Why Selling Insurance Can Solve Your Problems With Investments

By Todd Colbeck

What do you mean - problems with investments? The market is up, right?

I am not talking about problems with investment performance. I am talking about your problem bringing in new investments to manage. Oh, and you may have another problem - have you had any important clients transfer out lately?

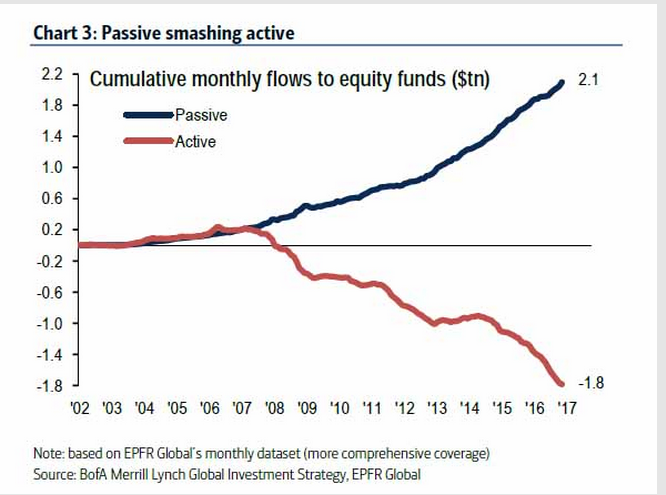

As I see it, the “problem” you have can be summed up in the chart below:

Can you guess where this trend will be in 10 years? Do you think it will reverse and go the other way? No.

Why do you think this this divergence started in 2008? In 2016, Vanguard raised $277 billion and Franklin Templeton lost $42 billion. A lot of those assets moving to Vanguard came from hard-working private wealth managers and financial advisors.

So if you are paid on assets under management, what is your plan to make up lost revenue? I guess you can fight fire with fire and take money back from Vanguard. Did you know they are now promoting their own financial advisors?

I want to discuss how you can increase your revenue significantly through insurance sales.

In my opinion, professionals who have both investment and insurance licenses typically sell about 10 percent as much insurance as professionals who have only an insurance license. Why is that? The clients are the same, the products are the same but the focus is completely different.

Without a focus on insurance, financial advisors do a poor job presenting. Next thing you know, clients are walking around unprotected and they are forced to draw down their investment accounts when something unexpected happens. Why? Because they didn’t have the proper insurance.

So why don’t clients buy something they obviously need? Because people hate buying what they “need.” People buy what they “want.” So how do we turn this dynamic around so people want insurance as much as they want a cool drink in the middle of the desert?

Clients already wanted to insure their house and their car, so why don’t they seem to want to insure their paycheck or even their life?

The key is asking the right questions that guide the client to that light bulb moment when they say, “Aha! I want this and I want it now.”

I find asking questions that focus on big-picture protection to be very effective. Why do you keep money in the bank instead of under the mattress? Why do you lock your car in the mall parking lot or on the street? Why do you install an alarm in your home? Because you want protection. Simple! Insurance is one of the most cost-effective protection strategies available.

That being said, let’s discuss how to create a want as well as a need.

It is human nature to be consistent. In his book, Influence: The Psychology of Persuasion, author Robert Cialdini named “consistency” as one of the six most important ways to create influence. Start by letting clients know that you wear two hats. One of your “hats” helps them make money. The other “hat” helps them protect that money. Ask clients what they think about those two hats. Ask which of those hats is more important for them and why. Then ask how important the other hat is and why.

When a client tells you why protecting their money is important, that is the No. 1 step toward being consistent. Every action you take to help clients decide on in the future must be consistent with their statement of why protecting their money is important. As soon as they make a decision conflicting with that statement, the uncomfortable feeling of inconsistency arrives – and you can point it out. Clients don’t necessarily want insurance per se, they want to be consistent with their stated values of protection.

Now you can start asking questions such as:

- Is your home protected?

- Are the contents of your home protected?

- Is your health protected?

- Is your transportation protected?

Most of the time, you will get four yes answers in a row. Now it’s time to ask the big questions.

- Is your paycheck protected if you become sick or injured and unable to work for six to 12 months?

- Are your future earnings protected for your family in case something should happen to you?

After your client gives four yes answers in a row, those last two questions will be very inconsistent if they reply with anything other than a yes.

Now ask your clients, based on their answers, what issue they think they should address first, second, etc. Let them know you will be happy to share some strategies at your next meeting and then see them again within two weeks and present your solutions.

The entire key to this process is that your client identified where they needed protection and told you their priorities. Why? Because they wanted to be consistent. If for some reason they said they didn’t want to be protected, go back to the values of what they already shared about protection.

After a meeting such as this, it should be easy to present the types of solutions that will provide the best protection for your client. I’m happy to help you take the questions we mentioned previously and kick them up to the next level.

Todd Colbeck, MBA, is owner of Colbeck Coaching Group, Miami Beach, Fla. He formerly was brokerage vice president of the northeast U.S. region at American Express Financial Advisors. Contact him at [email protected].

Lawmakers to Trump: Delay the DOL Rule

Financial Services Casting Nets For Younger Pros as Advisors Age Out

Advisor News

- Embracing a family-centric approach to financial planning

- Family communication: Financial planning’s growing blind spot

- Americans aren’t turning retirement plans into action, LIMRA finds

- Ashley Hinson ‘death tax’ story collides with truth

- How advisors can prepare clients for an uncertain retirement landscape

More Advisor NewsAnnuity News

- Investigation finds deceptive sales, churning of annuities targeting postal workers

- Corebridge annuity sales slip ahead of Equitable marriage

- California teachers settle class-action lawsuit over in-plan annuity fees

- Jackson Financial CEO caps 40-year career with blockbuster Q2

- Lumos Insurance introduces the Immediate Care Plan to help families fund long-term care

More Annuity NewsHealth/Employee Benefits News

- Louisiana hospitals see sharp uptick in uninsured patients after Obamacare subsidies expired

- CareScout Redefines Worksite Long-Term Care Insurance With a Solution That Goes Further for Employers and Employees

- Next Generation My Care – It’s here … now what?

- 4 common LTC missteps older Americans must avoid

- Missouri and Kansas can expect double-digit Obamacare premium hikes again

More Health/Employee Benefits NewsLife Insurance News

- Built to Last: Winston-Salem—a quiet industrial powerhouse

- The silver economy ushers in a new era of life insurance growth

- Family communication: Financial planning’s growing blind spot

- Indiana eyes more oversight of insurance companies' exposure to private credit

- HEALEY-DRISCOLL ADMINISTRATION RETURNS $14.5 MILLION TO HEALTH AND DENTAL INSURANCE CONSUMERS AND BUSINESSES

More Life Insurance News