Selecting The Right Annuity Requires Dialogue & Partnership

With millions of Americans entering retirement over the next decade, many will benefit from the unique features of annuities. Although the core and defining value of annuities is guaranteed lifetime income, deferred annuity products offer various combinations of downside protection and upside potential. Investors of varying levels of risk tolerance will have an abundance of options to meet their financial needs.

In the current investment environment — where interest rates are low and stock market returns have generally been strong — annuity carriers and distributors need to understand which annuity product concepts have the greatest appeal and which investors favor certain products. Aligning specific annuity products with clients’ needs is a service usually performed by advisors. Because of this tendency, simply looking at sales patterns may not reveal investors’ preferences on a conceptual level. If investors are given the opportunity to select for themselves, what would they want?

A recent Secure Retirement Institute study examined investor preferences for the four main types of deferred annuities now on the market: fixed-rate, fixed indexed, registered index-linked and variable. We asked investors to consider their current financial situation and to select one of four investment options with varying degrees of downside protection and upside potential in which to “invest” $100,000 for five years. Rather than use the industry terms for the product types, we provided study participants with a basic description and hypothetical outcomes.

Nearly half of investors (46%) selected the “full downside protection, limited upside potential” option, which corresponded to an FIA. The top reason was their placing more value on protecting savings than seeking maximum gains. FIAs are especially popular among older, more conservative and less financially knowledgeable investors. Another 35% of investors chose the “limited downside protection, limited upside potential” option, which corresponds to a RILA. Those who selected RILAs tend to believe the stock market will perform well over the next five years and value the ability to maximize gains. These two product classes were much more popular than were either VA or FRD products.

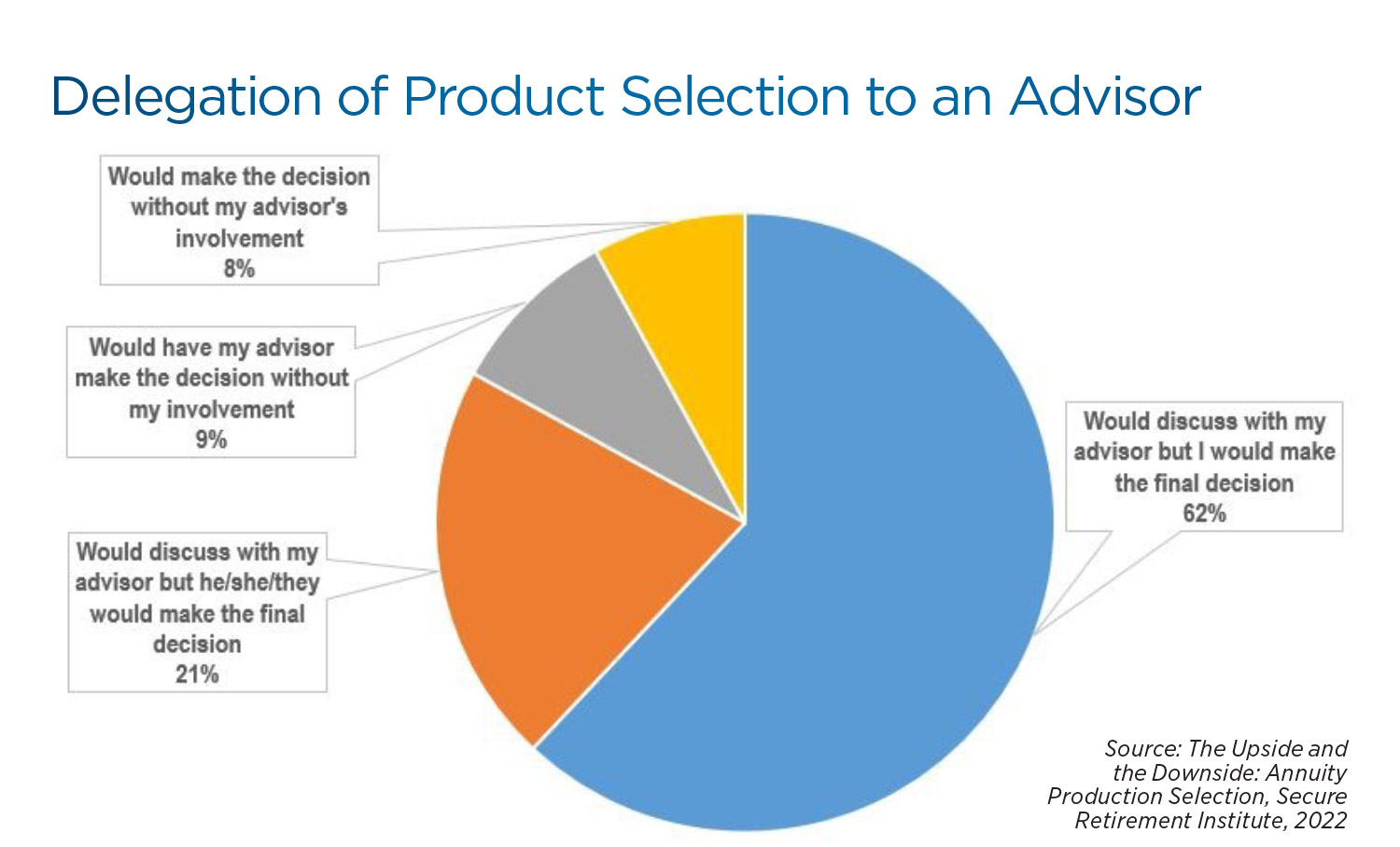

If investors have such strong preferences for FIAs and RILAs, could they simply seek out and purchase these products on their own? The SRI research suggests otherwise: Among the 57% of investors who regularly work with paid professionals to assist with the household’s financial and investment decisions, the vast majority (92%) would involve their advisors in this kind of product selection decision. Only 9% of those surveyed would fully delegate the decision to their advisors without the investor’s involvement. Older, retired and higher-income investors were more comfortable delegating this product selection decision to their advisors.

This overall selection pattern reveals that most investors appreciate the combination of upside potential and downside protection offered by FIAs and RILAs. In the context of a multiyear bull market, the notion of protecting assets clearly has traction. However, with interest rates so low, many investors also want to avoid locking in a low rate of return.

Our study clearly shows that most investors do not want the sole responsibility for such a complex financial decision. Even if clients give their advisors discretion over day-to-day buying and selling decisions in their portfolios, selection of a deferred annuity clearly requires dialogue and a partnership. When working with carriers, advisors will be successful by connecting the specific objectives of annuity products with the needs and mindsets of investors.

More States Eyeing Financial Literacy As A Graduation Requirement

Adults List The Financial Mistakes They Don’t Want Their Kids To Make

Advisor News

- What advisors should know about hedge funds in retirement planning

- Retirement control is top success measure for middle class, ACLI says

- Industry groups applaud House passage of Financial Exploitation Prevention Act

- Younger workers more likely to be eligible for a retirement plan after changing jobs

- Bank of America community event unpacks sales tax hike, small business struggles

More Advisor NewsAnnuity News

- Jackson Named InvestmentNews 2026 Annuities Provider of the Year

- State Farm’s agency overhaul: What distribution can learn

- IRI, ACLI express support for CLEAR Forms Act

- A new era at the Federal Reserve

- Globe Life Inc. (NYSE: GL) Making Surprising Moves in Tuesday Session

More Annuity NewsHealth/Employee Benefits News

- Pa., N.J. and Del. join multistate lawsuit against Trump administration over Medicaid work requirements

- Study Results from UNC Gillings School of Global Public Health Broaden Understanding of Managed Care (Days at Home among Children by Medical Complexity, Public/Private Insurance, and Urban/Rural Residence): Managed Care

- Reports from New York University (NYU) Add New Data to Findings in Managed Care (HealthySteps Comprehensive Services and Preventive Care: A Medicaid Claims Analysis): Managed Care

- 15 Maryland laws taking effect July 1 that you should know

- States take Trump administration to court over Medicaid rule

More Health/Employee Benefits NewsLife Insurance News

- Never stop learning: A lesson for the next generation of advisors

- Jackson Named InvestmentNews 2026 Annuities Provider of the Year

- Corebridge adds index strategies, growth potential to Max Accumulator+ III

- Estate planning 2.0: How ILITs can create liquidity

- AM Best Affirms Credit Ratings of Misr Insurance Company

More Life Insurance News