The Care Gap: Medicare and insurance won’t cover this

Financial advisors and insurance agents who avoid senior care discussions are leaving their clients — and themselves — exposed. That was the key point that came through in my recent discussion with industry leader Tafa Jefferson, founder of Amada Senior Care.

The truth is that nearly every client will eventually need some form of care — whether short-term care to recover from a broken bone or long-term assistance due to dementia or Parkinson’s disease. For advisors, this represents both a responsibility and an opportunity: helping clients prepare for the financial, emotional and logistical realities of care.

The truth is that nearly every client will eventually need some form of care — whether short-term care to recover from a broken bone or long-term assistance due to dementia or Parkinson’s disease. For advisors, this represents both a responsibility and an opportunity: helping clients prepare for the financial, emotional and logistical realities of care.

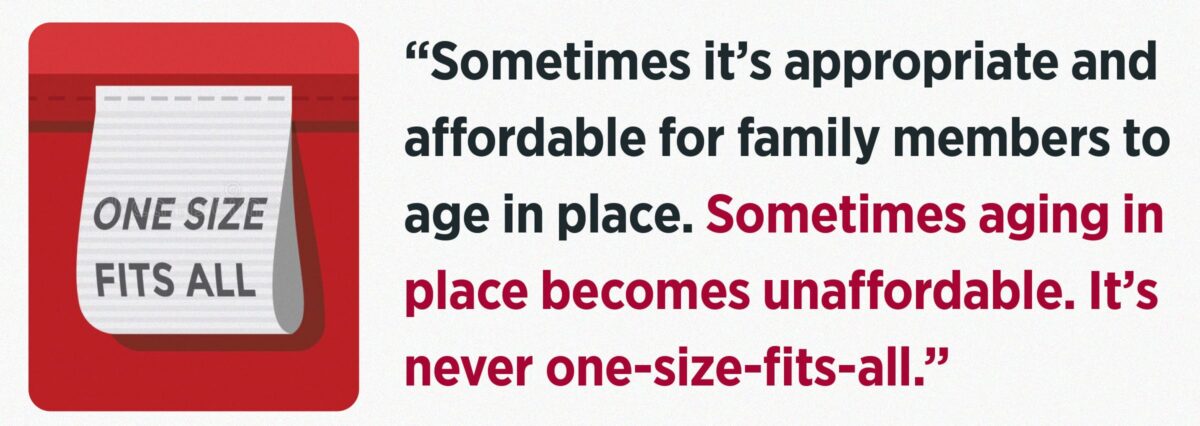

The landscape of care: Not one-size-fits-all

Senior care isn’t uniform, said Jefferson, adding, “Sometimes it’s appropriate and affordable for family members to age in place. Sometimes aging in place becomes unaffordable. It’s never one-size-fits-all.”

He said advisors should be prepared to help clients navigate multiple types of care, which include:

• Home care (nonmedical): Assis-tance with activities of daily living such as bathing, meal preparation or companionship. Not covered by Medicare.

• Home health care (medical): Skilled nursing, physical therapy or posthospital visits prescribed by a doctor. These services are often covered by Medicare, but only for limited periods.

• Assisted living/memory care: Facility-based care for those needing more structure, safety or specialized dementia support. Typically private pay, unless supplemented by long-term care insurance or other resources.

• Skilled nursing: For the highest levels of medical care, often after a hospital stay. Medicare may cover limited stays, but ongoing costs are substantial.

Insurance carriers are beginning to view home health care differently — not just as an alternative to facilities, but as a potentially more affordable and desirable option. Still, affordability depends on the intensity and duration of care.

The financial blind spot clients don’t see

What many families discover too late, said Jefferson, is that most care that people need is not covered by Medicare. “Nine out of 10 seniors discharged from hospitals need home care, and that’s long-term care insurance territory,” he explained.

Advisors who clarify this distinction early build trust and prevent unpleasant surprises. They must help families understand:

• What Medicare covers: Short-term skilled care, certain hospital and rehab stays

• What it doesn’t cover: Long-term, custodial or ongoing non-medical care

• How to bridge the gap: Insurance products, VA benefits, life settlements, home equity solutions or private savings

This kind of guidance transforms an advisor from a transactional salesperson into a trusted lifelong partner.

Why advisors should stay involved during care episodes

Once a claim is filed, said Jefferson, too many advisors step away from the process.

Often, once the claim is paid, the surviving spouse leaves the advisor; and when the remaining estate goes to the second generation, the advisor is usually out.

Jefferson pointed out that when advisors remain connected during a parent’s care episode, they often form new bonds with sons and daughters. Those relationships can lead to multigenerational clients.

Advisors can add value by:

• Checking in during care events

• Helping clients and families understand benefits

• Coordinating with care agencies to ensure claims are filed correctly

• Offering emotional support and guidance during stressful decisions

This “small role” can have big long-term payoffs. It demonstrates care for the whole family, not just the policy.

Filing and managing claims: Do it right the first time

Claims management is more complex than most advisors realize, said Jefferson. “You kind of get one shot at filing what we call a clean claim. If it’s filed incorrectly, it can create a really bad situation for the advisor and the family.”

Practical tips for advisors include:

• Partner with agencies that employ clinicians (such as registered nurses). These professionals help ensure claims are documented correctly.

• Understand that the carrier determines eligibility — not the advisor, not the agency. Setting clear expectations prevents confusion.

• Remember that claim management is ongoing. Initial filing is just the first step; maintaining the claim over several years requires diligence.

Advisors should offer to help their clients through the process: “Call me before you file any claims. I’ll do my utmost to help you get your claim through.”

Short-term needs: Not just for seniors

Senior care conversations often focus on aging, but accidents and disabilities create care needs for younger clients who need care that they can’t provide for themselves and who don’t have a partner or family member to provide that care.

Short-term, nonmedical care is a critical but often overlooked part of planning, said Jefferson. Whether it’s a hip fracture, surgery recovery or temporary disability, clients value the ability to stay at home while receiving support.

Advisors who raise this point broaden their relevance beyond senior care — positioning themselves as advocates for all stages of life.

An opportunity to build generational trust

“There’s communication, then rapport, then trust,” said Jefferson, adding, “Trust is formed during an episode of care.”

Every advisor already has clients who will face care events. By being proactive — starting conversations, clarifying coverage and offering to help navigate claims — advisors “drill a mile deep” into existing households instead of chasing cold leads.

That depth of service not only strengthens retention but also introduces the advisor to adult children and grandchildren. In Jefferson’s words, “We need to start thinking in terms of generations to come.”

Action steps for advisors

Here are steps advisors can take immediately:

1. Educate yourself on care types. Be ready to explain the differences between home health, home care, assisted living and skilled nursing.

2. Clarify Medicare myths. Help clients understand what is and isn’t covered. Nine out of 10 discharged seniors need nonmedical care that Medicare won’t pay for.

3. Introduce funding options. Discuss long-term care insurance, hybrid life/annuity products, VA benefits, life settlements or home equity strategies.

4. Stay engaged during care episodes. Don’t disappear after the claim is filed. Offer guidance, support and coordination.

5. Partner with the right agencies. Look for those with clinical staff and experience in claims management.

6. Build relationships with the next generation. Use care events as a natural way to connect with adult children and extend your client base.

7. Position yourself as the first call. Tell clients: “If a care need arises, call me before filing any claim.”

A duty and an opportunity

The need for senior care planning is universal. Nobody intends for these events to happen, but they happen to just about everybody.

For insurance agents and financial advisors, embracing these conversations isn’t just about protecting clients — it’s about strengthening relationships, differentiating services and securing multigenerational trust.

Senior care is no longer an optional topic. It is central to the promise advisors make: to safeguard not just wealth, but well-being.

2026 midterms: What’s in play and why it matters

The insurance industry is at ground zero in a perfect storm

Advisor News

- How advisors can prepare clients for an uncertain retirement landscape

- Investors aren’t waiting out uncertainty

- Transamerica and Advo(k)ate Advisors launch pooled employer plan

- ‘I wish I’d met him sooner:’ Karlan Tucker remembered for integrity, faith

- Why women must be more engaged in investing

More Advisor NewsAnnuity News

- AM Best Revises Outlooks to Negative for Subsidiaries of Group 1001 Insurance Holdings, LLC

- Market-value adjusted annuities: Key considerations for advisors

- Private equity’s next play in insurance

- Immediate Care Plan: A new solution for funding LTC

- Delaware Life Launches a New Bonus Fixed Index Annuity Built for Growth, Protection, and Flexibility

More Annuity NewsHealth/Employee Benefits News

- Studies from Harvard University T.H. Chan School of Public Health Describe New Findings in Managed Care [Preconception, prenatal and postnatal exposure to gaseous air pollutants (NO2, O3) and neurodevelopmental disorders in children among …]: Managed Care

- Studies from Harvard T.H. Chan School of Public Health Further Understanding of Managed Care (Structural Racism-related State Laws and Healthcare Access Among Black, Latine, and White Us Adults): Managed Care

- Data on Managed Care Reported by Researchers at University of California Berkeley (Welfare Program Participation Among Us Farmworkers Evidence From Three National Surveys): Managed Care

- ON MEDICAID'S 61ST ANNIVERSARY, A REMINDER PENNSYLVANIA REPUBLICANS CONTINUE TO PUSH DEVASTATING HEALTHCARE CUTS

- ON 61ST ANNIVERSARY OF MEDICAID, 10,000 FEWER ALASKANS HAVE COVERAGE AFTER PASSAGE OF DAN SULLIVAN'S AGENDA

More Health/Employee Benefits NewsLife Insurance News

- AM Best Revises Outlooks to Negative for Subsidiaries of Group 1001 Insurance Holdings, LLC

- Court sides with Ameritas in denying $4M STOLI payout to Wells Fargo

- AM Best Removes From Under Review With Positive Implications and Upgrades Credit Ratings of The Fortegra Group, Inc.’s Insurance Subsidiaries

- Yancey Jr., Delos Harley

- Vincent Esparza CFP, CLU joins Wilde Wealth Management Group as Senior Wealth Advisor

More Life Insurance News