Military Officers Association: How to Make the Most Out of Your Thrift Savings Plan

The Thrift Savings Plan has always been a valuable benefit for the military, and recent changes make this low-cost and tax-advantaged account even more attractive. Servicemembers in the Blended Retirement System (BRS) can receive matching contributions from the government. New withdrawal rules give retirees more flexibility to access TSP money. And many people still haven't taken advantage of the Roth TSP, which grows tax-free for retirement.

"The TSP for the military is the first and best option to save for retirement," said

Those automatic contributions can become even more valuable during a time of market volatility, such as the coronavirus pandemic. By contributing a fixed dollar amount from each paycheck, you avoid trying to time the market; plus, you'll buy more shares when the price is down.

"This is a historic opportunity to build wealth," said Lt. Col.

Meanwhile, older people need to assess their TSP investments to make sure their allocations still match their timeframe and risk tolerance. Whether you're new to the military, have been serving for years, or have retired and plan to start taking withdrawals soon, it's important to review your TSP account and make the most of the new rules and strategies.

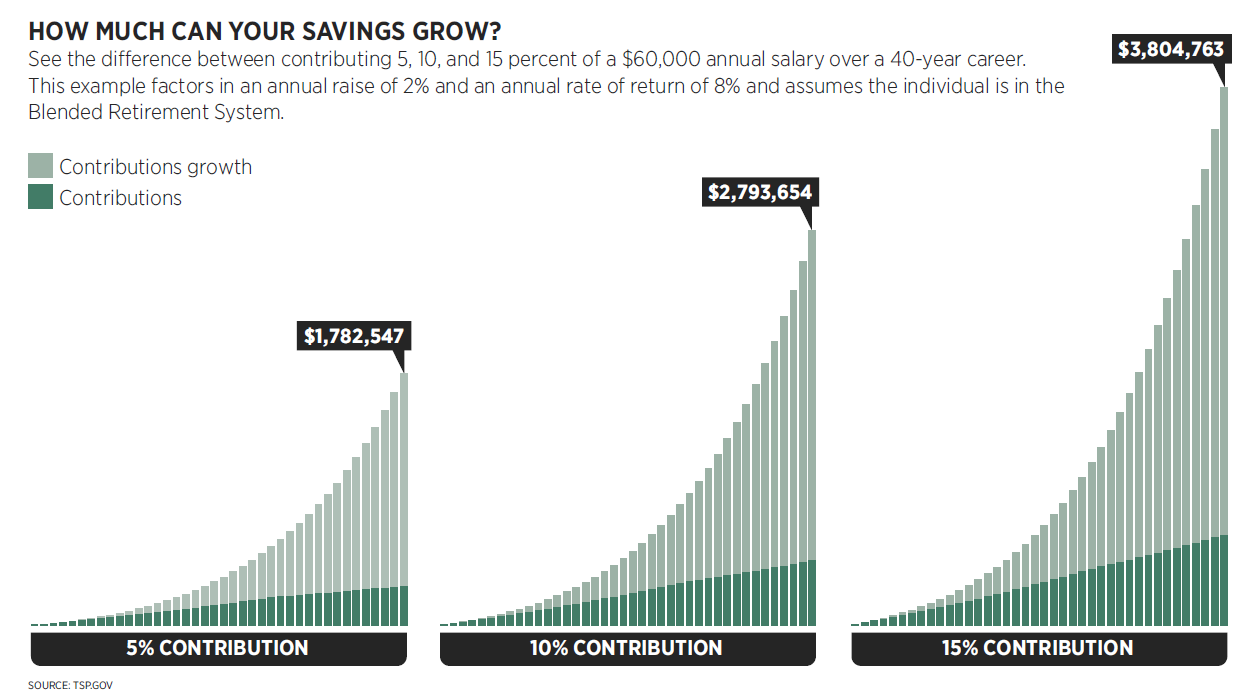

Click here to open the graphs in a new window (https://www.moaa.org/uploadedfiles/tsp-graphic-2021-internal.png).

{kind=link}

New Benefits for Contributing to the TSP

You can contribute up to

"If you're looking for a place to start, the absolute minimum would be to contribute 5% of your income if you're in the Blended Retirement System, or else you're leaving money on the table," said Col.

If you were automatically enrolled in the TSP in 2018 or later, then 3% of your basic pay is contributed to the TSP. You'll need to increase your contributions to 5% in your MyPay account to get the full match. Auto-enroll contributions increased to 5% for new participants starting on

The TSP is valuable even if you're in the legacy retirement system and don't receive a match. If you stay in the military for 20 years, your pension is based on 50% of your basic pay, not counting your housing allowance (40% of your basic pay under the BRS). If you don't stay for 20 years, you won't get a pension under either retirement system, so you'll have to rely on your retirement savings. Either way, add to your account whenever you can.

"If you get a promotion, pay yourself first and bump up your contribution rate," said Cmdr.

The contribution limits rise when you receive tax-exempt income in a combat zone --

Roth or Traditional Contributions?

Traditional TSP contributions are pre-tax, grow tax-deferred, and are taxable when withdrawn. Roth TSP contributions don't reduce your taxable income, but withdrawals are totally tax-free in retirement.

The Roth is better if you think you'll be in a higher tax bracket in retirement, which often happens when you aren't receiving a tax-free housing allowance and other benefi ts (also, recent tax cuts are scheduled to expire after 2025).

"If you're a junior officer, especially if you have a family, you are probably in the lowest tax bracket that you'll see throughout your life," said Quintiliani.

A Roth TSP also diversifies the tax situation of your retirement income. Pensions and traditional TSPs, 401(k)s, and IRAs are taxable when paid out. The Roth TSP gives you a bucket of tax-free money to tap in retirement.

"One thing I hear from people who are retired is that they wish they would have had an opportunity to put more money in a tax-free account because now everything they're getting is taxable," said Ostrom.

Investing Strategies

The TSP is known for its low fees and simple investing options. You can choose from five index funds -- investing in large companies (

"The younger you are, the more C, S, and I you should own. In your 20s, it should virtually all be stock. As you age, you can slowly add in more stable F and G," said Lt. Col.

Instead of making these choices yourself, you can invest in the L fund, a target-date fund that creates a diversified portfolio of the other funds based on your investing timeframe. You choose the date closest to when you plan to withdraw the money, and the fund gradually shifts to more conservative investments through time.

The L fund can also help you avoid panicking and selling at the wrong time in a volatile market.

"If someone is tempted during volatile times to make adjustments and make emotional decisions, then they really need to take a deep breath and think of their long-term goals," said Capt.

The L fund tends to be more conservative than other target-date funds. Beagle often recommends choosing a later target date to keep more money in stock funds for longer.

New Withdrawal Options

In the past, you could only take one partial withdrawal from the TSP, and then you either had to withdraw the remaining balance in a lump sum, convert it to a life annuity, or sign up for monthly payouts that could only change once per year. But new rules made TSP withdrawals much more flexible, like 401(k)s: You can now take withdrawals whenever you'd like, or you can set up and change installment payouts at any time.

There's now less of a reason to roll your TSP into an IRA when you leave the military. In fact, Ostrom often recommends rolling over money from other employers' 401(k)s into the TSP after you leave those jobs.

"The TSP is a bit unique by allowing you to move money into it after you're no longer employed there," said Ostrom. "You get the cost savings, you have the simplicity, and you're familiar with the plan."

Although you can choose between your Roth and traditional account, you can't specify which TSP investments to tap for withdrawals -- the money is taken pro rata from each of your investments. You can roll over your TSP to an IRA at that point and control which investments to tap, said Dorsett.

Sonoma County property owners rush to transfer inheritance ahead of new Prop.19 rules, higher taxes

Nev. A.G. Ford Joins Fight to Pause Deportations Pending Review of Policies by Biden-Harris Administration

Advisor News

- SEC: Get-rich-quick influencer Tai Lopez was running a Ponzi scam

- Companies take greater interest in employee financial wellness

- Tax refund won’t do what fed says it will

- Amazon Go validates a warning to advisors

- Principal builds momentum for 2026 after a strong Q4

More Advisor NewsAnnuity News

- Continental General Acquires Block of Life Insurance, Annuity and Health Policies from State Guaranty Associations

- Lincoln reports strong life/annuity sales, executes with ‘discipline and focus’

- LIMRA launches the Lifetime Income Initiative

- 2025 annuity sales creep closer to $500 billion, LIMRA reports

- AM Best Affirms Credit Ratings of Reinsurance Group of America, Incorporated and Subsidiaries

More Annuity NewsHealth/Employee Benefits News

- Gov. Lamont proposes 'Connecticut Option' to help small businesses afford health insurance

- Thousands in SLO County could lose Calfresh, Medi-Cal with ‘Big Beautiful Bill’

- Idaho lawmaker wants to limit the cost of certain anticancer drugs. What to know

- CQMC UPDATES CORE MEASURE SETS TO STRENGTHEN FOCUS ON HEALTH OUTCOMES AND REDUCE BURDEN

- Fewer Kentuckians covered by Kynect plans

More Health/Employee Benefits NewsLife Insurance News