Overcoming the all-or-nothing mindset

It is clear that there is a life insurance need gap — the difference between those who say they need life insurance and those who actually own it — and therefore a large opportunity for more individuals to obtain coverage. However, booming sales have not materialized. According to LIMRA, total U.S. retail life insurance new annualized premium fell 7% in the first quarter of 2023 to $3.7 billion. How do we grow this market?

One area to consider is helping consumers overcome the all-or-nothing mindset. This mindset refers to a thought process where individuals perceive things in extremes, considering situations or outcomes as either completely successful or completely unsuccessful. This mindset can make it challenging to find balance and to create realistic expectations. In many cases, individuals will just procrastinate and be inert.

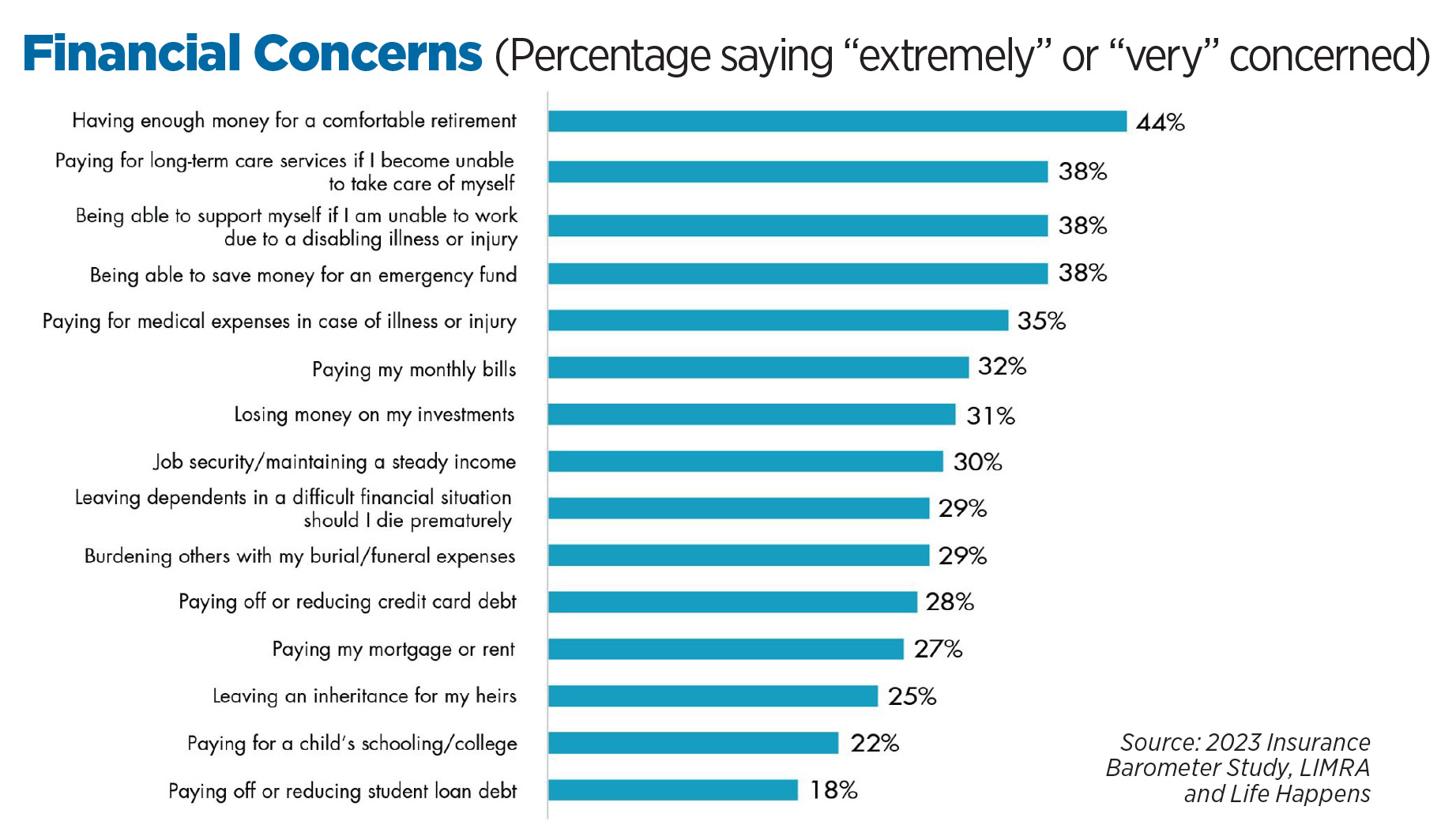

According to the 2023 Insurance Barometer Study, conducted by LIMRA and Life Happens, today’s consumers are trying to manage a multitude of financial concerns. Things such as saving money, paying monthly bills and paying down debt, or burdening others with their expenses are top of mind. These financial concerns could lead to consumer paralysis or result in consumers coming up with excuses. Two key reasons for not purchasing life insurance are “having other financial priorities” and “haven’t gotten around to it.”

Here are three things agents/advisors could do to help close the need gap.

1. Help individuals focus on small goals. Let them achieve and make progress. It doesn’t have to be all doom and gloom. Let them build momentum and see results.

In some cases, full-blown financial planning can be overwhelming and lead to customer concerns. According to a survey by Schroders, 76% of Americans say they feel overwhelmed by the thought of creating a financial plan and 56% say life is too uncertain for a plan to have any value.

2. Illustrate the impact of a dollar. Consumers can more easily visualize small dollar amounts through mental accounting. How much insurance could you buy instead of buying a latte? A relatively small change can amplify positive outcomes at relatively minimal cost.

There is also the potential to use subscription-based terminology and marketing to align with the growth of plans such as Netflix or Amazon Prime. According to eLabs, 64% of respondents say that they feel which connected to companies with which they have a direct subscription experience versus companies whose products they simply purchase as one-off transactions. In addition, 78% of adults globally have a subscription service.

3. Embrace digital in order to be relevant for younger consumers. For the first time, consumers are more likely to say they would prefer buying life insurance online than by any other method.

This is especially true for young adults. They expect a seamless experience and streamlined process that enables them to purchase coverage quickly and easily.

Younger customers also appreciate flexibility and personalized options. As you build trust over time, having the ability to offer your customers customized coverage based on their specific needs and budget will be crucial. You could start with simple and easy product options like term life insurance and increase coverage with other products as their circumstances change.

The financial services industry has always been based on relationships. That hasn’t changed. But to be effective, approaching these relationships must evolve to include a better understanding of clients’ needs, trying new sales tactics and embracing technology.

This will increase sales of life insurance across different and new demographics and help more Americans get the coverage they need to protect their loved ones.

Charting the course of life insurance

Annuities can help manage income risks in retirement

Advisor News

- Demonstrating the value of life insurance to Gen Z

- Poor money habits are a dealbreaker in a new relationship

- DC plan sponsors see opportunity in alternatives

- The American Dream: Redefined as financial stability

- Partial annuitization: How advisors can help clients balance income, growth

More Advisor NewsAnnuity News

- CA judge certifies class action in teachers’ lawsuit over in-plan annuity fees

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Managing Director Joins ‘Target Topics’ Podcast to Discuss State of Delegated Underwriting Authority Enterprises Market

- KBRA Assigns Rating to TruSpire Retirement Insurance Company

- Partial annuitization: How advisors can help clients balance income, growth

More Annuity NewsHealth/Employee Benefits News

- Douglas Veterans Claims Clinic Connects Rural Veterans With Critical Services

- Atrium pushes back after State Health Plan leaves healthcare network out of Tier 1

- Connecticut health insurance exchange shifts enrollment dates after federal changes

- Iowa health insurers propose premium increases for ACA customers

- NEW REPORT: THOUSANDS OF IOWANS FACING HIGHER HEALTH INSURANCE PREMIUMS NEXT YEAR THANKS TO ASHLEY HINSON

More Health/Employee Benefits NewsLife Insurance News

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Upgrades Credit Ratings of Sagicor Financial Company Ltd. and Most of Its Subsidiaries

- Trust, technology and the future of claims

- New York Life Launches an Indemnity Benefit for its Asset Flex Long-Term Care Insurance Solution

- AM Best Affirms Credit Ratings of DB Insurance Co., Ltd.

More Life Insurance News