Life insurance does more than just replace income

When mentioning life insurance to the average investor, the response is usually the same: “I pay a premium and in return, when I die, beneficiaries receive a large sum of money to help replace income that is lost.”

Although this is accurate when referring to term life insurance, universal and whole life policies offer investors additional advanced strategies, including cash value, taxation benefits, and the ability to use the death benefit if needed for long-term care. All these features make the life insurance conversation much more interesting.

Overfunding leads to cash value

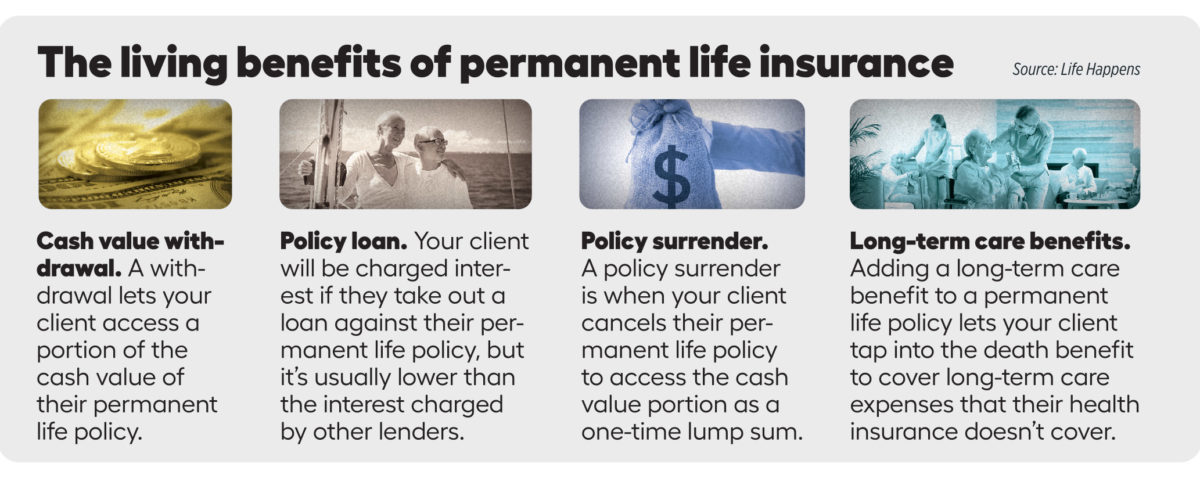

These advanced strategies can’t be done using term insurance but are available on policies that have cash value. A cash value life insurance strategy can be achieved with universal or whole life policies. In general, these types of policies are “overfunded,” meaning the policyowner is depositing money into the policy in excess of what is needed to provide the death benefit. Then this money is invested and grows tax deferred.

In universal policies, the money can be invested in the market using various indices or funds, depending on the type of policy. Meanwhile, a whole life policy usually provides a guaranteed fixed rate of return not tied to the market. These two types of insurance have pros and cons, and it’s widely debated which is the best type to own. As you can imagine, the answer depends on the purpose of the policy and the age of the person seeking it.

If your client is sensitive to market fluctuations, you might advise them toward an indexed universal life or whole life policy. Whole life offers a fixed rate of return while IUL can provide guarantees of principal protection and locked-in gains. This often will come at the cost of not receiving all the upsides of the market.

Policies can offer tax benefits

Tax benefits are a major draw for many individuals. As previously mentioned, the cash value (or the amount the policyowner overfunded) grows tax deferred. Those funds can be withdrawn from the policy in a tax-favored manner. Your client can withdraw funds and choose whether they want to withdraw the gains or some of their original deposit. This is the flexibility policyowners typically find appealing.

The gains, in this case, would most likely be a taxable event, but the gains could be part of a strategy when your client’s income is lower during their first years of retirement. This flexibility is something you can’t find in traditional retirement accounts, such as individual retirement accounts, where the order of withdrawals is not in your client’s control and the requirement to withdraw certain amounts at age 72 can cause a tax nightmare, including the Social Security torpedo tax and potentially higher Medicare part B and D costs.

A popular chosen strategy is not to withdraw money but instead allow the insurance company to lend it. The amount lent is not required to be paid back until death, when the death benefit proceeds are reimbursed by the life insurance company. This is a strategy the wealthy have been using for decades, and because it’s a loan, it’s completely tax-free.

Funds can be withdrawn in a lump sum or as a stream of income. The latter is what many gravitate toward as this stream of income is tax-free, helping to keep Social Security taxation and Medicare premiums low.

The loan will have interest, however. The interest rate often is fixed and determined at the beginning and guaranteed for the life of the contract. If the funds invested are performing better than the loan amount accruing, there shouldn’t be any issues. However, this is when you’ll want to work with your client to help create the best plan for their needs. Because of the many moving parts with this strategy, it is best to have the plan of action before the policy is sold and then tailor the policy to the plan. Even though these types of policies are flexible, it’s best to not veer too far from the illustration in order for the policy to perform at its best.

Death benefit withdrawals can help cover LTC

Strategies to withdraw money tax-free aren’t only for the cash value but can also be done with the death benefit. As mentioned previously, the death benefit often can be “accelerated” during the policyowner’s life.

This accelerated death benefit is a lump sum that can be used tax-free if needed for a long-term care event. Usually, the life insurance company will require documentation that the policyowner is unable to perform two or three of the six activities of daily living, or ADLs. ADLs are activities related to personal care. They include bathing or showering, dressing, getting in and out of bed or a chair, walking, using the toilet and eating.

Some clients assume Medicare will pay for a long-term stay in a hospital or nursing home. In most cases, Medicare will pay for only 100 days of this type of care. Anything that extends past this point will need to be paid out of pocket.

With costs ranging from $5,000 to $10,000 a month for this type of care, a retirement nest egg can take a huge hit. If such an event takes place at the beginning of retirement, a spouse can quickly drain investments meant to maintain income for the rest of their life. A long-term care policy can be purchased and designed for this sole purpose. However, premiums typically will increase as the policyowner ages. Designing a life insurance policy with the acceleration of a death benefit for long-term care is usually much less costly than a long-term care policy. Making the decision to go this route is frequently a no-brainer. Of course, if the policyowner never experiences a long-term care event, the death benefit gets paid to the policy’s beneficiaries, providing a tax-free legacy that’s hard to beat.

Life insurance has become even more useful with recent legislation, such as the SECURE Act, which eliminated the stretch IRA and added the requirement of certain beneficiaries to withdraw retirement accounts over a 10-year window after the IRA’s owners and spouses die. These changes require much larger withdrawals for most beneficiaries. These withdrawals often must be made at a time when the beneficiaries are in their peak earning years. If you believe income tax rates will increase, doesn’t it make sense to pass tax-free money instead of taxable retirement accounts to heirs?

Between tax reduction strategies, policy flexibility, and the ability to use the death benefit while you’re alive, life insurance does more than replace income and should be considered by those of any age.

Finding success with centers-of-influence marketing

Play to the end: Finish Q4 committed to 2023

Advisor News

- Poor money habits are a dealbreaker in a new relationship

- DC plan sponsors see opportunity in alternatives

- The American Dream: Redefined as financial stability

- Partial annuitization: How advisors can help clients balance income, growth

- Guide women along the walk through widowhood

More Advisor NewsAnnuity News

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Managing Director Joins ‘Target Topics’ Podcast to Discuss State of Delegated Underwriting Authority Enterprises Market

- KBRA Assigns Rating to TruSpire Retirement Insurance Company

- Partial annuitization: How advisors can help clients balance income, growth

- Guide women along the walk through widowhood

More Annuity NewsHealth/Employee Benefits News

- Findings on Science Detailed by Researchers at Health Analysis Division (The role of nonfinancial factors in the Congressional Budget Office’s health insurance coverage projections): Science

- New Managed Care Findings from University of Illinois Described (Dental Care Access for Young Children With Medicaid: Groundtruthing Online Data and Actual Access in the Chicago Metro Area): Managed Care

- Study Results from Kansai Medical University Update Understanding of Cerebrovascular Disease (Cardiovascular Safety of Romosozumab Versus Other Anti-Osteoporosis Medications in Patients with Osteoporosis: A Nationwide Health Insurance Claims …): Central Nervous System Diseases and Conditions – Cerebrovascular Disease

- This Miami health system could go out-of-network with United. What it means for you

- Health benefit premiums for NJ school workers expected to rise by 34%

More Health/Employee Benefits NewsLife Insurance News

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Upgrades Credit Ratings of Sagicor Financial Company Ltd. and Most of Its Subsidiaries

- Trust, technology and the future of claims

- New York Life Launches an Indemnity Benefit for its Asset Flex Long-Term Care Insurance Solution

- AM Best Affirms Credit Ratings of DB Insurance Co., Ltd.

More Life Insurance News