If You Want Younger Agents, You Need Younger Tools

By Sean A. Ruggiero

Let me introduce you to two agents, Tom and Austin.

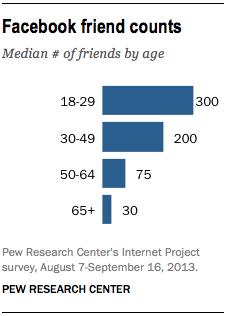

Tom is 56 years old and has been an insurance agent for six years following a career as a car salesman and serving in the military before that. Tom drives a Chrysler 300 and has a Nokia smartphone on which he has downloaded six apps. He occasionally uses Facebook, where he has 75 friends.

Austin is a brand new agent who is 27 years old. He has a college degree and he has never served in the military. He drives a BMW X3 and he owns the latest iPhone, on which he has downloaded 42 apps. He has 300 friends on Facebook, which he checks throughout the day.

When Tom started in the insurance industry, he was asked to write down the names of 200 friends and family members, and start calling them to buy insurance. Through sweat and perseverance, Tom was able to work through that process and survive his first year as an insurance agent. A large part of that success was credited to Tom, but a significant reason that Tom was able to succeed was the fact that he was calling other people who were 56, drove a Chrysler 300, and had 6 apps on their smartphone and 75 friends on Facebook.

When Austin started his insurance career, he was asked to do the same thing as Tom was asked to do when he started his. Unfortunately, Austin was not calling the same demographic that Tom was, so when he called his 200 names, he was met by voicemails, annoyance and confusion. See, Austin’s peers don’t communicate the way Tom’s peers do, so does Austin even have a chance at success when he is using the wrong tools to sell to his demographic?

The industry has been squawking a lot recently about “disrupting” the way we purchase insurance, and that millennials don’t want to use an agent. I believe that is only partially true. I believe that millennials don’t want to use Tom as their agent!

Unfortunately, there has been no adoption of modern sales and communication tools (such as the use of social media or inbound digital marketing) for the insurance industry because the average agent is Tom, not Austin, and modern marketing and communication methods have little effect for Tom. Let’s take a look at the reason why.

If Tom were to launch a social media marketing campaign, and create intriguing content that he posted to Facebook three times a week, he essentially would be marketing to 75 people who seldom use Facebook. Life insurance is sold when a “life event” occurs. A life event is something like a birth, death, marriage, mortgage, etc. When we are marketing on Facebook, we essentially are trying to intersect our messaging with a life event of a friend. Based on that logic, the more friends we have on Facebook (and the more active they are on Facebook), the better our chances of intersecting with a friend’s life event. So which agent has the better chance of success with social media marketing, Tom or Austin?

When we look at the probability of success mathematically, we can see that Austin has a 40 percent greater chance of success than Tom. The reality is that Austin’s chances are exponentially higher (or Tom’s chances are exponentially lower) because Austin’s 300 friends prefer to use Facebook and they are highly active on social media. In contrast, Tom’s 75 friends are not frequent users of Facebook and they are not active on social media.

If this is such an obvious conclusion, then why is the industry not providing, promoting and training new agents on these tools? Furthermore, why is the industry using Tom as the litmus test for social media and digital marketing effectiveness?

Insurance carriers, independent marketing agencies, brokerage general agencies and agents abroad must dedicate themselves to offering the next generation of agents these tools for selling life insurance. Furthermore, the industry must be patient in allowing these tools time to work and must promote these tools to attract new, younger agents into the industry. In order to do this, the social media and digital marketing tools adopted by the industry must be affordable and scalable. They cannot require large upfront costs and they can’t be complicated or intimidating to use.

If we were able to grab Austin’s iPhone, we would see a common denominator in the 42 apps he has downloaded; these 42 apps all would be simple to understand and to use. That is the same approach the industry must have when searching for tools to give their young agents.

We must seek out specific tools that are designed to help young life insurance agents accomplish social and digital sales, and they must be easy to use and affordable to operate. Only then can we attract the younger agents. Until we do that, we are headed for extinction and I personally don’t believe that is what is best for the industry or for the consumer, no matter what car they drive, how many apps they have on their phone or how often they use social media.

Sean A. Ruggiero, CEP, RICP, is founder and president of LifeDrip. Sean may be contacted at [email protected].

© Entire contents copyright 2016 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

Marketing To The Next Generations Is ‘A Whole New Ball Game’

Market Synergy Hammers DOL on Public Notice of Rule Changes

Advisor News

- Americans aren’t turning retirement plans into action, LIMRA finds

- Ashley Hinson ‘death tax’ story collides with truth

- How advisors can prepare clients for an uncertain retirement landscape

- Investors aren’t waiting out uncertainty

- Transamerica and Advo(k)ate Advisors launch pooled employer plan

More Advisor NewsAnnuity News

- Corebridge annuity sales slip ahead of Equitable marriage

- California teachers settle class-action lawsuit over in-plan annuity fees

- Jackson Financial CEO caps 40-year career with blockbuster Q2

- Lumos Insurance introduces the Immediate Care Plan to help families fund long-term care

- NAIC regulators begin consensus phase on annuity illustration overhaul

More Annuity NewsHealth/Employee Benefits News

- 3 summer sales habits that build next year’s pipeline

- ADMINISTRATION POLICIES GO BEYOND 2025 REPUBLICAN RECONCILIATION LAW, DEEPENING ITS HARM

- STATE LEGISLATIVE SESSIONS HIGHLIGHT CHOICE BETWEEN PROTECTING COVERAGE AND DEEPENING HARM AFTER FEDERAL MEDICAID CUTS

- ICYMI: WISCONSIN ATTORNEY GENERAL JOSH KAUL JOINS LAWSUIT CHALLENGING NEW FEDERAL RULE GOVERNING AFFORDABLE CARE ACT HEALTH PLANS FOR 2027

- Coverage for nonprofit staff in sight

More Health/Employee Benefits NewsLife Insurance News

- HEALEY-DRISCOLL ADMINISTRATION RETURNS $14.5 MILLION TO HEALTH AND DENTAL INSURANCE CONSUMERS AND BUSINESSES

- ‘Uniquely positioned’: Equitable outlines future post-Corebridge merger

- Don't keep checks with clerical errors

- The insurance distributor that builds its own software will win the next decade

- iA Financial Group Reports Second Quarter Results

More Life Insurance News