Why financial professionals should enter the 403(b) K-12 educator market

The K-12 educator market, representing less than 10% of 403(b) plan participants, represents a largely untapped opportunity for financial professionals.

Teachers, administrators and other staff in the public school system face a complex set of retirement planning challenges. Therefore, they need professional guidance to navigate their options. However, some financial professionals avoid this space due to misconceptions and criticisms.

Before diving into the criticisms about how this market works and examining the opportunities for financial professionals, it’s important we understand the trends over the past several decades that have made 403(b) plans attractive and necessary in the K-12 public school system, as well as the unique retirement planning needs of educators.

Understanding the 403(b) K-12 educator market

In the K-12 public school system, the 403(b) plan is meant to supplement the pension system, which has been the cornerstone of most educators’ retirement income since it was first established in 1958. However, the shift from defined benefit to defined contribution plans in recent years has resulted in a changing of the guard, so to speak, with more responsibility for retirement savings shifting to educators due to pensions becoming underfunded.

Two primary trends impacting pension liability are demographics and the state of funding obligations. In terms of demographics, there are more educators retiring and drawing pension benefits than there are educators entering the profession and helping fund the pensions during their working years. Moreover, 55% of educators say they are thinking about leaving the profession earlier than planned, according to a National Education Association member survey. This could result in fewer teachers staying in the profession long enough to become eligible for a pension. From a pension obligations standpoint, states have been challenged by rising obligations due to the demographic shifts widening the gap in funding liabilities.

Given a significant number of teachers leaving the profession before becoming eligible for their pension, 403(b) plans can play a crucial role in helping close the income gap for educators in retirement. In addition, the side effect of comprehensive retirement benefits for educators is improved fiscal health, which can directly impact both physical and mental health. This leads to better employee satisfaction and productivity and retention of talent.

Educators’ unique retirement planning needs

Educators have unique retirement planning needs that financial professionals entering this market must understand. Most school districts today annualize their salaries for educators, which leads to a consistent pay schedule throughout the year, including the summer months. Yet due to the nature of their daily schedule, educators rarely have breaks throughout the day to consider or plan for their future.

Educators’ time is in constant demand by students, peers, administrators and parents. This means that financial professionals who enter this space must be flexible and strategic about how they engage with educators.

For some financial professionals, this might mean coming into a classroom to meet with a client during their free or flex period during the school day instead of expecting the client to meet with them at their office. It could also mean hosting an information session at the school prior to the start of the school day or in the evenings.

Opportunities for financial professionals

The 403(b) K-12 educator market offers financial professionals a stable client base that is generally committed to long-term relationships, which aligns well with the financial planning process. Educators, regardless of salary, are also motivated to improve their financial security and are seeking clarity about their retirement options and how to manage their 403(b) accounts effectively.

Specifically, educators want help evaluating investment options and understanding tax considerations that could impact their finances when they reach retirement. Financial professionals who can help educators increase their financial literacy, assess the options available within their 403(b) plan and make informed choices are highly valuable. Advisors in this market can create a loyal, stable customer base with new and emerging household financial planning needs over the course of their lives.

With 403(b) plan participation rates for school districts ranging from less than 7.53% to more than 75.69%, according to the National Tax-Deferred Savings Association, the opportunity for financial professionals to add value and change educators’ lives is significant.

Understanding school districts’ goals and objectives when it comes to their employee benefits, having a strong comprehension of teacher retirement systems, and designing a personalized plan for each educator are keys to having a successful career supporting educators with their retirement options.

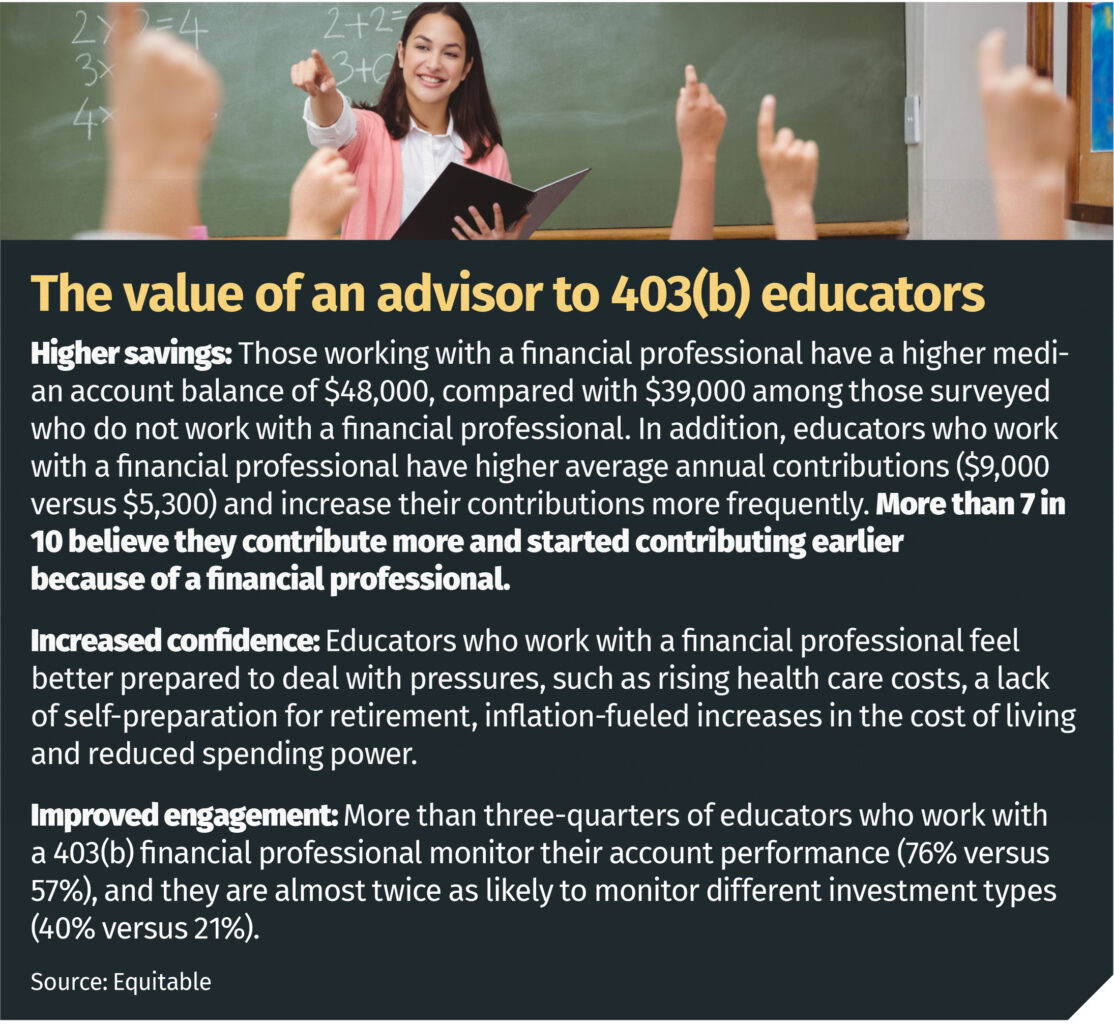

Research also shows that educators in 403(b) plans who work with a financial professional have better retirement outcomes. According to an Equitable survey of 1,001 K-12 educators, those who used a 403(b) financial professional had an average annual contribution of $9,000, as opposed to an annual contribution of $5,300 for employees who elected to not work with a financial professional. In addition, the survey found K-12 educators who work with a financial professional were likely to have a higher median retirement account balance of $48,000 compared to $39,000 for those who do not work with one.

Addressing criticisms of how the 403(b) K-12 market works

Despite the growth potential in this market, some persistent criticisms often discourage financial professionals from entering this market.

Criticism: Financial professionals are taking advantage of educators with excessive fees.

Critics of annuities argue these products have high fees and are overrecommended. Like in any industry, there are always bad actors, but the reality is that most financial professionals are reputable, transparent and focused on the financial security of their clients. And while 403(b) plans are not subject to the Employee Retirement Income Security Act, financial professionals are still subject to the Securities and Exchange Commission’s Regulation Best Interest, which is enforced by the SEC and the Financial Industry Regulatory Authority and requires all retail securities recommendations to be in the client’s best interest.

Regarding their cost, annuities are long-term investments that offer a variety of benefits and guarantees based on the claims-paying ability of the issuing life insurance company. Annuities will have different fees than, for instance, a mutual fund, which does not offer such benefits or guarantees. Financial professionals who are transparent about fees can help educators make better-informed decisions about which products to choose and how to avoid unnecessary costs.

This is a market where the need for education is extremely high, so financial professionals must provide clarity on fees and help educators choose options that balance cost with value.

Criticism: School districts should limit provider choices.

Another frequent criticism of the 403(b) structure in K-12 districts is that the number of providers offered is too high. Some critics and adjacent industry experts suggest that limiting retirement plan providers can reduce decision fatigue.

A one-size-fits-all approach misses the mark and has proven to have a negative impact on participant outcomes. Participant choice in providers and financial professionals is key to ensuring that the best products and solutions are competing to drive the right outcomes for educators. 403(b) plans are often compared with their distant cousin, 401(k) plans, in the private sector. The reality is that they are more like payroll deductible individual retirement accounts. As one of the fastest-growing retirement asset vehicles, IRAs thrive because of their open market concept, where participants can choose the advisors, investments and providers they most like to work with.

Embracing the market

The 403(b) K-12 educator market is full of potential for financial professionals willing to approach it with integrity, transparency and a focus on service. Financial professionals should not shy away from questions their clients may have about these common criticisms. Instead, by addressing them when appropriate, providing ethical advice and helping educators navigate complex decisions, financial professionals can become a trusted part of educators’ financial journeys.

Embracing this market can help financial professionals tap into a valuable client base and play a pivotal role in helping America’s teachers secure their financial well-being so they can pursue long and fulfilling lives.

The silent threat of disability to ultrasuccessful clients

We need to up our game to reach Gen Z

Advisor News

- Embracing a family-centric approach to financial planning

- Family communication: Financial planning’s growing blind spot

- Americans aren’t turning retirement plans into action, LIMRA finds

- Ashley Hinson ‘death tax’ story collides with truth

- How advisors can prepare clients for an uncertain retirement landscape

More Advisor NewsAnnuity News

- Investigation finds deceptive sales, churning of annuities targeting postal workers

- Corebridge annuity sales slip ahead of Equitable marriage

- California teachers settle class-action lawsuit over in-plan annuity fees

- Jackson Financial CEO caps 40-year career with blockbuster Q2

- Lumos Insurance introduces the Immediate Care Plan to help families fund long-term care

More Annuity NewsHealth/Employee Benefits News

- Louisiana hospitals see sharp uptick in uninsured patients after Obamacare subsidies expired

- CareScout Redefines Worksite Long-Term Care Insurance With a Solution That Goes Further for Employers and Employees

- Next Generation My Care – It’s here … now what?

- 4 common LTC missteps older Americans must avoid

- Missouri and Kansas can expect double-digit Obamacare premium hikes again

More Health/Employee Benefits NewsLife Insurance News

- Built to Last: Winston-Salem—a quiet industrial powerhouse

- The silver economy ushers in a new era of life insurance growth

- Family communication: Financial planning’s growing blind spot

- Indiana eyes more oversight of insurance companies' exposure to private credit

- HEALEY-DRISCOLL ADMINISTRATION RETURNS $14.5 MILLION TO HEALTH AND DENTAL INSURANCE CONSUMERS AND BUSINESSES

More Life Insurance News