Study shows significant growth in 401(k) balances for younger workers who consistently participate

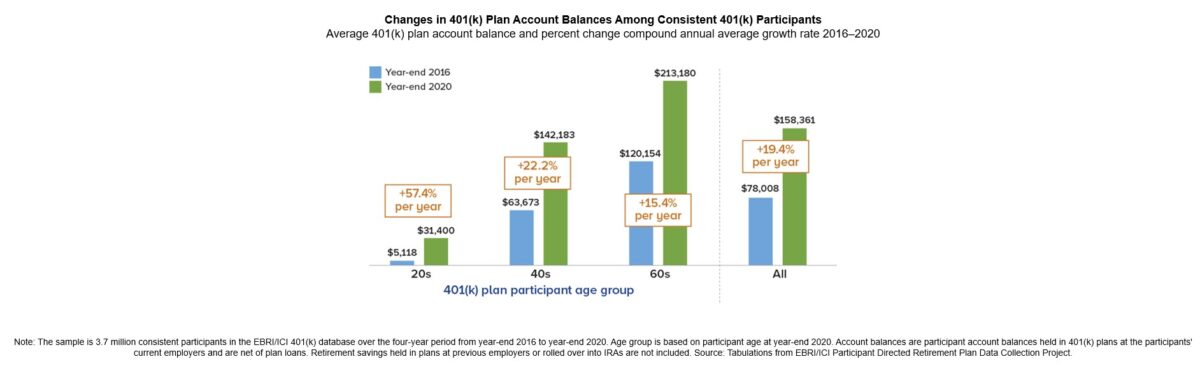

(Washington, D.C.) -- Account balances for consistent 401(k) plan participants rose from year-end 2016 through year-end 2020, according to a new study from the Employee Benefit Research Institute (EBRI) and the Investment Company Institute (ICI) titled “What Does Consistent Participation in 401(k) Plans Generate? Changes in 401(k) Plan Account Balances, 2016–2020.” The average 401(k) plan account balance for consistent participants rose each year from year-end 2016 through year-end 2020. Overall, increases reflect a compound annual average growth rate of 19.4 percent over the period, with the average account balance rising from $78,008 at year-end 2016 to $158,361 at year-end 2020.

Younger 401(k) participants, or those with smaller year-end 2016 balances, experienced higher growth in account balances compared with older participants, who tend to have larger balances on average. Three primary factors affect account balances: contributions by the participant, employer, or both; investment returns; and withdrawal and loan activity. The percent change in balance for participants in younger age groups was influenced by the relative size of their contributions to their account balances.

“Exploring the changes in account balances among consistent 401(k) plan participants highlights the strength of the 401(k) plan as a powerful savings tool,” said Sarah Holden, senior director, Retirement and Investor Research, ICI. “Younger 401(k) plan participants, whose relatively smaller initial account balances benefited from contributions as well as market returns, saw the highest growth rates over the period as their average 401(k) account balance rose 57.4 percent per year, on average, over the period.

Key findings in the report include:

- The median 401(k) plan account balance for consistent participants increased at a compound annual average growth rate of 28.3 percent over the period, to $62,134 at year-end 2020.

- Younger 401(k) participants or those with smaller year-end 2016 balances experienced higher percent growth in account balances compared with older participants or those with larger year-end 2016 balances. Because younger participants’ account balances tended to be smaller, their contributions produced significant percentage growth in their account balances.

- 401(k) participants tend to concentrate their accounts in equity securities. On average at year-end 2020, more than two-thirds of consistent 401(k) participants’ assets were invested in equities—through equity funds, the equity portion of target date funds, the equity portion of non–target date balanced funds, or company stock. Younger 401(k) participants tend to have higher concentrations in equities than older 401(k) participants.

“Younger 401(k) plan participants tended to be more invested in equity funds and target date funds while older participants were more likely to invest in fixed-income securities,” said Craig Copeland, director, Wealth Benefits Research, EBRI. “At year-end 2020, 401(k) plan participants in their twenties had allocated 86 percent of their plan account balances to equities while participants in their sixties had allocated 57 percent to equities.”

The study is based on the EBRI/ICI database of employer-sponsored 401(k) plans, compiled through a collaborative research project undertaken by the two organizations since 1996. The project is unique because it includes data provided by a wide variety of plan recordkeepers and, therefore, represents the activity of participants in 401(k) plans of varying sizes—from very large corporations to small businesses—with a variety of investment options. This longitudinal analysis tracks the account balances of 3.7 million 401(k) plan participants who had accounts in the year-end 2016 EBRI/ICI 401(k) database and each subsequent year through year-end 2020 (a four-year period).

Complete results of the annual EBRI/ICI 401(k) database update are posted on each organization’s website at www.ebri.org and www.ici.org/system/files/2023-03/per29-02.pdf.

Private equity insurance investors facing higher capital charges for CLOs

How a defined process eases client concerns

Annuity News

- Jackson CEO Laura Prieskorn to retire at the end of 2026

- Has your annuity been reinsured in the Cayman Islands? Here’s why it matters

- DOL slams pension risk transfer lawsuit as ‘opportunistic’ litigation

- AM Best Affirms Credit Ratings of New York Life Insurance Company and Its Subsidiaries

- Advisors don’t have an annuity problem; they have an integration problem.

More Annuity NewsHealth/Employee Benefits News

- Rising health insurance exchange costs are bad news for Mississippi's working poor

- Iowa health insurers propose premium increases for ACA customers

- IOWANS ARE HOLDING ASHLEY HINSON ACCOUNTABLE FOR RAISING THEIR HEALTH INSURANCE PREMIUMS

- RECAP: IOWANS CALL OUT ASHLEY HINSON FOR SENDING HEALTH INSURANCE PREMIUMS SKYROCKETING AND CLOSING HEALTHCARE CLINICS

- New dashboard tracks Kansas Affordable Care Act enrollment by legislative district, county

More Health/Employee Benefits NewsLife Insurance News

- AM Best Comments on Credit Ratings of Horace Mann Educators Corporation and Its Subsidiaries Following Announced Transaction with Medical Mutual of Ohio

- AM Best Affirms Credit Ratings of Hanwha General Insurance Company Limited

- Globe Life boosts Q2 earnings, eyes AI shift for long-term growth

- ATTORNEY GENERAL BRENNA BIRD LEADS FIGHT TO PROTECT IOWA PENSIONS

- AM Best Affirms Credit Ratings of Bao Viet Insurance Corporation

More Life Insurance NewsProperty and Casualty News

- Connecticut Attorneys Title Insurance Company Trademark Application for “CATIC ACADEMY” Filed: Connecticut Attorneys Title Insurance Company

- Florida Democrats Annette Taddeo and Earle Ford compete to face CFO Blaise Ingoglia in November

- NEW MERKLEY BILL TACKLES DUAL CRISES OF WILDFIRE RISK AND INSURANCE AFFORDABILITY

- Researchers’ Work from California Institute of Technology (Caltech) Focuses on Economics (Competing Under Information Heterogeneity: Evidence From Auto Insurance): Economics

- Insurance companies might have to start warning homeowners about cancellation

More Property and Casualty News