Will Rising Mortgage Rates Squash The Housing Market?

Commentary

The historic spike in mortgage rates instigated chatter across the country that the housing market is a bubble that will soon pop.

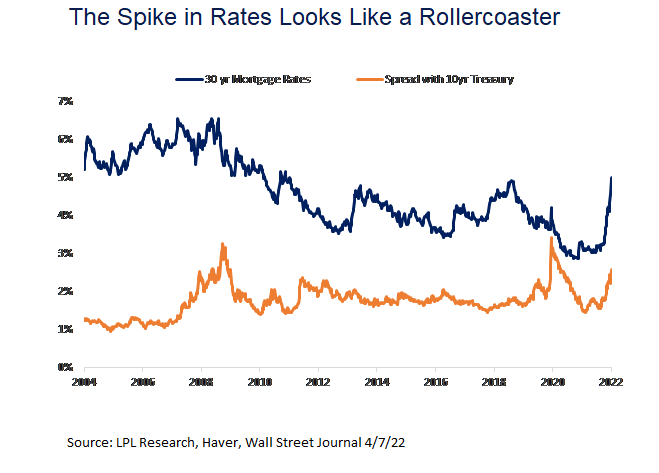

Mortgage rates made a steep climb recently as markets reacted to a newly-minted hawkish Federal Reserve. As seen in the LPL Chart of the Day, mortgage rates rose to levels last seen in 2011.

“Our view is the housing market is not necessarily a bubble, but rising rates will no doubt slow some of the irrational exuberance,” says Jeffrey Roach, Chief Economist at LPL Financial.

However, we don’t believe headwinds from higher rates will not fully negate the tailwinds of low inventory, pandemic reshuffling, and positive demographics. Other variables would have to turn over before the housing market materially declines.

Rates On The Rise

A 150-basis-point rise in mortgage rates is probably not enough to cause severe demand destruction.

Several months ago, a prospective homebuyer would pay $1,347 for a $300,000 loan at 3.50%. If the buyer waited until this week to lock in a new rate at 5.00%, the borrower would pay $263 more per month. For most households, an additional cost of $263 per month will cut into discretionary spending, and prospective buyers will reconsider housing options.

The initial response to higher rates will be most obvious for first-time prospective home buyers, who will bear the brunt of higher rates. This cohort will likely realign expectations or delay a home purchase altogether. But, those selling a current home could be more adaptable to higher rates, since this cohort can likely offset high costs with existing home equity.

Higher cost of funds will likely mean a cut in discretionary items most sensitive to relative price changes. Inflationary periods with high mortgage costs will weigh on the consumer but if rates stay contained, our baseline expectation is the consumer will wade through it.

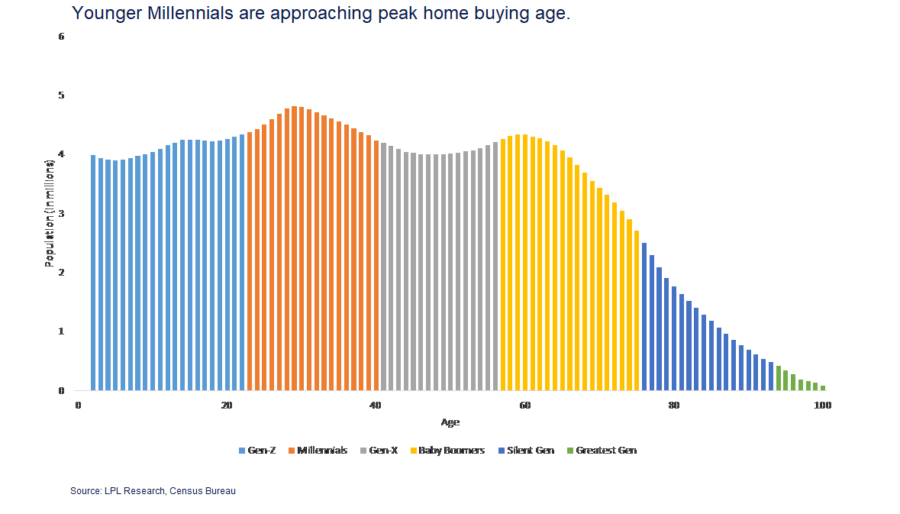

Here Come The Millennials

Long-term demographic trends will support housing. According to the latest data from the National Association of Realtors (NAR), the median age of first-time buyers has risen to 33.[1] The median age of repeat buyers is 55. The wave of millennials coming into peak buying age and high net worth of the boomers will help support the housing market even though mortgage rates and home prices are rising at an extraordinary pace.

Wage growth from a tight labor market also provides support in the near-term. Rising median age of repeat buyers, strong household net worth and low financial debt obligations explain why all-cash sales were roughly 30% of U.S. home purchases in 2021. As borrowing costs increase, all-cash sales will likely rise in 2022.

Years Of Underbuilding

Inventory of residential homes is at all-time lows according to Redfin Housing Market data. Other agencies corroborate: at the current sales rate of existing single-family homes, the entire inventory would deplete in less than two months. In some regions, inventory of homes is more scarce.

Perhaps some seasoned builders are reluctant to build after experiencing the Great Financial Crisis, but the lack of labor and high cost of raw materials weigh on builders. Therefore, we expect inventory to remain extremely tight, adding support to housing even during times of rising mortgage rates.

[1] https://www.nar.realtor/blogs/economists-outlook/age-of-buyers-is-skyrocketing-but-not-for-who-you-might-think#:~:text=The%20number%20that%20has%20changed,to%20a%20number%20of%20factors.

California Contractor Faces 21 Felony Counts Of Forgery, Theft, And Insurance Fraud

New Generation Of Women Investors Redefining Wealth And Influence

Annuity News

- Malibu Life Holdings Completes Acquisition of TruSpire, Establishing Malibu USA and Accelerating Entry into the U.S. Retail Annuity Market

- Why job boards are failing insurance agencies

- MassMutual Ranks No. 100 on the 2026 Fortune 500® List

- What’s fueling record annuity growth?

- Jackson Named InvestmentNews 2026 Annuities Provider of the Year

More Annuity NewsHealth/Employee Benefits News

- How health insurers get a free pass to deny coverage from a 52-year-old law meant to protect worker pensions

- Nation’s first state-run long-term care insurance program about to launch in WA

- Kim Reynolds creates Iowa Medicaid fraud task force as deficit grows

- West Virginia's youngest children are losing health care coverage

- Long-term care insurance launches

More Health/Employee Benefits NewsLife Insurance News

- NAIFA praises House committee approval of Clarity for Compensation Act

- PHL Variable liquidation pushed out to 2027, Connecticut regulators say

- ‘Recession-Proof’ Insurance Is Trending. Safety Net or Scam?

- Winged Keel Group Expands National Presence and PPLI Leadership, Welcomes SBSI, Inc. (dba NFP Insurance Solutions)

- MassMutual Ranks No. 100 on the 2026 Fortune 500® List

More Life Insurance NewsProperty and Casualty News

- What are the 'top workplaces' in the New Orleans area? Check out this year's awards.

- Insurity Unveils Agenda for Excellence in AI & Insurance, Showcasing How Insurers Are Turning AI into Operational Advantage

- GOVERNOR HOCHUL ISSUES NEW GUIDANCE TO IMPLEMENT REFORMS AIMED AT LOWERING AUTO INSURANCE PREMIUMS FOR NEW YORKERS

- REPS. CARTER, FIELDS, EZELL, BRESNAHAN INTRODUCE THE NFIP PREMIUM TRANSPARENCY ACT

- GARBARINO, FLOOD SECURE HOUSE PASSAGE OF BIPARTISAN TRIA REAUTHORIZATION ACT

More Property and Casualty News