Expand your toolbox with cash value life insurance

While the market may only do three things in a given day (go up, go down, remain flat), recently it seems that the ups and downs are more extreme and occurring more frequently.

Because this is today’s investment reality, no longer should we use traditional asset classes and allocation strategies alone to reduce risk. Nor should we continue to rely solely on traditional investment products and planning strategies created during different times when constructing investment portfolios and developing planning strategies today. We must be more creative and evolve with the times.

To paraphrase David McKnight, people really do not want to save or invest more money; they want to be smarter about the money they are saving and investing. So, as we evolve, how can we be more creative when implementing savings and investment strategies that will work over time and are more efficient with planning dollars?

The answer is simple: Expand your toolbox. How, you ask? Simply consider a tool that has been available for centuries that is now being used as a “new” alternative investment in today’s new world. This tool’s general features include:

» Most favored asset class status in the IRS Tax Code.

» Tax-deferred growth and tax-free income distributions for any reason.

» Liquidity without penalty before and after age 59 ½.

» No traditional qualified plan funding limitations.

» No required minimum distributions.

» Distributions are not included in IRS provisional income calculation to determine whether Social Security income is taxable.

» Cash value and distributions are not considered in college financial aid calculations.

» Professional and institutional investment management.

» Leveraged asset transfer efficiency, unlike other assets.

» Can be a “no work and no worry” proposition with guarantees.

So, what is this “new” investment alternative that has been around for so long? Ready? Answer: cash value life insurance. Yeah, I know: letdown, right? Hold on! Keep reading.

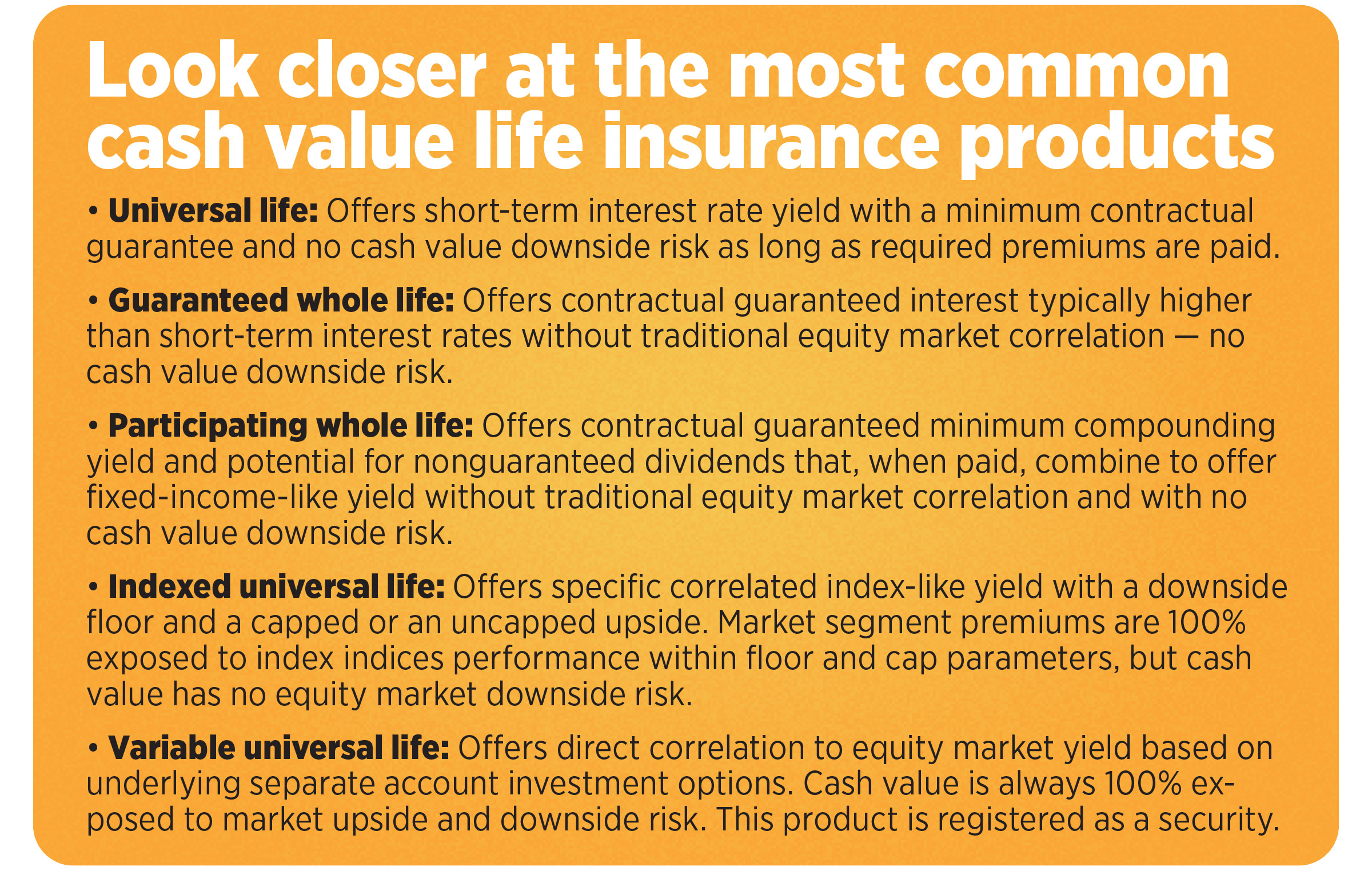

You see, as the investment world has grown and evolved over time, so has the life insurance industry. Today’s cash value life insurance products offer all features mentioned above and more. Furthermore, every one of these features is a benefit that any and every saver or investor wants.

Additionally, life insurance eliminates potential investment liquidity at death, preserving investment portfolios. Cash value life insurance also can be used as an asset in a diversified investment strategy or as a hedge in an investment plan. Today’s cash value life insurance can be designed to offer guaranteed interest, fixed-income-like returns with guarantees, market index indices return with guarantees and complete equity market upside potential like other traditional investments.

Furthermore, in addition to providing attractive competitive returns, tax-free growth, tax-free income, and access to cash for purchases, expenses, emergencies, opportunities, and things like college funding and retirement, cash value life insurance may also be designed to provide living benefits for things such as terminal and chronic illness.

Today’s life insurance products can allow for death benefit acceleration under certain circumstances while the policy owner is living. General life situations where death benefit acceleration may be helpful include the following.

Critical illness: A sudden acute medical condition or event. Examples of qualifying conditions include major heart attack, coronary artery bypass, stroke, invasive and blood cancers, major organ transplant, end-stage renal failure, paralysis, coma, and severe burns. Conditions vary by carrier and state.

Chronic/cognitive illness: Doctor-verified inability to perform two out of six activities of daily living, requiring assistance or supervision for severe cognitive impairment. Those activities of daily living include walking, bathing, dressing, eating, toileting and transferring. (Note: Some carriers do not require permanent diagnoses.)

Terminal illness: A physician-diagnosed medical condition that is expected to result in the death of the insured within a specified period of time, usually 12-24 months.

The following may apply to each or all of the benefits described above and vary by carrier:

» These benefits are typically available as a part of the policy contract and or may be offered as a rider on a contract.

» These benefits usually have a minimum and may allow for a percentage up to the full death benefit amount to be accelerated as long as the insured qualifies as stipulated in the policy and/or rider. However, many carriers cap the amount available below the full death benefit.

» These benefits may be offered at no cost at policy issue but charge a fee (fixed or formula) at time of access or may charge a premium in addition to the cost of the base policy.

» Electing to accelerate any amount of death benefit will reduce the amount a beneficiary receives upon the insured’s death.

» Chronic illness riders may or may not have an elimination period and may or may not be indemnity benefits.

» Qualified accelerated benefits that are received generally will not be subject to taxation under Section 101(g) of the Internal Revenue Code. However, receiving an accelerated benefit may affect the recipient’s rights to receive certain public funds, such as Medicare, Medicaid, Social Security and Supplemental Security Income. As with all taxable matters, clients should consult with a tax advisor to determine the tax consequences prior to electing to receive benefits.

Another life situation is disability. Although this does not trigger death benefit acceleration, many carriers offer a disability rider for an additional premium that pays the policy premiums, as stipulated in the rider, if the policy owner becomes disabled. This allows the policy owner to keep their life insurance death benefit and cash value without having to pay premiums while disabled.

The world and the economy continue to evolve, forcing the financial services and insurance industries to evolve to meet the demands of our new world. Your toolbox must expand to meet your prospects’ and clients’ holistic planning needs while you help them become smarter about how they plan and save and invest their money. Now is the time to add cash value life insurance to your planning toolbox if you haven’t done so already.

Using a SPIA to protect an IRA in Medicaid planning

Simplicity in it for the long haul

Advisor News

- Americans aren’t turning retirement plans into action, LIMRA finds

- Ashley Hinson ‘death tax’ story collides with truth

- How advisors can prepare clients for an uncertain retirement landscape

- Investors aren’t waiting out uncertainty

- Transamerica and Advo(k)ate Advisors launch pooled employer plan

More Advisor NewsAnnuity News

- Corebridge annuity sales slip ahead of Equitable marriage

- California teachers settle class-action lawsuit over in-plan annuity fees

- Jackson Financial CEO caps 40-year career with blockbuster Q2

- Lumos Insurance introduces the Immediate Care Plan to help families fund long-term care

- NAIC regulators begin consensus phase on annuity illustration overhaul

More Annuity NewsHealth/Employee Benefits News

- VARIABILITY IN REBIMBURSEMENT RATES FOR STATE-FUNDED ABORTION SERVICES FOR MEDICAID ENROLLEES: A 2026 UPDATE

- GOVERNOR NEWSOM ANNOUNCES APPOINTMENTS 8.7.26

- Small school districts unite to lower health costs

- Endorsing Janoo

- Ashley Hinson unveils insurance transparency bill amid scrutiny of her health care record

More Health/Employee Benefits NewsLife Insurance News

- Indiana eyes more oversight of insurance companies' exposure to private credit

- HEALEY-DRISCOLL ADMINISTRATION RETURNS $14.5 MILLION TO HEALTH AND DENTAL INSURANCE CONSUMERS AND BUSINESSES

- ‘Uniquely positioned’: Equitable outlines future post-Corebridge merger

- Don't keep checks with clerical errors

- The insurance distributor that builds its own software will win the next decade

More Life Insurance News