Annuity Rebound Is Coming, Secure Retirement Institute Says

The Secure Retirement Institute is forecasting all individual annuity product lines except traditional variable annuities and fixed-rate deferred annuities to rebound in 2021.

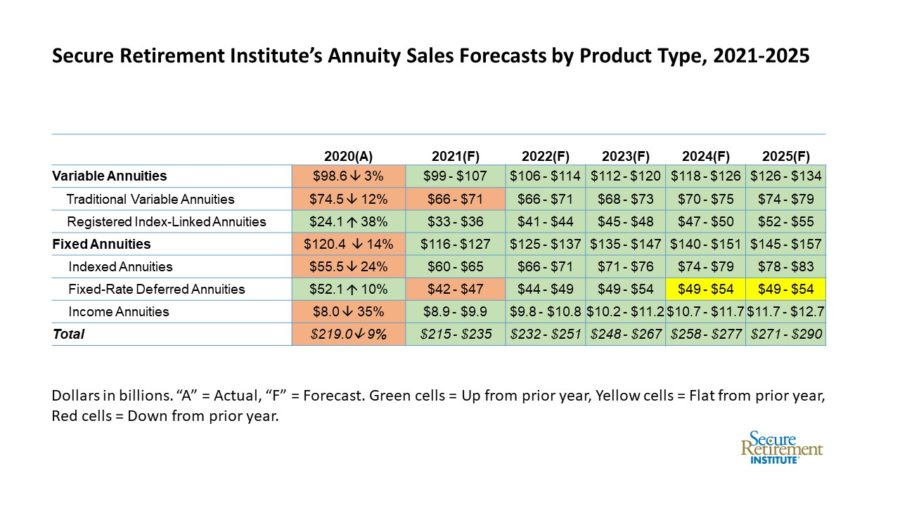

Overall individual annuity sales could see a slight increase in 2021, as the U.S. and the insurance industry slowly transition from the global pandemic. Longer term, SRI expects the total annuity market to benefit from improving economic conditions, shifts in demographic, as well as technology implementations. By 2025, SRI is forecasting the annuity market to grow as much as 30%.

There are several factors that will likely drive the annuity market:

• While economic conditions are forecasted to improve, historic low interest rates will continue to be a headwind.

• Products with protection features will continue to be in high demand.

• Demand for guaranteed income is expected to grow.

“The most significant factors that drive annuity sales are the economic and regulatory environment,” noted Todd Giesing, assistant vice president of SRI Annuity Research. “How, and how quickly, manufacturers and distributors respond to external factors will dictate the ultimate impact of these changes. The rate of change and adoption of solutions to the challenges created by the 2020 global pandemic were accelerated, as companies looked for ways to adapt and show resilience amidst massive disruption.”

A Look Individual Products:

Traditional Variable Annuities (VA): SRI is projecting traditional VA sales to decline slightly in 2021. By 2022, traditional VA sales will flatten out as economic conditions improve. Slow growth will come back to the traditional VA market in 2023 through 2025. Improving interest rates will help carriers with pricing efficiencies in products with guaranteed living benefits, and smooth equity markets will aid in the slow growth of investment-focused traditional variable annuities.

Registered Index-Linked Annuities (RILA): The RILA market has experienced remarkable growth over the past few years and this trend is expected to continue through 2025. New manufacturers continue to enter the market and SRI expects some to introduce guaranteed lifetime benefits riders to broaden the appeal of these products to investors. By 2025, RILA sales are expected to be double what they are today.

Fixed Indexed Annuities (FIA): The indexed annuity market faced an extremely challenging environment in 2020, and as a result saw sales decrease by nearly $20 billion in 2020. Looking ahead, as interest rates improve, indexed annuities should slowly return to growth mode in 2021, but will face challenges as RILA’s continued success will likely take a portion of flows away from FIA sales, particularly in the independent BD and bank channel. SRI does expect FIA sales to enjoy slow and steady growth through 2025, and to reach or exceed 2019 record sales levels.

Fixed-Rate Deferred Annuities (FRD): Record market volatility and highly competitive crediting rates drove 2020 FRD sales to their highest annual level since 2009, as consumers sought investment protection and guaranteed growth. Despite improving interest rates and market stability — which would normally drive investors toward other products with greater growth potential — FRD sales will be bolstered by the nearly $150 billion invested in short-term fixed-rate deferred products over the past three years that will be coming out of their surrender periods. Given the current market conditions, we expect many investors will likely reinvest in fixed-rate deferred annuity products due to the rising rates, driving sales to close to $50 billion over the next few years.

Income Annuities: Despite improving economic conditions, low interest rates will continue to challenge the value proposition of income annuities through 2025. In addition, more flexible income solutions, such as guaranteed living benefits, will continue to capture a majority of the flows for investors seeking income guarantees in their retirement portfolio. While the growing aging population will benefit these products, the challenges of limited liquidity and the inability for insurers to provide robust pricing to attract individuals to income annuities will limit income annuity sales growth.

Fla. Division of Emergency Management: Critical Investments in Preparedness Support Florida Disaster Response

Guidehouse Designates US Markets Ripe for “Payvider” Adoption and Growth

Advisor News

- Nearly half of nonretirees doubt they will fully retire

- How much could failure to fund Social Security cost average Americans?

- How can more Americans achieve financial independence?

- Savers vs. spenders: How money management attitudes impact financial confidence

- Demonstrating the value of life insurance to Gen Z

More Advisor NewsHealth/Employee Benefits News

- Insurers propose premium increases for ACA customers in Iowa

- How Does New CareScout Long-Term Care Insurance Policy Compare In Cost

- They harvest the nation’s food, but a new rule may strip them of health insurance

- A new option for long-term care costs

- Rising health insurance exchange costs are bad news for Mississippi's working poor

More Health/Employee Benefits NewsLife Insurance News

- AM Best Comments on Credit Ratings of Horace Mann Educators Corporation and Its Subsidiaries Following Announced Transaction with Medical Mutual of Ohio

- AM Best Affirms Credit Ratings of Hanwha General Insurance Company Limited

- Globe Life boosts Q2 earnings, eyes AI shift for long-term growth

- ATTORNEY GENERAL BRENNA BIRD LEADS FIGHT TO PROTECT IOWA PENSIONS

- AM Best Affirms Credit Ratings of Bao Viet Insurance Corporation

More Life Insurance NewsProperty and Casualty News

- 4 Myths about Insurance in California

- Connecticut Attorneys Title Insurance Company Trademark Application for “CATIC ACADEMY” Filed: Connecticut Attorneys Title Insurance Company

- Florida Democrats Annette Taddeo and Earle Ford compete to face CFO Blaise Ingoglia in November

- NEW MERKLEY BILL TACKLES DUAL CRISES OF WILDFIRE RISK AND INSURANCE AFFORDABILITY

- Researchers’ Work from California Institute of Technology (Caltech) Focuses on Economics (Competing Under Information Heterogeneity: Evidence From Auto Insurance): Economics

More Property and Casualty News