RILAs take off as consumers look for balance, protection

As more Americans retire without the backstop of a pension, the individual annuity market is stepping up to provide the ability to layer on protection and security to an investor’s portfolio.

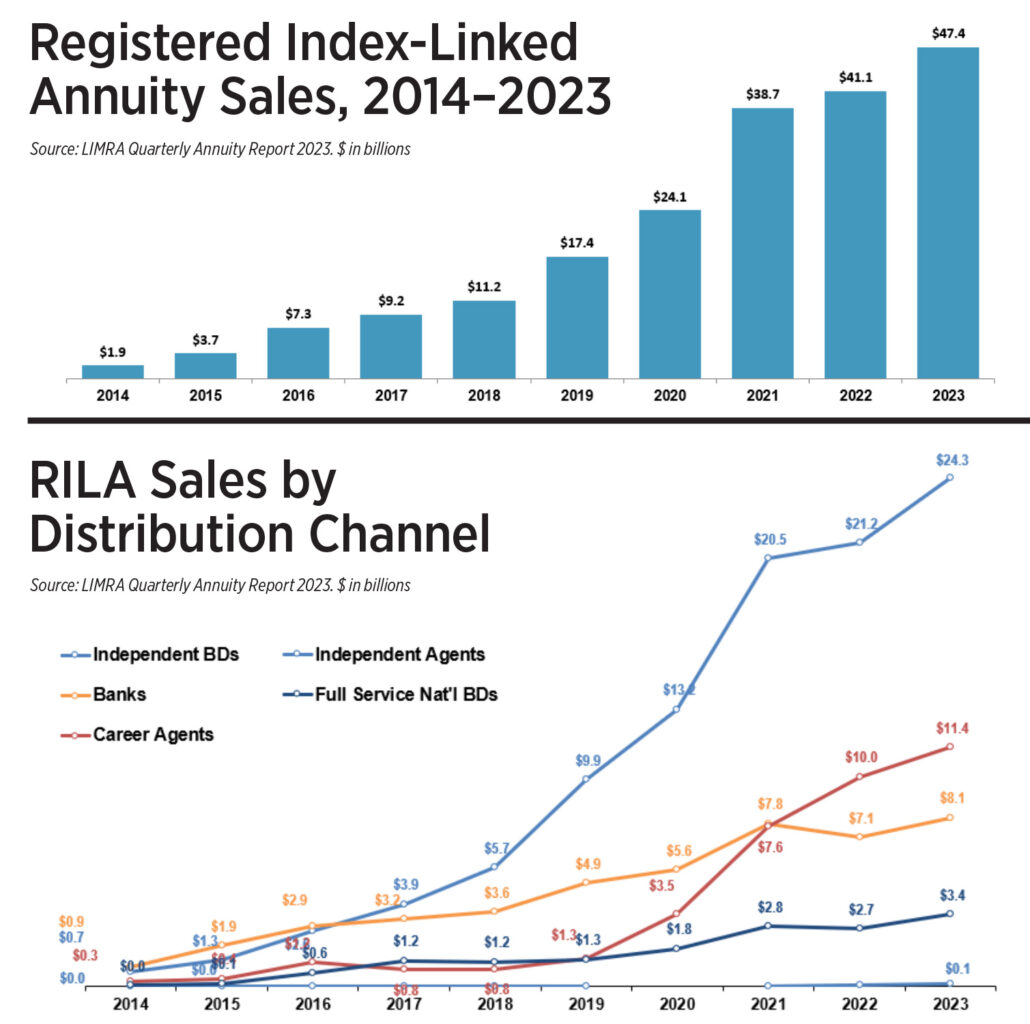

Registered index-linked annuities were first introduced in 2010 following the financial crisis of 2008-2009. However, RILA sales didn’t really take off until more than a decade later. Around the time of the pandemic, fears about an equity downturn motivated investors to take advantage of the product’s unique function of downside protection while simultaneously taking advantage of upside potential.

As a result of the value proposition offered by RILAs, these products have experienced growth for the ninth consecutive year, with sales reaching $47 billion in 2023. The growth in 2023 represents a 15% increase over 2022 and an increase of more than 2,000% from 2014 volumes, with new premium representing roughly 98% of sales and, as of 2022, an average premium of around $160,000.

Product innovation and new market entrants suggest the RILA market still has significant growth potential. For 2024 and 2025, LIMRA is forecasting RILA products to expand on the five consecutive years of record sales. RILA sales are likely to be as high as $52 billion in 2024 and $57 billion in 2025.

When looking at sales by the various channels they are provided in, RILAs continue to be sold typically through the independent broker-dealer, with IBDs accounting for more than 50% of sales in 2023, followed by the career channel, representing roughly 25% of sales.

Currently, most sales (a ratio of roughly 9-to-1) are coming from products without a guaranteed living benefit. However, as more and more carriers enter this space and emphasize sales of products with a guaranteed living benefit, we expect this segment to grow.

When looking at the split between sales of traditional variable annuities and sales of RILAs, an interesting pattern emerges. In the past, traditional VAs accounted for the majority of sales. However, as of fourth-quarter 2023 we have seen a shift where RILAs are now the dominant registered product. This trend continued through the first quarter of 2024, with no changes expected throughout the year. We might even see 2024 as the first year when RILAs outperform traditional VAs at an annualized level.

Moving forward, the RILA market is expected to continue growing, posting record sales year after year. Currently, there are roughly 20 carriers in this space, with the top five companies representing more than 70% of sales (as of first-quarter 2024). With additional carriers entering the market and providing innovation and unique features that appeal to investors, the market will grow for years to come.

Protecting clients amid the ‘triple threat’ in LTC services

Should you recommend a CLAT or a reversionary CLAT in wealth planning?

Advisor News

- The American Dream: Redefined as financial stability

- Partial annuitization: How advisors can help clients balance income, growth

- Guide women along the walk through widowhood

- Dutch gambling tax hike falls short as prediction markets eye World Cup

- Caregiving: A challenge that costs employers billions

More Advisor NewsAnnuity News

- Partial annuitization: How advisors can help clients balance income, growth

- Guide women along the walk through widowhood

- Regulators clear way to rewrite annuity illustration rules

- Diversification’s growing importance in retirement planning

- AI’s dual reality: Efficiency for insurers, disruption for agents

More Annuity NewsHealth/Employee Benefits News

- Elevance hikes 2026 outlook off strong Q2, to exit more Medicaid markets

- CVS Health Risk Factors: Key Regulatory, PBM, Insurance, and Pharmacy Risks

- New York Life Launches an Indemnity Benefit for its Asset Flex Long-Term Care Insurance Solution

- They harvest the nation’s food, but a new rule may strip them of health insurance

- CALPERS HOLDS HEALTH PREMIUM INCREASE TO 4.97% FOR 2027 WHILE ADVANCING CARE QUALITY

More Health/Employee Benefits NewsLife Insurance News

- New York Life Launches an Indemnity Benefit for its Asset Flex Long-Term Care Insurance Solution

- AM Best Affirms Credit Ratings of DB Insurance Co., Ltd.

- AM Best Upgrades Credit Ratings of The People’s Insurance Company of China (Hong Kong), Limited

- SWBC’s Joan Cleveland Reappointed to Texas Association of Life & Health Insurers (TALHI) Board of Directors

- AM Best Introduces US Life Version of Best’s Capital Adequacy Ratio Model Product

More Life Insurance News