Whole life insurance: Is simple really better?

Simplicity is the buzzword of the moment, but when it comes to life insurance, the pursuit of simplicity might be stripping away options that could provide important value to the client.

OneAmerica® believes the insurance carrier’s role is to educate clients by clearly communicating the value of the product and its associated options. We should be removing complicated messages and misconceptions about the product for clients, not eliminating intricacies that make the product valuable. By building relationships and having trusted conversations about whole life insurance with your clients, you can tailor coverage to their unique goals and needs.

Decoding complexity

Adapting coverage to specific needs is effectively done via optional riders. These riders add versatility to whole life insurance. But they can sometimes make the products seem more complicated. However, instead of removing these options, we just need to explain them better. This is one of the ways financial professionals bring value to their clients.

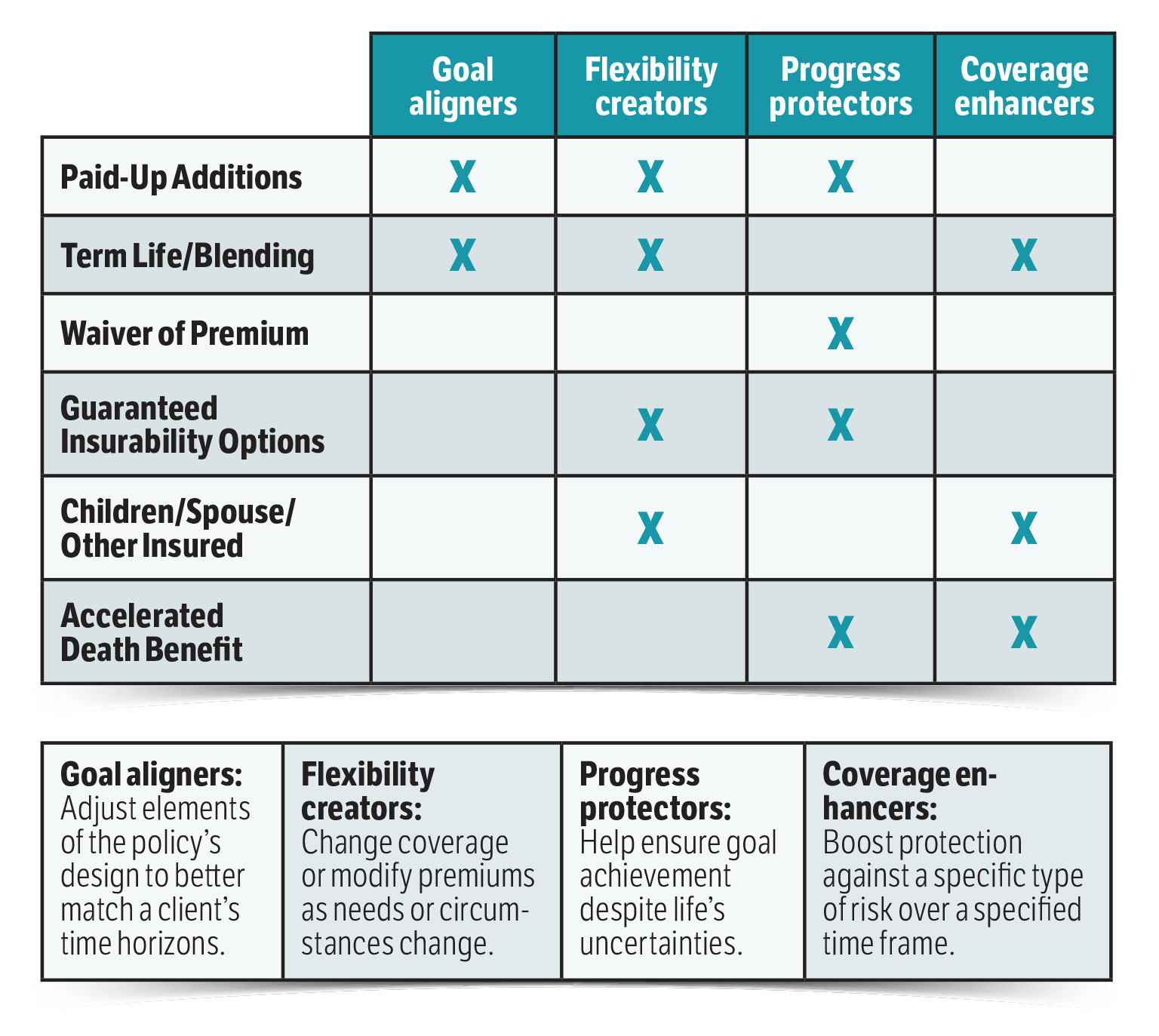

The goal should be to maintain whole life’s valuable complexities while making our communication about them more accessible. One approach is to categorize the goals that riders help achieve.

These categories allow you to clarify the unique benefits of each type of rider, which may enable clients to better understand their options. In some cases, a single rider may span multiple categories. An additional term life insurance rider, for example, is designed as a coverage enhancer, offering a boosted coverage amount for a designated period. Simultaneously, it can add flexibility to the policy, enabling policyholders to adjust their coverage to align with their changing needs and goals. This includes creating capacity to add more permanent whole life coverage beyond what was initially purchased.

By using this framework, you can collaborate with clients to make decisions that go beyond the core benefits of whole life insurance. This approach opens a conversation about the various customization options that whole life insurance can offer to align the policy with the individual client’s needs and financial goals. As a result, what might seem like a complex decision becomes a clear, guided process.

Leveraging the power of customization

Whole life insurance, known for its guaranteed death benefits, cash value growth and fixed premiums, provides a sturdy foundation. Yet the true potential is in the customization options available through optional riders. The key is to build a client’s financial future on the guarantees and leverage the flexibility of the non-guaranteed elements to tailor coverage to specific needs and circumstances.

Consider a client scenario in the context of “goal aligners.” Suppose a client has embarked on a high-intensity career path — perhaps in sales. They plan to go full throttle for the next 10 to 15 years, fully aware that sustaining this pace for 30 years could lead to burnout. Their strategy includes a peak earnings period, during which they intend to overfund their insurance. However, they also foresee a career transition, during which they will shift gears rather than maintain that breakneck speed for the next two to three decades.

In such cases, the goal isn’t always to align the coverage with a retirement date. Instead, it’s about understanding your clients’ premium goals and time horizons and aligning the policy design as closely as possible with those horizons. This could mean, for instance, explaining a policy this way: “By using riders, I’ve customized your policy design to plan for intentionally higher premiums during your peak earning years, with a target of reduced premium requirements as you get closer to retirement and no planned premiums after retirement.”

Clarifying complexity to deliver value

As our world accelerates, automates and streamlines, it’s tempting to simplify products to keep pace. Yet the value of an insurance company and the financial professionals it partners with lies in the ability to clarify complexities, not eliminate them.

Clearly communicating concepts to the client shouldn’t come at the expense of flexibility and potential for personalization. It’s essential not to lose sight of the true objective: to offer nuanced, adaptable solutions that cater to the diverse needs of clients.

To learn more about the power and adaptability of OneAmerica’s whole life products, go here.

OneAmerica® is the marketing name for the companies of OneAmerica. Riders may be optional and carry an additional cost. The long-term advantage of a rider will vary with the terms of the benefit and the length of time the product is owned. As a result, in some circumstances, the cost of a rider may exceed the actual benefit paid under that rider. Guarantees are subject to the claims paying ability of the issuing insurance company.

Medication Therapy Management: A Part D Plan Program to Benefit Your Clients

Pioneering a tech-driven future for life insurance

Advisor News

- DC plan sponsors see opportunity in alternatives

- The American Dream: Redefined as financial stability

- Partial annuitization: How advisors can help clients balance income, growth

- Guide women along the walk through widowhood

- Dutch gambling tax hike falls short as prediction markets eye World Cup

More Advisor NewsAnnuity News

- KBRA Assigns Rating to TruSpire Retirement Insurance Company

- Partial annuitization: How advisors can help clients balance income, growth

- Guide women along the walk through widowhood

- Regulators clear way to rewrite annuity illustration rules

- Diversification’s growing importance in retirement planning

More Annuity NewsHealth/Employee Benefits News

- ARE SURVIVAL RATES FOR ADULTS WITH CONGENITAL HEART DISEASE LINKED TO SPECIALIZED CARDIAC CARE ACCESS?

- THIRTY-TWO YEARS, ZERO RESULTS: NRSC CHARGES SHERROD BROWN SOLD OUT TO BIG INSURANCE

- Employers weigh retention, costs in developing benefits strategies

- As beer strike continues, community stands behind workers

- Researchers at RTI International Report New Data on Managed Care (Tobacco Cessation Treatment in Pregnancy: Insights from Florida Medicaid Claims Data): Managed Care

More Health/Employee Benefits NewsLife Insurance News

- Trust, technology and the future of claims

- New York Life Launches an Indemnity Benefit for its Asset Flex Long-Term Care Insurance Solution

- AM Best Affirms Credit Ratings of DB Insurance Co., Ltd.

- AM Best Upgrades Credit Ratings of The People’s Insurance Company of China (Hong Kong), Limited

- SWBC’s Joan Cleveland Reappointed to Texas Association of Life & Health Insurers (TALHI) Board of Directors

More Life Insurance News