Genworth LTC rate increases helping insurer gain strength

Court settlements and rate actions are helping Genworth massage losses with its block of troubled long-tern care policies, executives said Wednesday.

Speaking on a conference call with analysts, Dan Sheehan, chief financial officer and chief investment officer, said LTC claims are more severe in 2022. The end of the COVID-19 pandemic restrictions contributed to a shift away from home-based care back to more costly facility care, he noted.

"Claim severity continued to increase in the current quarter as expected, given the aging of the block," Sheehan said. "Our newer blocks of business, which are beginning to enter into their claim years, have higher daily benefit amounts and inflation coverage than the older LTC blocks."

Payouts related to a pair of class-action settlements are also impacting the bottom line, Sheehan said. They are:

- In Halcom vs. Genworth Life Insurance, plaintiffs alleged that that Genworth withheld material information from policyholders relating to the "full scope and magnitude" of Genworth’s future rate increase plans and to Genworth’s reliance on obtaining such rate increases to be able to pay future claims. A settlement was reached this summer offering class members various benefits options along with payouts to certain members.

- Similar claims were made in Skochin vs Genworth Life Insurance, which preceded the Halcom lawsuit. The resulting settlement offering members various options to continue benefits.

Settlement impacts will continue into 2023, Sheehan said. "However, based on our experience with the Choice 1 settlement [Skochin], we believe that overall, the settlements are favorable to both the policyholders and Genworth and will reduce our tail risk on our LTC block," he said.

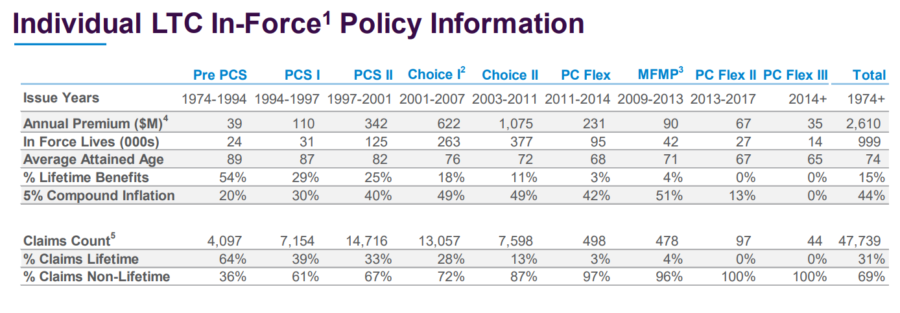

Genworth provided a snapshot of the roughly 999,000 LTC policies it continues to manage:

The two largest blocks, Choice I and Choice II, represent "more than half" of Genworth's total book of LTC policies, said President and CEO Tom McInerney. With the average ages of the Choice policyholders in the early-to-mid 70s, the insurers is looking at another 10-12 years until the "peak claim years" begin, he noted.

The earnings

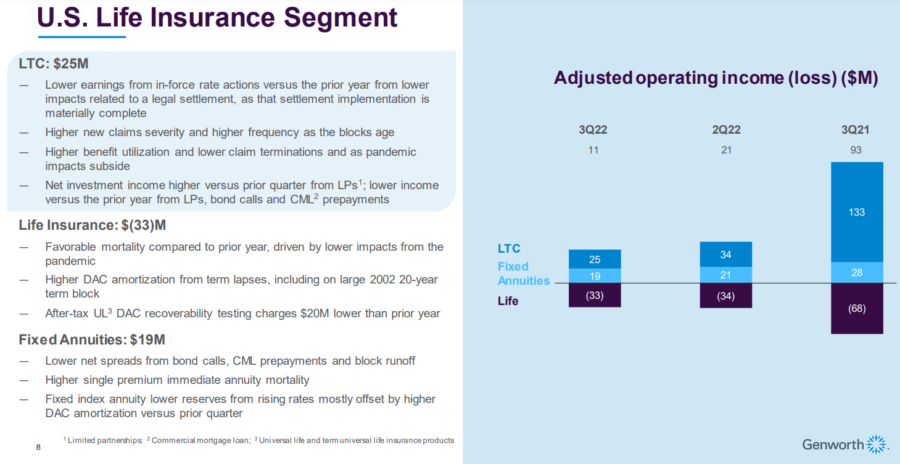

Genworth reported third-quarter net income of $104 million. The Richmond, Virginia-based company said it had profit of 20 cents per share. Earnings, adjusted for one-time gains and costs, came to 31 cents per share.

The financial services company posted revenue of $1.84 billion in the period. Its adjusted revenue was $1.91 billion.

The insurer received additional settlement news last month when a federal judge approved a $25 million settlement between Genworth and a class of more than 13,400 plaintiffs alleging that policyholders of the company’s Gold and Gold II universal life insurance policies were subject to unlawful cost of insurance (COI) increases.

But it is long-term care where Genworth made the most waves. The insurer was a major force when LTC policies recorded their highest sales in the early 2000s. Then lapse rates did not match assumptions, people lived longer and more extensive care options evolved, and interest rates fell to near zero. These factors sent Genworth scrambling to regulators in need of rate hikes on its LTC books. It continues to seek rate hikes in many states today.

"During the first 9 months of 2022, we received LTC in-force rate action approvals impacting $610 million of annualized in-force premiums with a weighted average increase of 33%," Sheehan reported. "The resulting $200 million in incremental annual premium increases brings the total net present value from achieved LTC rate actions to $21 billion since 2012, up approximately $1.4 billion since year end."

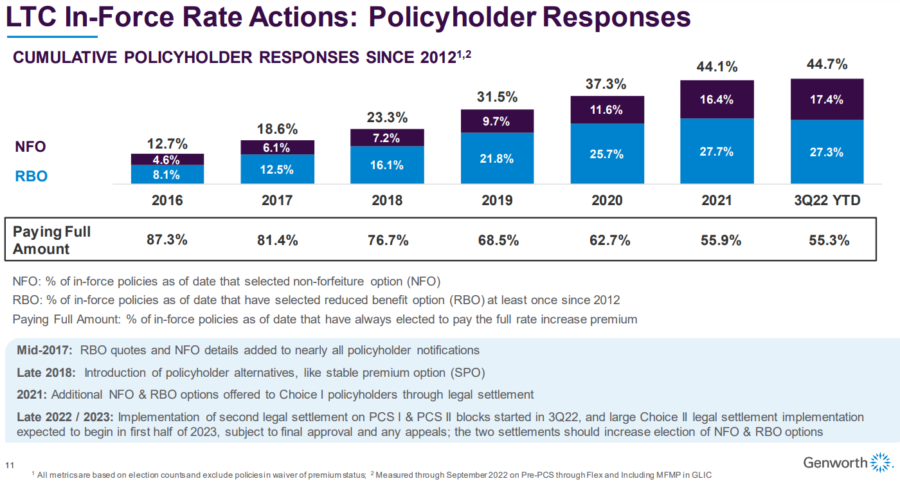

In addition to ongoing rate hikes, insurers are also offering reduced benefits (RBO) and non-forfeiture (NFO) options to policyholders. A nonforfeiture benefit is designed to ensure that if a policyholder lapses after a specified number of years, they retain some benefits from the policy.

There are currently two common types of nonforfeiture benefits being offered with certain insurance policies covering long term care services: a "reduced paid-up benefit" and a "shortened benefit period."

Genworth executives report a surge of policyholders opting for both options:

New active claims remain below pre-pandemic levels, Genworth reported:

Healthcare inflation is another variable for Genworth to contend with in the years to come, one analyst noted. U.S. healthcare expenditures are forecast to increase 6.2% annually in nominal dollars through 2026, according to Healthcare: United States, a report recently released by Freedonia Focus Reports.

McInerney told analysts he is not especially concerned about inflation, although Genworth is experiencing some of its effects.

"When we look at inflation in particular, just as with all our assumptions, we look over the long term. We've got obligations over the next 20, 30, 40, 50 years. So we have to look over that longer term.

"On top of that, there are offsets to inflation. So for example, when inflation is up interest rates tend to be up, and that's a good guide that offsets the bad guide that comes with inflation."

InsuranceNewsNet Senior Editor John Hilton has covered business and other beats in more than 20 years of daily journalism. John may be reached at [email protected]. Follow him on Twitter @INNJohnH.

© Entire contents copyright 2022 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

How commercial insurers can nurture a new generation of small businesses

Workplace financial well-being programs continue to expand

Advisor News

- Dutch gambling tax hike falls short as prediction markets eye World Cup

- Caregiving: A challenge that costs employers billions

- Could your practice benefit from an advisory board?

- SEC nears settlement with accused scammer Tai Lopez

- The 3 things that shrink your Social Security income

More Advisor NewsAnnuity News

- Globe Life Inc. (NYSE: GL) Highlighted for Surprising Price Action

- Trademark Application for “EMPOWER YOUR MONEY” Filed by Empower Annuity Insurance Company of America: Empower Annuity Insurance Company of America

- Built-in guaranteed annuities: What advisors should know

- Malibu Life Holdings Completes Acquisition of TruSpire, Establishing Malibu USA and Accelerating Entry into the U.S. Retail Annuity Market

- Why job boards are failing insurance agencies

More Annuity NewsHealth/Employee Benefits News

- Colorado hospitals poised to receive $455 million Medicaid funding boost

- Nevada sees drop in health insurance marketplace enrollment as subsidies lapse

- NYC Expands Outreach to Help Residents Keep Health Coverage

- 'We have to be smart about it'

- Georgia can do more to protect health coverage for its youngest residents

More Health/Employee Benefits NewsLife Insurance News

- THINGS YOUR CLIENTS SHOULD KNOW BEFORE SELLING A LIFE INSURANCE POLICY

- Could your practice benefit from an advisory board?

- AM Best Revises Outlooks to Stable for Missouri Farm Bureau Group’s Members and Farm Bureau Life Insurance Company of Missouri

- Globe Life Inc. (NYSE: GL) Highlighted for Surprising Price Action

- AM Best Assigns Credit Ratings to China Ping An Insurance (Hong Kong) Company Limited

More Life Insurance News