Why The Annuity Tide May Be Turning

If Americans want to retire and set aside worries about future income, many of them are going to need some help from the insurance industry.

Sure, those in the top tax brackets have an abundance of options and plenty of advice on how to manage their finances. However, many people can benefit from the guaranteed lifetime income that comes from annuities.

Yes, I know that “annuity” is a dirty word. In fact, the 2020 Guaranteed Lifetime Income Study by Greenwald & Associates and CANNEX found that to be true yet again. One-third (33%) of consumers who liked the idea of guaranteed lifetime income lost interest once they heard the word “annuity.” Even so, the tide may be turning for annuities.

Why the optimism? Let’s talk about the SECURE Act, which paves the way for sponsors to add guaranteed lifetime options to their plans (more on this later in this article) and, perhaps counterintuitively, may increase annuity sales outside of retirement plans.

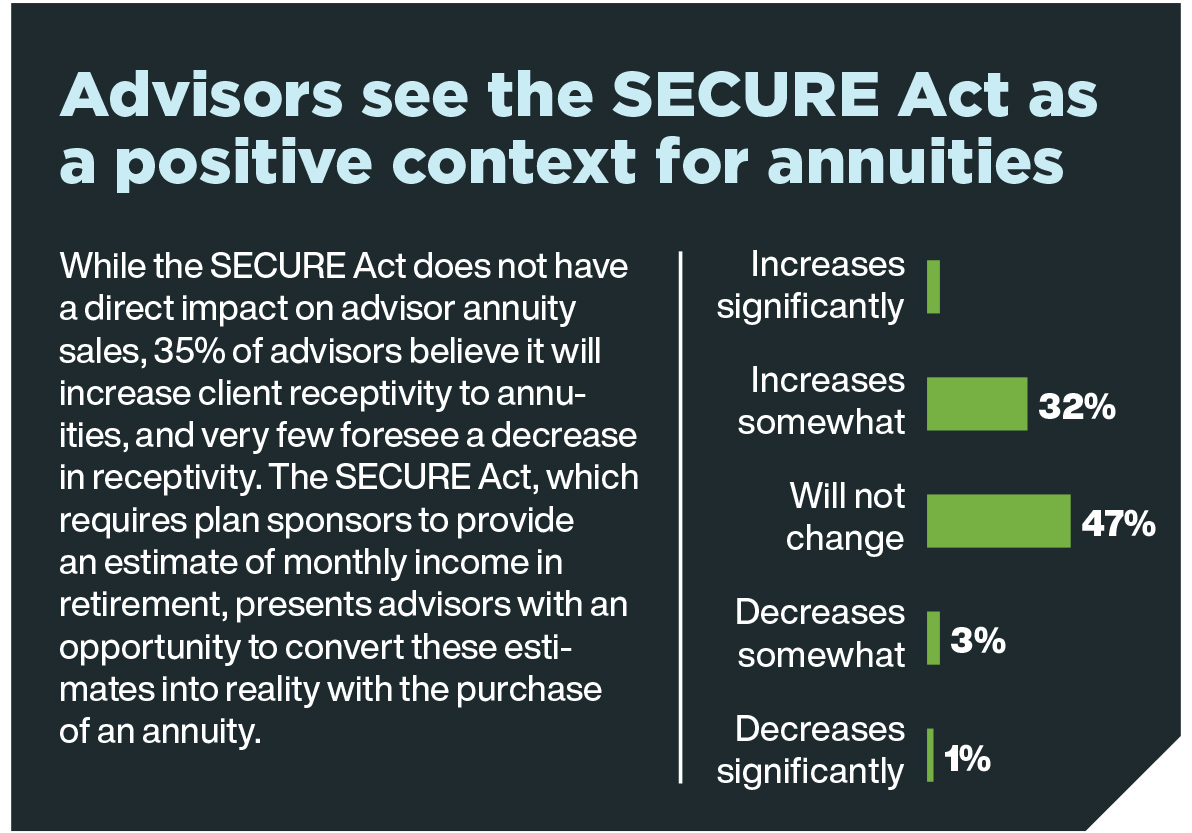

In fact, one-third (35%) of financial professionals we surveyed thought that clients will be more receptive to annuities because of SECURE. And one-quarter (27%) thought it would lead to an increase in annuity sales. Their clients are even more enthusiastic: Nearly half (46%) of consumers who hadn’t yet retired said they would be more interested in buying a product with guaranteed lifetime income if one were available within their retirement plan.

These questions, which were part of the 2020 study, shed light on the unexpected consequences of legislation that focuses on employer-sponsored retirement plans. At first blush, it may seem like there is no relationship between that and retail sales. However, SECURE does two things in particular that we believe could affect how clients perceive annuities and embrace them as part of their personal retirement plan solutions.

Establishment Of Safe Harbor

For one, SECURE establishes a safe harbor for the selection of guaranteed lifetime income contracts. This means it is much easier for plan sponsors to add these options to their plans, and we certainly hope that this will happen more often.

We don’t expect a tsunami of employers rushing to add annuities to their plans, but even if adoption is slow, there is a secondary benefit of focusing attention on them. SECURE’s emphasis on annuities in itself is an endorsement of their value in increasing retirement security.

After all, it was important enough for the Department of Labor to expand its regulations specifically to increase worker access to these products.

Plus, the safe harbor itself shows that employers (and by association, their employees) can trust companies that meet certain criteria, validating the product. We believe that SECURE’s safe harbor allays concerns about the financial security of the companies issuing annuities.

Disclosure Of A Lifetime Income Stream

Another requirement under SECURE is the disclosure of how much income from a life annuity a worker would get from the current account balance. This provision takes steps to help savers understand how accumulated savings would translate into a regular guaranteed payment. For one thing, this addresses the psychological barrier clients face when handing over a very large amount of money in exchange for much smaller checks.

But it turns out that investors want to know this too. After all, the calculation of future income from a lump sum is not intuitive, yet it is critical to paint a basic picture of what life in retirement will look like. In the study, half (52%) of pre-retirees thought that an estimate of future income would be more valuable than estimates of either expenses in retirement or how much to save.

What does this have to do with financial professionals?

First of all, clients will be seeing income estimates at least once a year on their 401(k) statements and may expect the same from their advisors. I see this as a virtuous circle that could finally help orient people to the idea of future income and give them a feel for how savings will eventually translate into a regular check.

Second, many of those who haven’t been getting an estimate may not know what they’re missing — yet. Among those who saw an income estimate, 80% thought it was very helpful. By contrast, among those who hadn’t seen an income estimate, only 52% agreed. If you don’t think your clients care about this calculation, you could be wrong in short order.

Filling In The Gaps

Guaranteed income options within defined contribution plans are still few and far between. While SECURE is intended to move the needle to increase retirement security, the reality for many workers is that they will not have access to workplace annuities in the near future. This doesn’t make it any less important an issue for retirement planning.

For financial professionals, SECURE creates a prime opportunity to ask clients whether they already have access to guaranteed lifetime income through their employer plans. Best of all, based on the rationale I’ve laid out, this study suggests there is reason to believe clients may be more receptive than ever to the concept.

Employer-Sponsored Plans Must Step Up

Now, let’s get back to one of the core purposes of SECURE, which is to increase availability of annuities within retirement plans. If clients are more receptive to the idea when talking with financial professionals, why is it so important to see these options available at the workplace?

Because many people who are very interested in lifetime guarantees may never hear about them, whether or not they get professional advice. We have seen a disconnect between what advisors and consumers themselves report their interest in guaranteed lifetime income would be. Whereas two out of five consumers (42%) are very interested in these products, only a fraction of advisors (14%) think the same.

This is especially true for those with savings between $100,000 and $250,000. As it happens, 40% of advisors have a minimum asset threshold in order to consider a client for an annuity. Among those who do, 68% require assets above $250,000.

This leaves a large chunk of workers who are interested in this type of solution underserved and shows why it is so important that employers start adding annuities as soon as possible. But in the meantime, financial professionals can and should respond to the unmet demand out there.

Today, there is a growing opportunity for financial professionals to step up to the plate with more solutions that meet retirement income planning needs.

Proper client education on how these solutions work is the cornerstone of the trust and confidence they need to commit to a plan. This has not changed, but I see that SECURE provides a nudge in the right direction with the new annuity disclosure and suggests that clients may have more appetite for income replacement, especially if they are not getting it at the workplace.

After all, the income guarantee is designed to help replace a paycheck, since most will not be satisfied living on the income from Social Security alone. SECURE promotes changes that will close that gap. Until that outcome is realized — and even after — it will pave the way for workplace savings to serve as the jumping-off point for this conversation

American Equity Making Deals To Survive Low Interest Rates

8 Ways To Turn Social Media Into A Weapon For Success

Advisor News

- Demonstrating the value of life insurance to Gen Z

- Poor money habits are a dealbreaker in a new relationship

- DC plan sponsors see opportunity in alternatives

- The American Dream: Redefined as financial stability

- Partial annuitization: How advisors can help clients balance income, growth

More Advisor NewsAnnuity News

- CA judge certifies class action in teachers’ lawsuit over in-plan annuity fees

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Managing Director Joins ‘Target Topics’ Podcast to Discuss State of Delegated Underwriting Authority Enterprises Market

- KBRA Assigns Rating to TruSpire Retirement Insurance Company

- Partial annuitization: How advisors can help clients balance income, growth

More Annuity NewsHealth/Employee Benefits News

- Amid claims of 'playing politics,' Auburn council amends city manager's contract

- OCWNY to hold seminar for disability beneficiaries Friday

- Atrium pushes back after State Health Plan leaves healthcare network out of Tier 1

- Douglas Veterans Claims Clinic Connects Rural Veterans With Critical Services

- Atrium pushes back after State Health Plan leaves healthcare network out of Tier 1

More Health/Employee Benefits NewsLife Insurance News

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Upgrades Credit Ratings of Sagicor Financial Company Ltd. and Most of Its Subsidiaries

- Trust, technology and the future of claims

- New York Life Launches an Indemnity Benefit for its Asset Flex Long-Term Care Insurance Solution

- AM Best Affirms Credit Ratings of DB Insurance Co., Ltd.

More Life Insurance News