Benefits Boost Financial Wellness As Well As Physical Wellness

Traditional workplace benefits such as health insurance, dental insurance and accident insurance give employees the tools they need to protect their physical health. But what about their fiscal health? Can group benefits protect an employee’s financial wellness? Researchers at two benefits carriers say financial wellness benefits are the latest offerings to help a pandemic-battered workforce obtain some security.

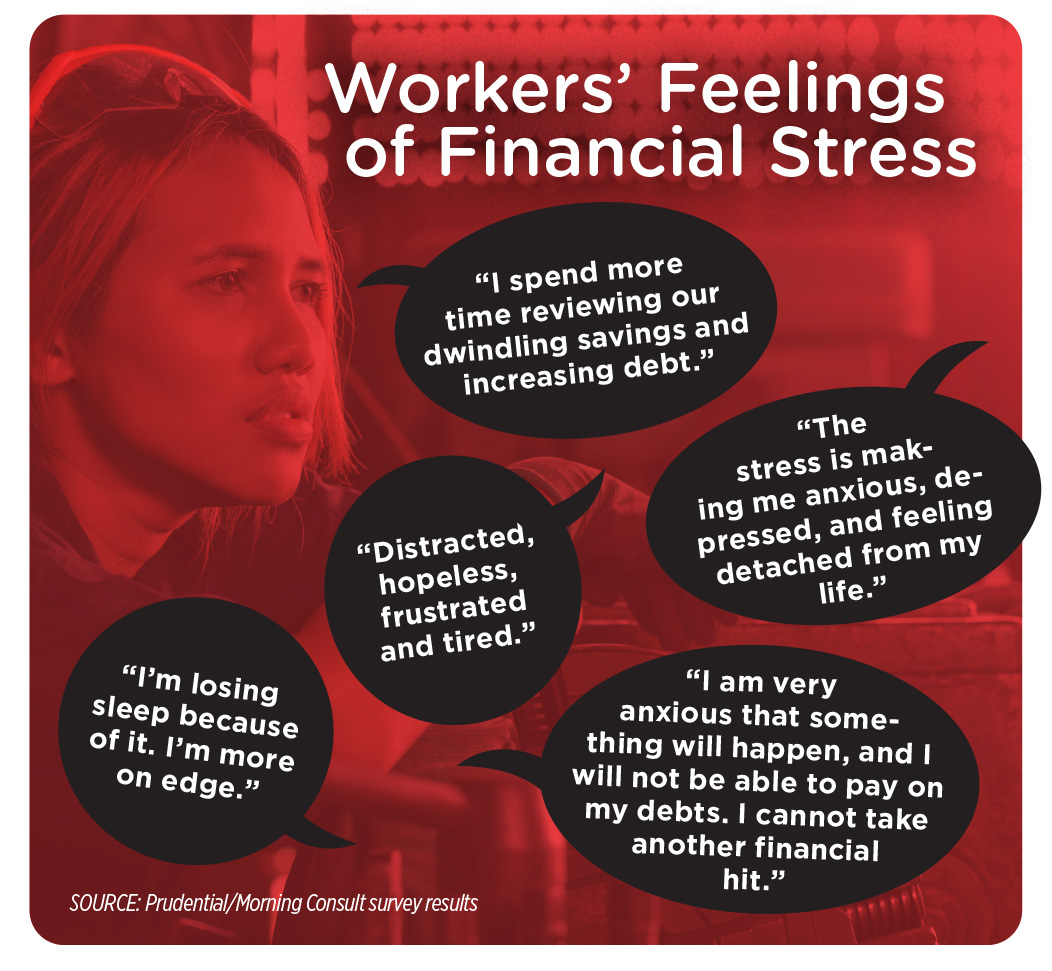

Workers who are highly stressed due to financial reasons are more likely than average to feel a range of negative emotions, Prudential reports, with the majority feeling worried (80%), frustrated (73%), exhausted (65%), low energy (58%), in fear (59%), sad (60%) and hopeless (51%). Some even report feeling depressed and suicidal.

“We found that about 29% of people who are experiencing financial problems also had some increased health risk, compared with about 11% of those who weren’t experiencing financial problems, said Suzanne Schmitt, Prudential vice president of financial wellness outcomes.

The COVID-19 pandemic has cast a bright spotlight on the interconnected challenges of managing mental and financial health, Prudential said in its report “The Tight Links Between Mental And Financial Health.”

In that report, Prudential said many American workers are struggling to manage day-to-day activities that look nothing like they did before. In many cases, they are worried about their mental and financial well-being. The many changes resulting from the pandemic, including quarantines, social isolation, remote work, virtual exhaustion and increased loneliness, each can have a dramatic effect on a person’s well-being.

The financial and mental stress brought about by the pandemic is damaging workers’ well-being, Prudential’s report said. In fact, loneliness and social isolation can be as damaging to health as smoking 15 cigarettes a day, according to the Health Resources & Services Administration.

More than half of Americans say their financial health has been negatively affected amid the COVID-19 pandemic. Among the 51% who say they’ve experienced a financial setback, some have seen devastating consequences. About 26% of the respondents to Prudential’s 2020 Financial Wellness Census had experienced an income disruption (whether due to furlough or reduced compensation or work hours), and 17% had seen their household income fall by half or more in the months following the virus’ outbreak.

The link between financial health and mental health is obvious in the Prudential report. Individuals who struggle to pay off their debts and loans are more than twice as likely as others to experience mental health problems, including depression and anxiety. The impact on a person’s mental health can be particularly severe if they resort to cutting back on essentials (e.g., food, heating, medicine, etc.), or if creditors are aggressive or insensitive when collecting outstanding debts.

Employees experiencing financial problems may miss significantly more days of work and hours of productivity than those who are not experiencing financial problems. Prudential found that employees who experience financial problems lose a full week of productivity compared to other employees. In addition, those who experience financial problems are more likely to experience a short-term disability.

Mental and financial health problems can devolve into a vicious circle in which one compounds the other. When employees experience poor mental health, earning and managing money may become challenging. In turn, this can create financial stress, anxiety, fear and worry.

Employers are seeing how financial wellness is an important part of their workers’ overall health. Prudential’s research showed 79% of employers surveyed reported their organization will focus more on total wellness (physical, mental and financial health) in the next year or two.

What can benefits brokers and their employer clients do to help ease workers’ fiscal stress?

“People don’t always know where to start, and the process can be overwhelming,” Schmitt said. “So, first of all, there’s a tremendous focus on providing an overall assessment of financial health and then start to frame some best actions.”

The second thing they are seeing is tremendous interest in programs that help employees with their emergency savings, she said. “And the next thing is working on employee debt management — having the conversation, bringing financial education coaching support into the workplace, working with expert counselors who can help workers get on a better path toward paying off their student loan debt or their credit card debt.”

Another benefit that could help workers’ financial health, Schmitt said, is caregiving support. A recent McKinsey & Co. survey showed that about one-quarter of women are considering leaving the workforce because of caregiving responsibilities.

Schmitt said some caregiver support could be offered through a company’s employee assistance program.

“But there are some additional benefits that are available from a range of vendors that will provide education for folks who might not know where to start, or what community services are available to them,” she said. “This will allow individuals to work with a licensed professional who’s going to personally evaluate their situation and put together a plan of care that is unique to that caregiver’s needs as well as the needs of the care recipient.”

One common goal of all employee benefits, Schmitt said, “is the ability for employees to be present and productive at work.”

Advisors have an opportunity, she said, “to really help employers understand that in addition to helping employees be happier, more engaged in their work by offering financial wellness programs, they also have the ability to help those employers improve their productivity and make a positive impact on their health care claims exposure.”

Guardian Life’s ninth annual Workplace Benefits Study also showed a link between financial wellness and employee benefits.

More than half (52%) of workers surveyed said they would face financial hardship without their workplace benefits, while 67% said they would not be able to afford benefits if they did not get them through their employer. If faced with an emergency medical bill, one-third said they would pay with a credit card, and about one in five would take out a bank loan, home equity loan, or borrow from their retirement plan or children’s college savings.

Before the pandemic, 39% of workers told Guardian they felt their financial health was excellent or very good. That percentage dropped to 33% during the pandemic. In addition, 74% of those who report high financial stress also have very high medical deductibles, while 76% of those who report high financial stress have college debt. In January 2020, prior to the pandemic, four in 10 full-time employees reported they were living paycheck to paycheck and believed they were losing ground financially.

The Family Tree Strategy That Keeps Money In The Family

Americans More Confident In Life Insurance Since COVID-19

Advisor News

- How much could failure to fund Social Security cost average Americans?

- How can more Americans achieve financial independence?

- Savers vs. spenders: How money management attitudes impact financial confidence

- Demonstrating the value of life insurance to Gen Z

- Poor money habits are a dealbreaker in a new relationship

More Advisor NewsAnnuity News

- Canvas steps into the direct-to-consumer market that has yet to take off

- The next growth phase in life/annuities depends on modernization

- CA judge certifies class action in teachers’ lawsuit over in-plan annuity fees

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Managing Director Joins ‘Target Topics’ Podcast to Discuss State of Delegated Underwriting Authority Enterprises Market

More Annuity NewsHealth/Employee Benefits News

- A Tale of Two Behavioral Health Systems, or How the State Border Determines Who Gets Access to Mental Healthcare

- Recent Findings from Iwate Medical University Provide New Insights into Science (Nonlinear Associations Between Sleep Duration and Incident LTCI Certification in Older Adults: Findings From the Iwate-Kenpoku Cohort Study): Science

- Researchers from Capital Medical University Detail New Studies and Findings in the Area of Managed Care (Factors Contributing To the Enrollment of Ambiguous Medical Insurance Cases: a Retrospective Study At a Tertiary Hospital In Beijing): Managed Care

- Studies from Cornell University Further Understanding of Managed Care (IRA Reforms To Medicare Part D Reinsurance Were Associated With Plan Exits And Higher Premiums, 2024-25): Managed Care

- New Managed Care Study Results from Yale University School of Medicine Described (Establishing Neonatal Toxicology Testing Protocols to Prioritize Clinical Utility Reduces Racial and Socioeconomic Bias): Managed Care

More Health/Employee Benefits NewsLife Insurance News

- USAA introduces Secure Start whole life program for children

- Best’s Market Segment Report: AM Best Maintains Stable Outlook on South Korea’s Non-Life Insurance Market

- Horace Mann Strengthens Customer Relationships and Accelerates Long-Term Growth Through Transactions with Medical Mutual of Ohio

- Regulators: ‘No firm conclusions’ from first offshore reinsurance filings

- Allianz Life Study Finds Americans Struggle to Shift From Retirement Saving to Spending

More Life Insurance News