Helping the public get an A+ in financial literacy

According to the most recent available Federal Reserve SCF data, the average retirement savings for Americans who are between the ages of 65 and 69 is $206,819. The highest average was among those 55-59 years old at $223,493. According to the Government Accountability Office, however, only about half of households age 55 or older have any retirement savings. About a third have no defined benefit plan or retirement savings, and about 20% have a defined benefit plan but no retirement savings. The remaining 52% have some retirement savings.

Those numbers are alarming.

There are some signs of hope, however. A recent BlackRock study found that Generation Z workers, ages 18-25, are saving an average of 14% of their income. So one might assume that financial literacy is improving among the younger generations. Among the older generations — millennials, Generation X and baby boomers — the average is 12%.

However, with nearly half the population having little or no retirement savings, there is definitely a shortfall when it comes to financial literacy.

A savvy advisor I recently had a conversation with suggested that financial literacy education should start in middle school. My wife, Lisa, is a middle school engineering teacher. If we’re teaching engineering in middle school, why not financial literacy? The advisor went on to say that in terms of retirement planning, even people who work in other aspects of the financial industry are not educated in what is needed to plan for their financial future and retirement. It’s a different set of skills.

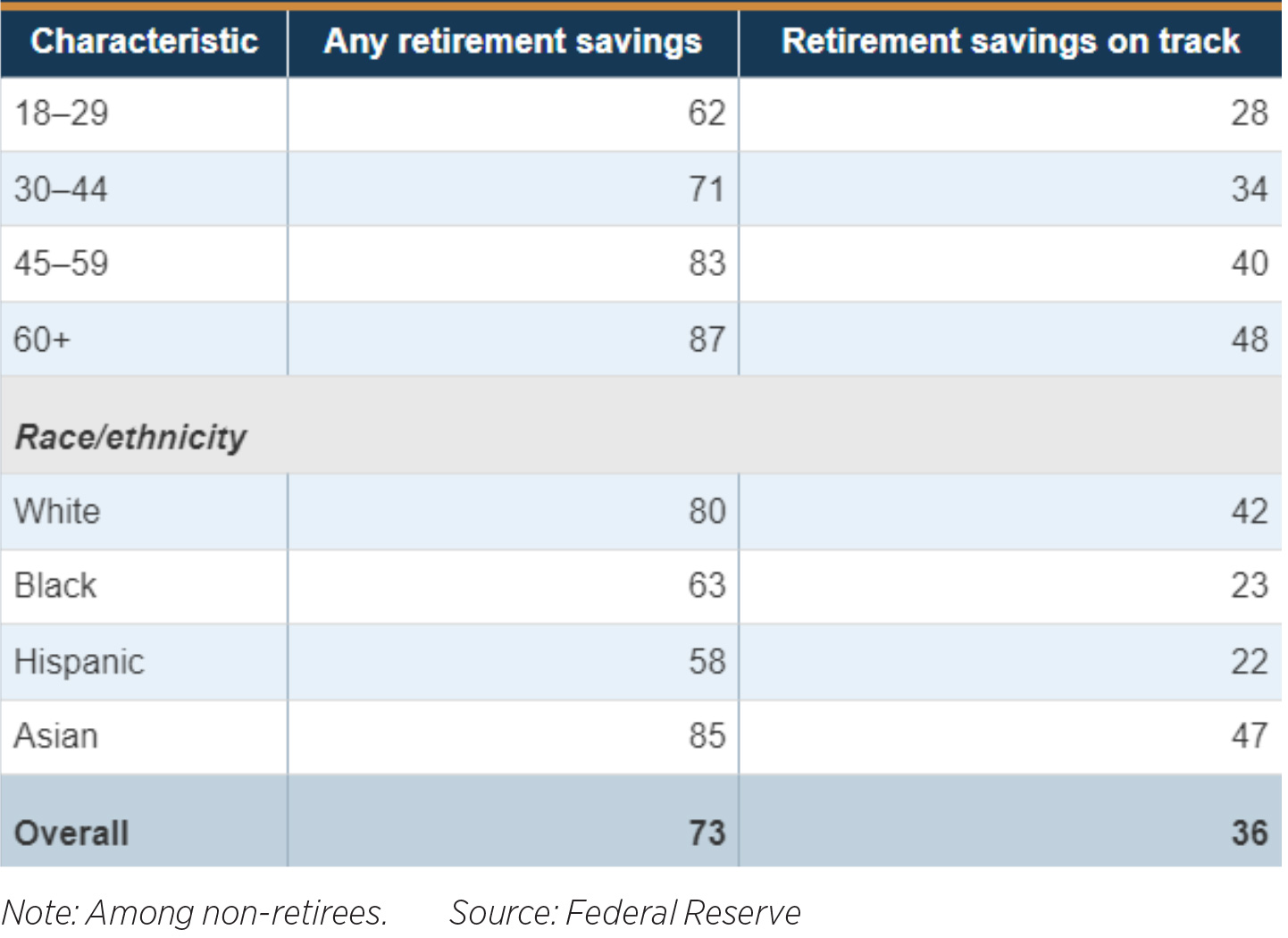

About one-fourth of non-retirees have no retirement savings at all, according to the Federal Reserve. And only about one-third of non-retirees believe their saving plan is on track. And the breakdown by race/ethnicity shows an even greater disparity.

While 42% of white people believe their retirement savings is on track, that percentage drops to 23% for Blacks and 22% for Hispanics. And while 80% of whites have at least some retirement savings, that percentage drops to 63% for Blacks and 58% for Hispanics. (See chart.) So there is also a disparity in financial literacy across racial and ethnic groups, and, in fact, a more intense need for financial literacy.

While it’s alarming that only 40% of those ages 45-59 believe their retirement savings are on track, according to the Federal Reserve, it’s also alarming that only 34% of those ages 30-44 believe they are on track. As we know, the earlier people start saving for retirement, the greater chance they have at meeting their retirement savings goals.

Obviously, improved financial literacy is better for all: those who are managing their budgets and planning effectively for retirement, and for the financial advisor community, since improved literacy would provide a greater pool of the public seeking financial assistance.

It’s also clear that there is a large percentage of the public in the middle-aged demographic who need financial advice and help steering their retirement planning onto a better course. For them, the need is more urgent.

I noticed recently that Schwab MoneyWise has a feature on its site called “Ask Carrie.” Certified financial planner Carrie Schwab-Pomerantz offers the kind of advice that the public needs in order to become financially literate.

She does so in a format that we’ve all come to recognize and be comfortable with — the advice column — and which doesn’t reek of making an overt sales pitch, but only offers sound advice. This type of approach is one of many possible methods of addressing the need for financial literacy. There is no right or wrong way, but more outreach is needed. There are many ways to connect — through advice columns or blogs on your website, a regular podcast, newsletters — maybe even offering a seminar at your local high school. Letting the public know that you are there to offer help and advice is a crucial step in helping to turn the tide and improve financial literacy.

Welcome to FPA

As we strive to broaden the voices in the magazine, we are working to expand the number of professional associations providing useful information and discussion for our readers.

With this issue, we welcome the Financial Planning Association to our pages with their first article, “Pro bono financial planning benefits society and advisors,” which takes a look at how offering your time and guidance can make you a better financial planner. FPA is the leading membership organization for Certified Financial Planner professionals and those engaged in the financial planning process, and we know the association will add to the valuable discussions and provide actionable information for our readers. Welcome to FPA!

John Forcucci

Editor-in-chief

The how and when of texting clients

Helping clients navigate difficult estate-planning conversations

Advisor News

- The McEwen Group Merges with Prairie Wealth Advisors to Form Billion Dollar RIA

- Guaranteed income streams help preserve assets later in retirement

- Economic pressures make boomerang living the new normal

- Pay or Die: The scare tactics behind LA County’s Measure ER tax increase

- How to listen to what your client isn’t saying

More Advisor NewsAnnuity News

- Guaranteed income streams help preserve assets later in retirement

- MassMutual turns 175, Marking Generations of Delivering on its Commitments

- ALIRT Insurance Research: U.S. Life Insurance Industry In Transition

- My Annuity Store Launches a Free AI Annuity Research Assistant Trained on 146 Carrier Brochures and Live Annuity Rates

- Ameritas settles with Navy vet in lawsuit over disputed annuity sale

More Annuity NewsHealth/Employee Benefits News

- HAFA takes legal action against New York state

- Understanding Advantage Plans and Supplements

- Dawson County commissioners renew county health insurance after confusion in meeting

- BEACH BILL TO REQUIRE HEALTH INSURERS TO COVER STUTTERING TREATMENTS ADVANCES

- Voluntary healthcare cost limits aren't working. Should Rhode Island's insurers face sanctions?

More Health/Employee Benefits NewsLife Insurance News

- Industry Innovator Scores New High-Water Mark: Reliance Matrix Logs 8 Millionth Employee Benefit/Absence Claim

- $150M+ asset sale payout distributed to Greg Lindberg policyholders

- Best’s Market Segment Report: AM Best Revises Outlook on France’s Non-Life Insurance Segment to Stable from Negative, Reflecting Top-line Growth, Technical Profitability

- Pacific Life Launches New Flagship Variable Universal Life Insurance Product

- NAIFA launches “NAIFA Cares” initiative to help build long-term financial security for children

More Life Insurance News