Advisors must help clients plan for rising health care costs in retirement

Government spending on health care for older Americans has been flat but that doesn’t mean health care spending has remained the same. In fact, while government spending on Medicare has been stable, the program’s beneficiaries continue to see their out-of-pocket health care costs increase – and those costs will keep going up.

In a recent brief, HealthView Services revealed that while the average annual cost to the government per Medicare beneficiary has not significantly increased since 2010, demographic changes are driving health care costs upward.

The first baby boomers started to retire in the late 2000s, and have been turning age 65 at a rate of around 10,000 a day since. Driven by this demographic wave, the number of Medicare recipients has increased by 39.8% since 2010 (from 47.2 million to 65.8 million) and the proportion of the 65-and-over population has skewed younger and healthier, compared to more than a decade ago.

Since health care costs are highest toward the end of retirement as health declines, the average annual cost per retiree under Medicare will be lower for a younger population. Looking forward, aging boomers will make for an older and less healthy retiree population. This will result in significantly higher average per beneficiary expenses, assuming all else remains equal.

Improvements in health care, the more efficient service delivery, higher out-of-pocket costs due to increased cost-shifting to retirees, and the ability of the government to negotiate expenses with providers have played a modest role in slowing the pace of rising health-care costs, HealthView said.

Although Medicare Advantage enrollment has increased dramatically over the last decade – which was expected to reduce costs to the government – industry data indicates that this too, has not had a particularly beneficial impact on government costs, HealthView said. In fact, there is evidence that the opposite may be true. Advisors and retirees need to focus on the big picture.

“Health care cost increases are happening in pre-retirement and in retirement as well,” said Ron Mastrogiovanni, HealthView Services president. “We are taking more responsibility for total health care costs whether you are in retirement or pre-retirement.”

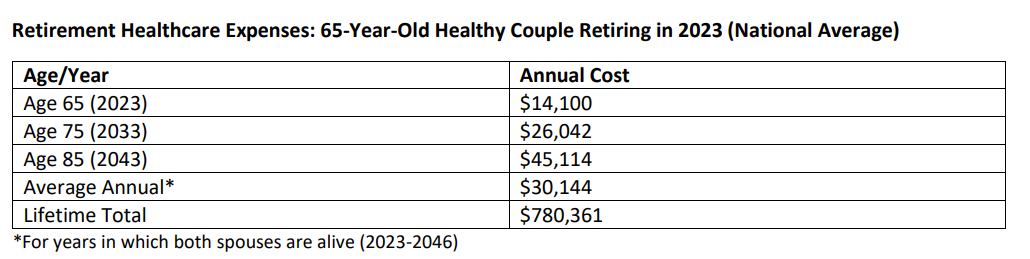

Medicare costs have increased 73% since 2011, from $522.9 billion to $905.2 billion in 2022. HealthView’s actuarial data, which is based on 530 million actual health care claims, shows that annual total health care costs for 65-year-old retirees have increased by 60% since 2011. A healthy 65-year-old couple would have spent $8,900 in 2011 on Medicare Part B and D premiums, supplemental insurance, dental insurance and out-of-pocket costs for hospitalization, doctor visits, tests, prescription drugs, dental, vision and hearing. Today, a 65-year-old couple will spend $14,100 – an increase of $5,200.

Lifetime health care costs for a 65-year-old couple starting Medicare in 2023 will be substantial, HealthView said, with the decades-long trend of health care costs rising at 1.5–2 times consumer price inflation expected to continue. For all premiums and out-of-pocket expenses, HealthView’s data shows this hypothetical couple should expect more than $780,000 (future value) in total retirement health-related expenditures. This assumes they live to actuarial life expectancy of 88 (male) and 90 (female). To address these expenses, they will need to have saved $260,995 at retirement, assuming a 6% return on their portfolio, annual withdrawals to fund all costs less Medicare Part B (funded via Social Security), and a balance at longevity of zero.

HealthView expects that Medicare premiums will continue to increase, and retirees should anticipate picking up more of the cost of health care. Changes to the Social Security Full Retirement Age and benefit payouts based on claim age are also likely.

In preparing clients for retirement, advisors must “make them aware of the reality of health care costs,” Mastrogiovanni said.

“Health care costs become important from a financial planning perspective. People need to understand what that total number will be, just like the total number for housing, food and transportation.

“The consumer who works with an advisor has choices. They can use insurance products, they can use capital market products, they can use a combination of the two to address the problem of covering health care costs. The advisor can guide them on what's the best solution for them.”

Susan Rupe is managing editor for InsuranceNewsNet. She formerly served as communications director for an insurance agents' association and was an award-winning newspaper reporter and editor. Contact her at [email protected]. Follow her on Twitter @INNsusan.

© Entire contents copyright 2023 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

Whatever happened to Medicare For All?

Business owners worry about gaps in insurance coverage, survey finds

Advisor News

- Nearly half of nonretirees doubt they will fully retire

- How much could failure to fund Social Security cost average Americans?

- How can more Americans achieve financial independence?

- Savers vs. spenders: How money management attitudes impact financial confidence

- Demonstrating the value of life insurance to Gen Z

More Advisor NewsAnnuity News

- Jackson CEO Laura Prieskorn to retire at the end of 2026

- Has your annuity been reinsured in the Cayman Islands? Here’s why it matters

- DOL slams pension risk transfer lawsuit as ‘opportunistic’ litigation

- AM Best Affirms Credit Ratings of New York Life Insurance Company and Its Subsidiaries

- Advisors don’t have an annuity problem; they have an integration problem.

More Annuity NewsHealth/Employee Benefits News

- They harvest the nation’s food, but a new rule may strip them of health insurance

- A new option for long-term care costs

- Rising health insurance exchange costs are bad news for Mississippi's working poor

- Iowa health insurers propose premium increases for ACA customers

- IOWANS ARE HOLDING ASHLEY HINSON ACCOUNTABLE FOR RAISING THEIR HEALTH INSURANCE PREMIUMS

More Health/Employee Benefits NewsLife Insurance News

- AM Best Comments on Credit Ratings of Horace Mann Educators Corporation and Its Subsidiaries Following Announced Transaction with Medical Mutual of Ohio

- AM Best Affirms Credit Ratings of Hanwha General Insurance Company Limited

- Globe Life boosts Q2 earnings, eyes AI shift for long-term growth

- ATTORNEY GENERAL BRENNA BIRD LEADS FIGHT TO PROTECT IOWA PENSIONS

- AM Best Affirms Credit Ratings of Bao Viet Insurance Corporation

More Life Insurance News