The structural rise of structured products

Structured credit has shifted over the past decade from a niche allocation to a core component of fixed-income portfolios for both insurers and mutual fund managers. National Association of Insurance Commissioners Schedule D data and quarterly Securities and Exchange Commission filings point to steady, compounding growth in exposure. This growth is driven by relative-value advantages, risk-based capital efficiency and growing demand for stable, cash-flow-generating assets.

Insurer allocations: From modest to meaningful

For insurers, the shift has been both steady and substantial. Structured product holdings increased from $884 billion in 2014 to $1.44 trillion in 2024, raising their share of total bond portfolios from 22.9% to 26.5%. Growth was led by ABS and “Other Structured” categories, which more than doubled from $261 billion to $700 billion over the period. RMBS and CMBS exposures remained comparatively stable but benefited from the revival of the RMBS 2.0 market and the introduction of new collateral types, such as Non-Qualified Mortgage and Second Liens. Since 2021, insurers have increasingly relied on structured products to enhance yield and capital efficiency amid corporate spread compression and greater capital sensitivity, as we illustrate in Figure 1.

The resulting reallocation has been toward senior, cashflow stable structured deals that provide higher spread per unit of capital charge – a critical metric for insurers seeking to meet liabilities efficiently, particularly with multiyear guaranteed annuities.

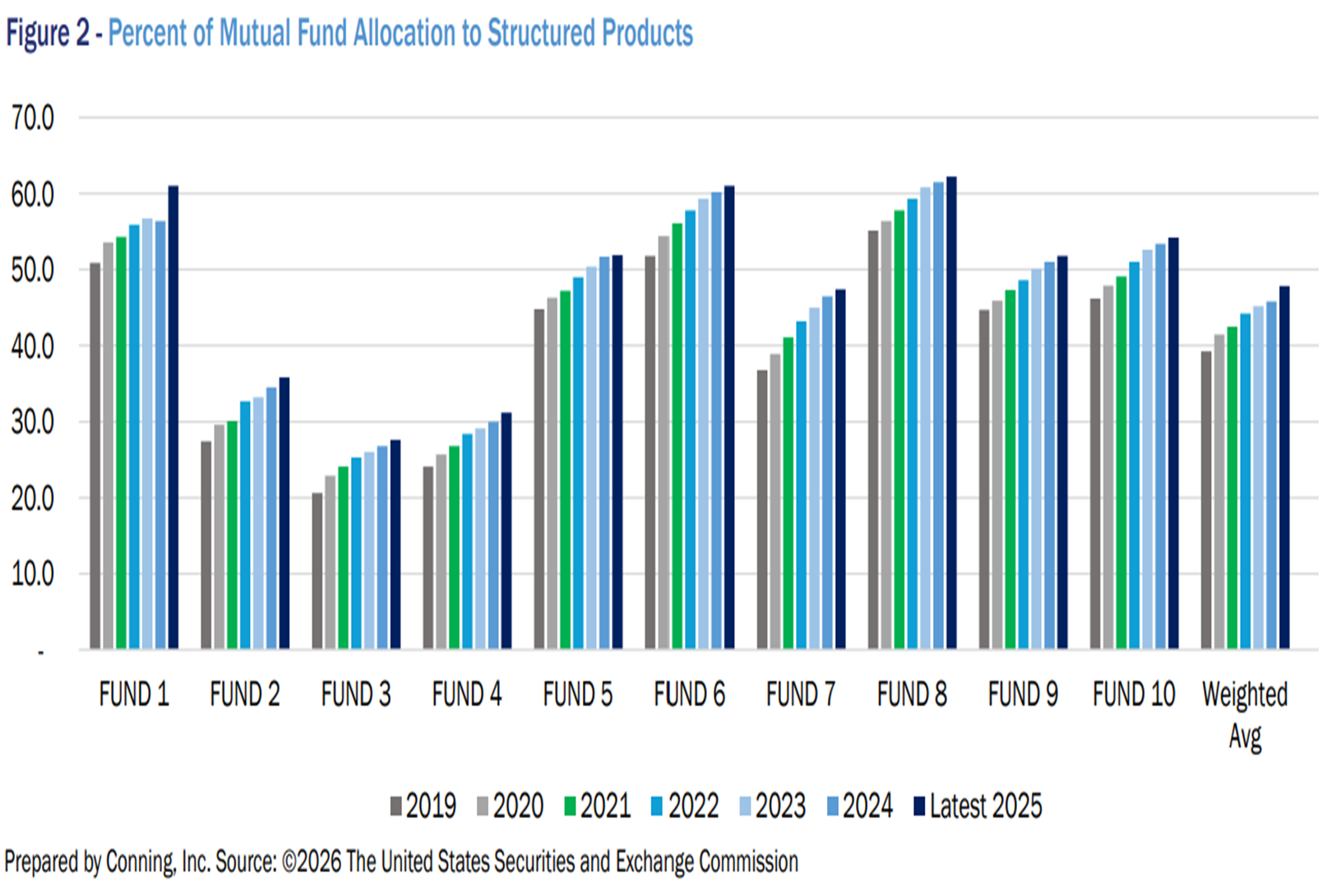

Mutual funds: Active managers embrace structured

In parallel, the 10 largest active fixed-income funds, representing more than $660 billion in assets under management, have steadily increased their structured product exposure over the last six years, illustrated in Figure 2. On a weighted-average basis, allocations to structured products (agency and non-agency MBS, ABS, CMOs and CLOs) rose from 39.3% in 2019 to 47.9% in 2025, a gain of nearly 9 percentage points. This shift reflects more than $55 billion of reallocation away from traditional areas of the fixed-income market.

Portfolios once dominated by corporates now commonly allocate more than one-third of their investments to structured sectors. Managers have been drawn to the incremental spread advantage relative to investment-grade corporates of similar duration and quality, as well as the flexibility offered by diverse collateral types across consumer, commercial, equipment and real estate markets. This breadth supports more precise duration and risk positioning.

Demographics and income demand

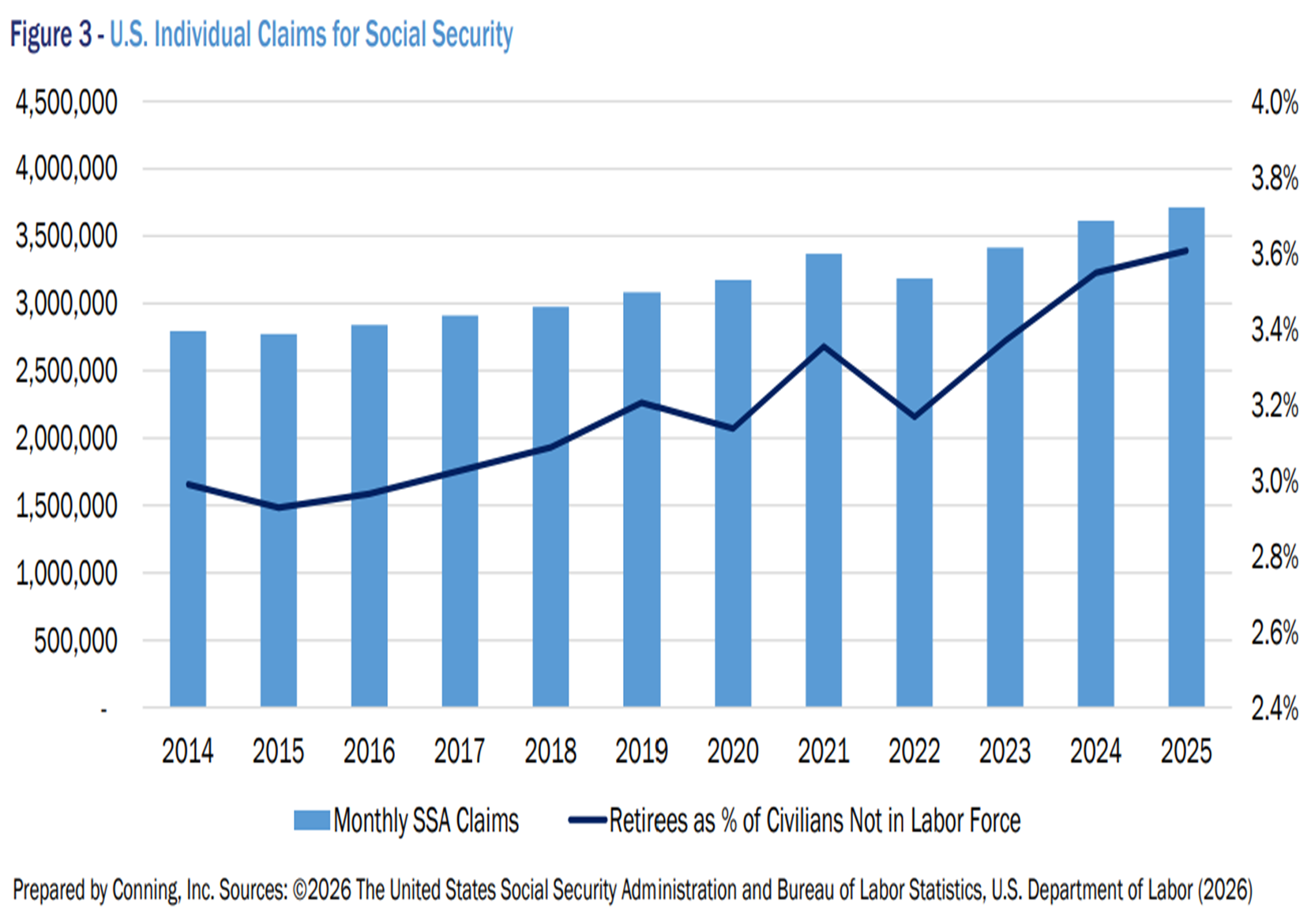

Demographic shifts are reinforcing the move toward income-oriented strategies. Since 2020, the share of retirees in the U.S. non-labor force population has increased from 3% to 3.6% and monthly Social Security claims have risen by nearly one million individuals since 2014, illustrated in Figure 3. As a growing portion of the population transitions to retirement, both money managers and insurers have seen increased inflows into fixed income funds and MYGA products, reflecting stronger demand for predictable, cash-flow producing assets.

Structured credit, particularly senior tranches of Esoteric ABS, RMBS, CMBS and CLOs, have emerged as an attractive alternative to traditional fixed income sectors for generating higher income and yields to offset liabilities. These sectors offer:

- Predictable amortization schedules that align well with liability-driven portfolios.

- High levels of credit enhancement and historically low default rates, particularly in seasoned collateral pools.

- Compelling relative value compared to investment-grade corporates of similar duration and quality.

In this environment, both insurers and mutual fund complexes are increasingly converging toward the same solution: structured products as core portfolio anchors for a generation seeking income and downside resilience.

Viewed across both insurers and mutual funds, structured products are no longer peripheral building blocks; they have become foundational. The sustained rise in allocations over the past decade reflects a deliberate shift in fixed-income portfolio construction rather than a temporary search for relative value. With a growing share of baby boomers entering retirement and increasing demand for stable income solutions, this trend is likely to persist. Structured products now sit at the intersection of income generation and capital efficiency, and they will continue to play a central role for investment managers navigating today’s fixed-income landscape.

© Entire contents copyright 2026 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

Invigorating client relationships with AI coaching

Metlife study finds less than half of US workforce holistically healthy

Advisor News

- Nearly half of nonretirees doubt they will fully retire

- How much could failure to fund Social Security cost average Americans?

- How can more Americans achieve financial independence?

- Savers vs. spenders: How money management attitudes impact financial confidence

- Demonstrating the value of life insurance to Gen Z

More Advisor NewsAnnuity News

- Advisors don’t have an annuity problem; they have an integration problem.

- Agentic AI is transforming insurance sales both for consumers and agents

- Canvas steps into the direct-to-consumer market that has yet to take off

- The next growth phase in life/annuities depends on modernization

- CA judge certifies class action in teachers’ lawsuit over in-plan annuity fees

More Annuity NewsHealth/Employee Benefits News

- Insurers hedge on Trump-backed pledge to improve denials process

- Tips for life, health insurance for military members, families

- Health insurers use a whole arsenal of tools to deny care, increase profit

- Health insurers use a whole arsenal of tools to deny care, increase profit

- Covered California rates to jump nearly 10% as thousands struggle to afford coverage

More Health/Employee Benefits NewsProperty and Casualty News

- New ReSource Pro Primary Research Reveals Five Critical Lessons from Across the Insurance Industry

- Giannoulias Marks Major Victory for Illinois Drivers Facing Skyrocketing Costs with Landmark Auto Insurance Reform

- GOVERNOR HOCHUL ANNOUNCES HUNDREDS OF LAW ENFORCEMENT OFFICIALS SUCCESSFULLY COMPLETED SPECIALIZED AUTO INSURANCE FRAUD TRAINING IN ALBANY

- AM Best Affirms Credit Ratings of The Hartford Insurance Group, Inc. and Its Subsidiaries

- Opinion: We must clear the insurance industry’s name

More Property and Casualty News