Leveraging Medicaid-compliant annuities in crisis LTC planning

Clients frequently find themselves in a long-term care crisis and need an advisor’s help. Thomas Krause, vice president of sales and marketing with The Krause Agency, described how to help a client’s crisis LTC planning during a recent event, “Don’t Be Scared of Long-Term Care” by the National Association of Insurance and Financial Advisors’ Limited and Extended Care Planning Center.

Crisis planning, he said, is the financial planning surrounding a long-term care event when someone already has entered a facility. The goals of crisis planning include avoiding or mitigating the financial stress associated with long-term care, as well as preserving assets for a healthy spouse or for the next generation.

Getting the care recipient to qualify for Medicaid is the foundation of crisis planning, Krause said, but specific criteria must be met. In addition, to accelerate Medicaid eligibility, the care recipient’s assets must be “spent down” properly. This may include purchasing or improving exempt assets, paying off existing liabilities or purchasing a Medicaid-compliant annuity.

Krause explained a Medicaid-compliant annuity is a single-premium immediate annuity that meets Medicaid requirements. It converts assets into an income stream for the owner, allowing the institutionalized person to qualify for Medicaid benefits. A Medicaid-compliant annuity has no cash value to the owner, can have terms as short as two months and can be funded with nonqualified or tax-qualified funds.

A Medicaid-compliant annuity has several requirements, Krause said. They are:

- The terms of the contract cannot be changed.

- Non-assignable. The contract cannot be assigned or sold to another party.

- Equal payments. The contract must not have any deferral or balloon payments.

- Actuarially sound. It must be a fixed term equal to or shorter than the owner’s Medicaid life expectancy, determined by the Social Security Administration actuarial life table in most states.

- State as beneficiary. The state Medicaid agency must be the primary beneficiary in most cases.

A client might be a good candidate for a Medicaid compliant annuity, Krause said, if they:

- Are about to enter a facility or are already in one.

- Have assets in excess of the resource allowance.

- Have exhausted their long-term care insurance or Medicare benefits.

- Are expected to stay at the facility indefinitely.

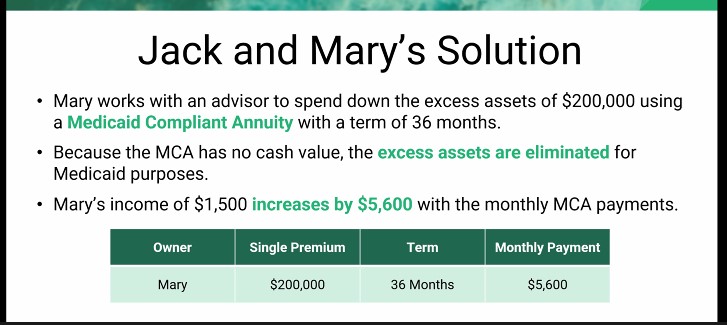

A Medicaid-compliant annuity can help in the case of a married couple in which one partner is about to enter a care facility or is already in one. Krause explained that the most common Medicare-compliant annuity planning strategy for a married couple consists of converting the spend-down amount into a Medicare-compliant annuity for the spouse at home.

The primary goals of this strategy are to:

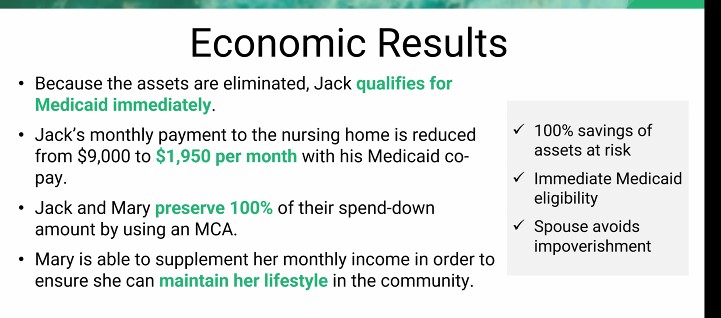

- Gain immediate Medicaid eligibility for the institutionalized spouse.

- Provide reliability monthly income to the spouse at home, avoiding spousal impoverishment.

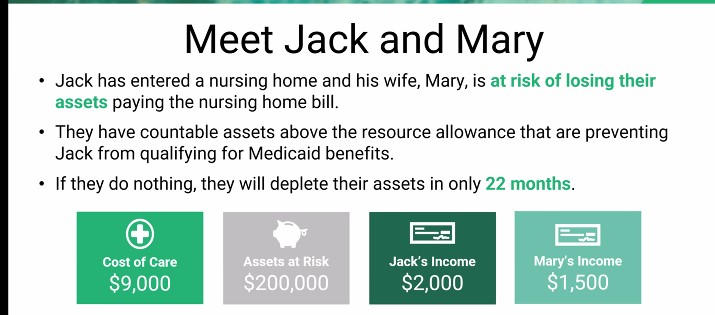

Krause provided the following case study illustrating how a Medicaid-compliant annuity can help a married couple avoid running out of assets when one partner needs care.

“There is still a solution available even if someone didn’t do their planning previously,” Krause said.

Susan Rupe is managing editor for InsuranceNewsNet. She formerly served as communications director for an insurance agents' association and was an award-winning newspaper reporter and editor. Contact her at [email protected]. Follow her on Twitter @INNsusan.

© Entire contents copyright 2023 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

MassMutual to ‘wind down’ Haven Life amid poor results, high costs

Level funding: an onramp to health plan innovation for fully insured employers

Advisor News

- Demonstrating the value of life insurance to Gen Z

- Poor money habits are a dealbreaker in a new relationship

- DC plan sponsors see opportunity in alternatives

- The American Dream: Redefined as financial stability

- Partial annuitization: How advisors can help clients balance income, growth

More Advisor NewsAnnuity News

- CA judge certifies class action in teachers’ lawsuit over in-plan annuity fees

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Managing Director Joins ‘Target Topics’ Podcast to Discuss State of Delegated Underwriting Authority Enterprises Market

- KBRA Assigns Rating to TruSpire Retirement Insurance Company

- Partial annuitization: How advisors can help clients balance income, growth

More Annuity NewsLife Insurance News

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Upgrades Credit Ratings of Sagicor Financial Company Ltd. and Most of Its Subsidiaries

- Trust, technology and the future of claims

- New York Life Launches an Indemnity Benefit for its Asset Flex Long-Term Care Insurance Solution

- AM Best Affirms Credit Ratings of DB Insurance Co., Ltd.

More Life Insurance NewsProperty and Casualty News

- What's Working: Where to find Colorado homeowners insurance discounts and grants

- COLUMN: Military members, families: Check out these insurance tips

- Homeowners of color pay higher insurance costs in WA, nationwide

- Loews Corp. (NYSE: L) Highlighted for Surprising Price Action

- Charleston ranks 10th-riskiest US county to insure. Here’s how much it costs

More Property and Casualty News