

- Dutch gambling tax hike falls short as prediction markets eye World Cup

- Caregiving: A challenge that costs employers billions

- Could your practice benefit from an advisory board?

- SEC nears settlement with accused scammer Tai Lopez

- The 3 things that shrink your Social Security income

More Advisor NewsAnnuity News

- Globe Life Inc. (NYSE: GL) Highlighted for Surprising Price Action

- Trademark Application for “EMPOWER YOUR MONEY” Filed by Empower Annuity Insurance Company of America: Empower Annuity Insurance Company of America

- Built-in guaranteed annuities: What advisors should know

- Malibu Life Holdings Completes Acquisition of TruSpire, Establishing Malibu USA and Accelerating Entry into the U.S. Retail Annuity Market

- Why job boards are failing insurance agencies

More Annuity NewsHealth/Employee Benefits News

- Findings in Type 2 Diabetes Reported from Institute of Urban and Demographic Studies (Impact of Health Insurance Coverage on Diabetes Care Quality: A Systematic Review and Meta-analysis of Racial, Ethnic, and Gender Disparities in U.S. Adults …): Nutritional and Metabolic Diseases and Conditions – Type 2 Diabetes

- Nassau University Medical Center Researchers Provide New Study Findings on Health and Medicine (Health insurance payor type and care deviations in patients with trauma with lower extremity fractures): Health and Medicine

- Public worker premiums to spike again

NJ public worker health plans poised for another year of premium hikes

- New Health and Medicine Findings Has Been Reported by Researchers at Health Insurance Review and Assessment Service (Mortality, Health Care Use, and Spending Patterns During South Korea’s Trainee Physicians’ Walkout): Health and Medicine

- Dishonest telemarketers are selling fake health insurance, leaving Minnesotans in the lurch

More Health/Employee Benefits NewsLife Insurance News

- Could your practice benefit from an advisory board?

- AM Best Revises Outlooks to Stable for Missouri Farm Bureau Group’s Members and Farm Bureau Life Insurance Company of Missouri

- Globe Life Inc. (NYSE: GL) Highlighted for Surprising Price Action

- AM Best Assigns Credit Ratings to China Ping An Insurance (Hong Kong) Company Limited

- Reliance Matrix Expands Employee Navigator Integration with New Evidence of Insurability (EOI) API Enhancement

More Life Insurance News