Customizing FIAs with riders meets a broad set of client needs

What truly builds trust in the financial world? It’s more than just offering the right products. It’s also about delivering personalized solutions — the kind that speak directly to a client’s specific fears and provide clarity amid uncertainty.

In our business, sustained growth comes from solving the client’s most complex problems. Right now, that problem is simple: Retirees need protected growth and ironclad income guarantees. This need is driving the massive momentum behind fixed indexed annuities.

Why FIAs are your sales engine

LIMRA showed FIA sales were $93.8 billion in the third quarter of 2025, slipping 1% from record results posted in the nine months of 2024.

Although the base FIA contract is a solid foundation — offering principal protection (a 0% floor) and a tax-deferred, index-linked upside — it is the strategic utilization of optional riders that transforms the product into a tailored solution. These riders are essential for customizing the contract and delivering individualized value to every client.

Why base FIAs require customization

A base FIA is a great tool, providing a floor of 0% protection and the potential for greater index-linked interest crediting. However, a single, standardized contract can’t solve every intricate client need. A “vanilla” FIA protects principal, but it doesn’t address the client’s specific, deep-seated anxieties: outliving money, protecting the spouse, unforeseen medical costs or ensuring efficient wealth transfer.

Advisors who focus solely on caps and participation rates miss the real marketing edge. Diagnose these precise risks and build the corresponding layer of assurance. We position the rider not as an optional add-on, but as a critical, customizable component designed to meet the client’s risk-need-time profile.

The three pillars of risk mitigation

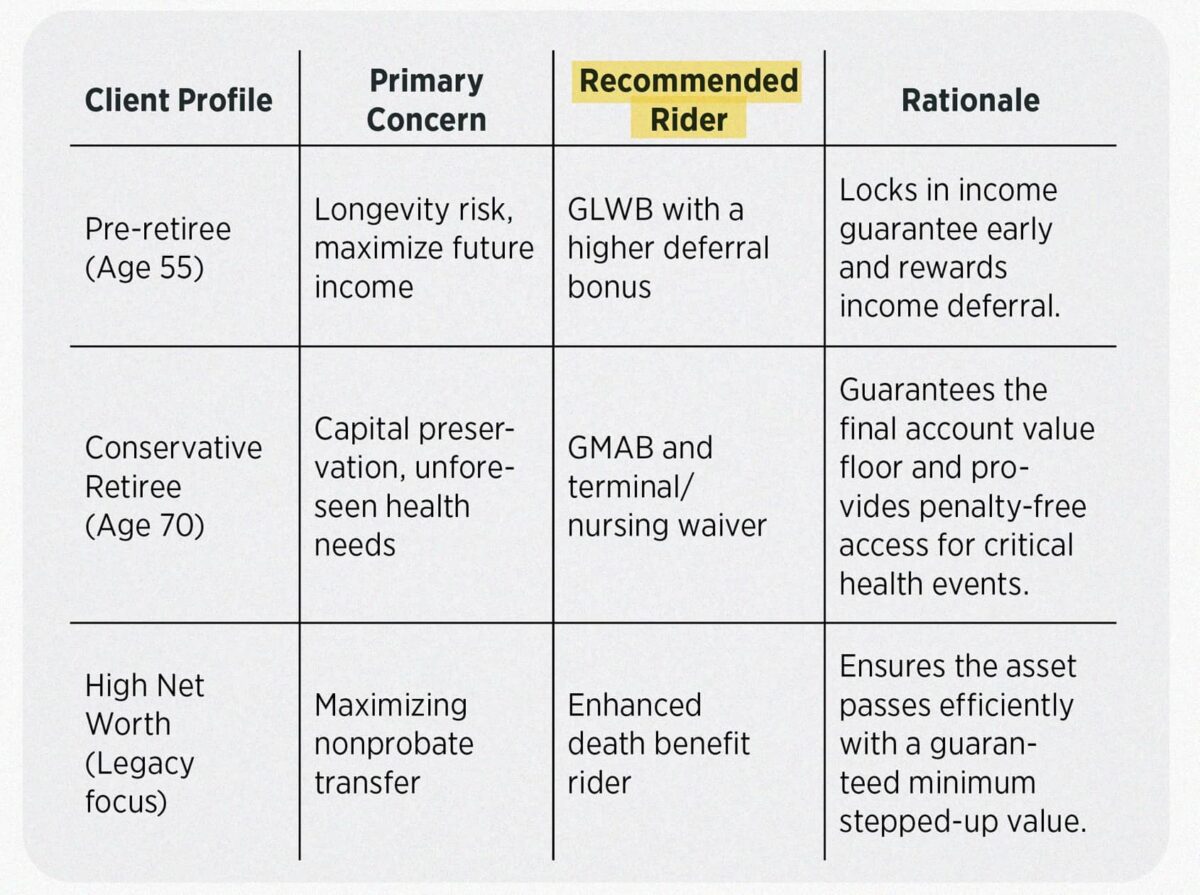

Successful agents train to match each client to one of these three rider categories: income, accumulation or legacy.

1. The income pillar: the guaranteed lifetime withdrawal benefit guarantee

Longevity risk — the fear of outliving one’s money — is perhaps the most significant psychological barrier facing retirees today. The guaranteed lifetime withdrawal benefit rider is our most decisive countermeasure against this fear.

This feature provides a contractual guarantee: a percentage of the benefit base that the client can withdraw every year, for life, regardless of how the actual accumulation value performs. Furthermore, the income stream is calculated using a separate benefit base that often grows at a guaranteed rate of return during the deferral period. This mechanism is a game-changer for clients seeking predictable cash flow.

The value of this guarantee translates directly to asset retention. Contracts with a GLWB rider consistently demonstrate higher client persistence. For example, a joint study by the Society of Actuaries and LIMRA showed that surrender rates dropped significantly. Approximately 10% of contracts with a GLWB were surrendered in the year the surrender charge expired, compared with 33% for those without. The guaranteed lifetime income stream creates emotional lock-in that transcends mere performance anxiety.

2. The accumulation and protection pillars: GMAB and GMIB

For clients who are earlier in the accumulation phase or who demand maximum certainty in their final contract value, we turn to guaranteed minimum riders.

» Guaranteed minimum accumulation benefit: This rider assures the contract value will reach a specified minimum amount at the end of the surrender period. This protects assets against years of low index performance and ensures a baseline return regardless of market volatility.

» Guaranteed minimum income benefit: When the client plans to annuitize, they use this feature. The GMIB establishes a minimum floor for future income payouts, providing a stable target for retirement income planning.

3. The legacy pillar: Enhanced death benefit

Many high-net-worth clients, or those focused on nonprobate asset transfer, use FIAs for wealth preservation. The enhanced death benefit rider makes this possible, especially when legacy is the priority. This rider ensures that beneficiaries receive the greater of the actual accumulation value, the total premium, or a value that has grown at a set, guaranteed interest rate. This strategically bypasses market downside and ensures maximum efficiency for generational wealth transfer.

The advisor’s guide: Matching riders to client goals

We train our agents to use a simple risk assessment framework. Match the product’s customization to the client’s most significant psychological need.

Maximizing value: Transparently addressing costs

As we know, these valuable riders come at a cost. Riders typically incur an explicit annual fee, generally ranging from 1% to 1.5% of the benefit base. Since this fee is deducted from the accumulation value, a year of zero index credit results in the contract value declining by the fee amount. We must address costs clearly, as transparency is the cornerstone of trust and the best-interest standard.

This is the strategic conversation point: The value of the guaranteed benefit must demonstrably outweigh the ongoing cost. If the client has ample retirement savings and minimal longevity risk, paying the fee is unnecessary and would be a drag on potential growth. Use sophisticated analysis to prove that for the client who needs the guarantee, the cost is a highly effective premium for essential risk transfer.

Move beyond selling a product to providing a fully engineered financial strategy. Master the diagnostic approach and become the go-to guide on rider utilization to elevate your practice. Remember, you are not just selling an annuity; you are selling certainty — the one guarantee every retiree truly needs and the path to your agency’s growth.

Congress unlikely to take up major health care legislation this year

The April explosion

Advisor News

- How much could failure to fund Social Security cost average Americans?

- How can more Americans achieve financial independence?

- Savers vs. spenders: How money management attitudes impact financial confidence

- Demonstrating the value of life insurance to Gen Z

- Poor money habits are a dealbreaker in a new relationship

More Advisor NewsAnnuity News

- Canvas steps into the direct-to-consumer market that has yet to take off

- The next growth phase in life/annuities depends on modernization

- CA judge certifies class action in teachers’ lawsuit over in-plan annuity fees

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Managing Director Joins ‘Target Topics’ Podcast to Discuss State of Delegated Underwriting Authority Enterprises Market

More Annuity NewsHealth/Employee Benefits News

- Covered California rates to jump nearly 10% as thousands struggle to afford coverage

- A Tale of Two Behavioral Health Systems, or How the State Border Determines Who Gets Access to Mental Healthcare

- Recent Findings from Iwate Medical University Provide New Insights into Science (Nonlinear Associations Between Sleep Duration and Incident LTCI Certification in Older Adults: Findings From the Iwate-Kenpoku Cohort Study): Science

- Researchers from Capital Medical University Detail New Studies and Findings in the Area of Managed Care (Factors Contributing To the Enrollment of Ambiguous Medical Insurance Cases: a Retrospective Study At a Tertiary Hospital In Beijing): Managed Care

- Studies from Cornell University Further Understanding of Managed Care (IRA Reforms To Medicare Part D Reinsurance Were Associated With Plan Exits And Higher Premiums, 2024-25): Managed Care

More Health/Employee Benefits NewsLife Insurance News

- USAA introduces Secure Start whole life program for children

- Best’s Market Segment Report: AM Best Maintains Stable Outlook on South Korea’s Non-Life Insurance Market

- Horace Mann Strengthens Customer Relationships and Accelerates Long-Term Growth Through Transactions with Medical Mutual of Ohio

- Regulators: ‘No firm conclusions’ from first offshore reinsurance filings

- Allianz Life Study Finds Americans Struggle to Shift From Retirement Saving to Spending

More Life Insurance News