Most long-term care doesn’t qualify for insurance benefit

The U.S. Department of Health and Human Services’ latest report on long-term care projected a lower likelihood of requiring LTC and highlighted a new issue for financial professionals: The majority of LTC may be needed by clients who have lower levels of disability that do not meet the criteria for an LTC insurance benefit. The report’s authors concluded that better financial planning is needed to deal with the costs of LTC across the entire spectrum of disability at older ages.

LTC estimates were based on a microsimulation model that estimated the likelihood and duration of LTC for individuals (not couples, as explained further) who turned 65 today. The benchmark in the study, as with prior government studies that modeled LTC risk, was significant disability that required care at “the threshold for benefits under a tax-qualified long-term care insurance policy as specified by the Health Insurance Portability and Accountability Act (HIPAA)” of 1996. This advanced level of disability is what financial professionals target when they discuss LTC with clients. LTC at earlier levels of disability is not usually included in planning strategies.

Estimates for significant disability at the HIPAA threshold were as follows.

» Forty-nine percent of men and 64% of women turning 65 today will require long-term care.

» For all 65-year-olds combined, including those who will and will not need LTC, the duration of LTC will average 3.1 years.

» If projections included only people who will need LTC, the duration of LTC will average 5.4 years.

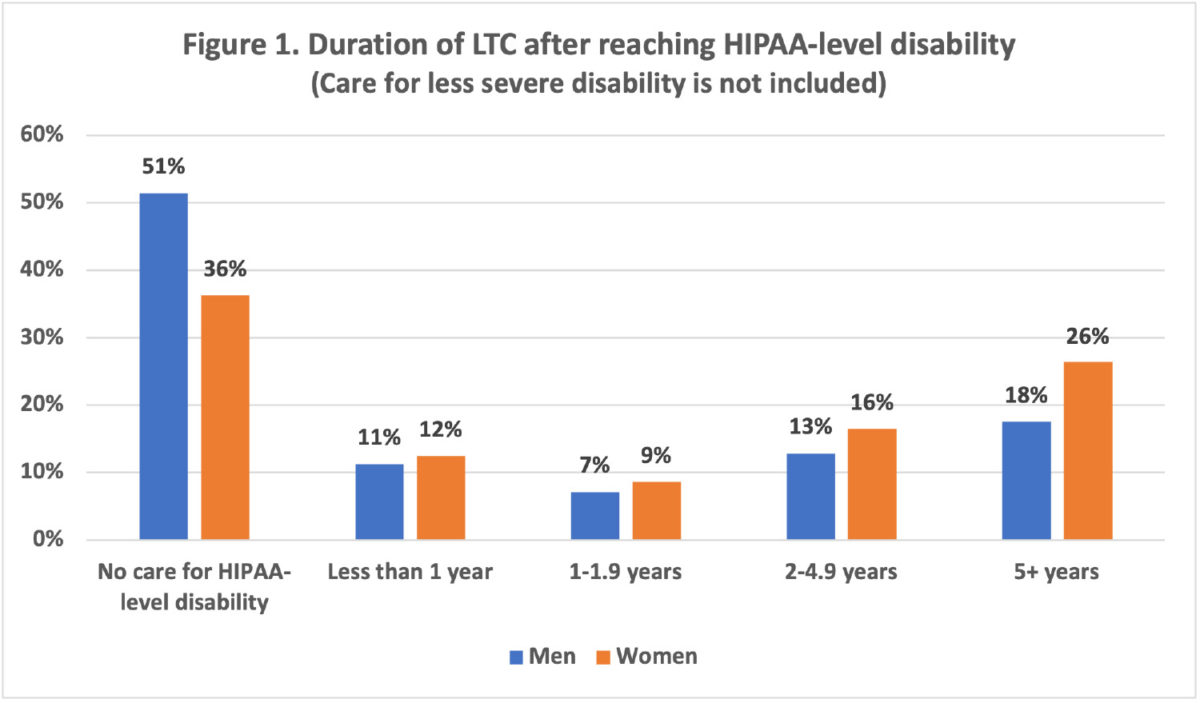

Figure 1 shows the distribution of LTC by duration.

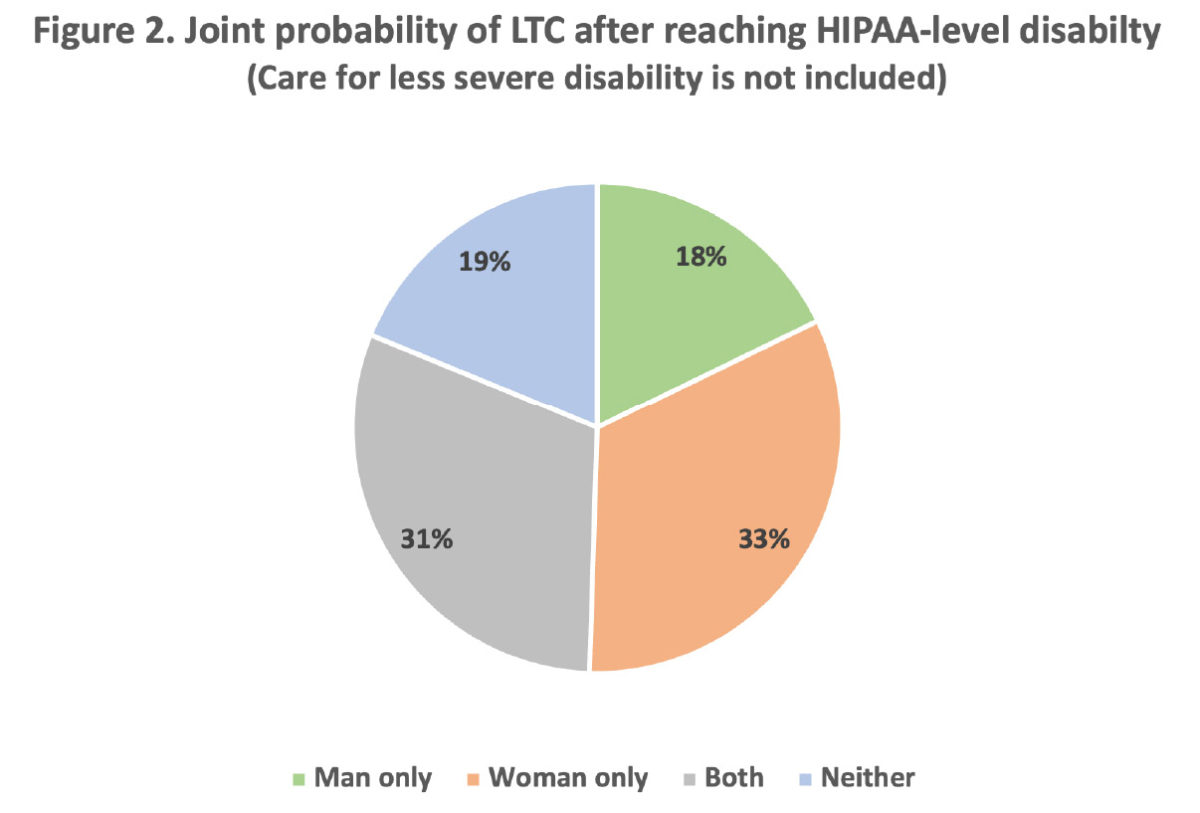

Data from the study was used to calculate the joint probability of LTC in couples (Figure 2). In eight out of 10 couples (81%), one or both partners will need LTC after reaching HIPAA-level disability.

The report highlighted a second issue of importance to financial professionals: Projections in the study underestimated the true likelihood and cost of LTC. The reason is because this and most similar studies do not count LTC that is provided before reaching HIPAA-level disability, which includes:

» LTC due to limitations of the instrumental activities of daily living (cooking, housework, laundry, managing finances and medical care, phone and computer use, shopping, and transportation).

» LTC because of inability to do one activity of daily living, rather than the two or more ADL limitations required by HIPAA criteria.

» LTC for some significant disabilities that can be mitigated with special equipment, such as wheelchairs, walkers, handrails and ramps.

How common is pre-HIPAA-level LTC? An earlier study by the Urban Institute suggested that the majority of LTC may be provided for people with lower levels of disability who do not meet the threshold for an LTC insurance benefit. Estimates are that one in four people (26%) who pay for LTCi and almost three in four (71%) who receive only unpaid LTC would not meet the threshold for benefits under a tax-qualified LTC insurance policy.

Health care and social service professionals have largely abandoned the expression “long-term care” because this term is associated with end-of-life care for severe disability. The preferred designation today is “long-term services and supports,” which includes a much broader array of unpaid and paid services that are needed as a result of aging, chronic illness or disability.

Points of engagement

» Financial professionals generally equate LTC with advanced disability that satisfies the benefit criteria of a tax-qualified LTCi policy. This approach creates an artificial distinction between LTC that is provided before and after meeting HIPAA criteria.

» For clients, LTC is not a “Yes or No” dichotomy that is determined by an arcane government law or an insurer’s benefit criteria. Instead, LTC is experienced as a continuum of care that evolves as disability worsens over time. It begins when care is first needed and costs are incurred.

» The majority of LTC may be needed at lower levels of disability that can exhaust family caregivers and deplete retirement funds. Some clients will never reach a point where their illness triggers an LTCi benefit, usually because death occurs at an earlier stage of disability.

» Recognition of the need for LTC at earlier stages of disability presents novel planning opportunities for financial professionals. The messages are that (1) LTC will be needed by the majority of individuals, and the likelihood is even higher for couples, (2) care will usually involve both unpaid (family) and paid caregivers, and (3) much, and sometimes all, of the care and cost will be incurred at lower levels of disability. This message ideally should be included in the financial plan, especially for single clients, widows, and couples with limited financial means who could spend down their assets before reaching the threshold for an LTCi benefit.

This more holistic approach to LTC planning will reassure clients that financial professionals are concerned about the impact of LTC across the entire spectrum of disability. Some clients will still have no interest in LTC planning. But merely introducing this topic often will lead to discussions about investments, wealth transfer, financial planning, closer ties to adult children who will be the main caregivers and potential clients in the future, as well as product options, including life and LTC insurance, annuities and Medicare supplement insurance.

This overlooked asset could help optimize your clients’ financial plan

A life lesson in success — with John Wheeler

Advisor News

- Americans aren’t turning retirement plans into action, LIMRA finds

- Ashley Hinson ‘death tax’ story collides with truth

- How advisors can prepare clients for an uncertain retirement landscape

- Investors aren’t waiting out uncertainty

- Transamerica and Advo(k)ate Advisors launch pooled employer plan

More Advisor NewsAnnuity News

- Corebridge annuity sales slip ahead of Equitable marriage

- California teachers settle class-action lawsuit over in-plan annuity fees

- Jackson Financial CEO caps 40-year career with blockbuster Q2

- Lumos Insurance introduces the Immediate Care Plan to help families fund long-term care

- NAIC regulators begin consensus phase on annuity illustration overhaul

More Annuity NewsHealth/Employee Benefits News

- VARIABILITY IN REBIMBURSEMENT RATES FOR STATE-FUNDED ABORTION SERVICES FOR MEDICAID ENROLLEES: A 2026 UPDATE

- GOVERNOR NEWSOM ANNOUNCES APPOINTMENTS 8.7.26

- Small school districts unite to lower health costs

- Endorsing Janoo

- Ashley Hinson unveils insurance transparency bill amid scrutiny of her health care record

More Health/Employee Benefits NewsLife Insurance News

- Indiana eyes more oversight of insurance companies' exposure to private credit

- HEALEY-DRISCOLL ADMINISTRATION RETURNS $14.5 MILLION TO HEALTH AND DENTAL INSURANCE CONSUMERS AND BUSINESSES

- ‘Uniquely positioned’: Equitable outlines future post-Corebridge merger

- Don't keep checks with clerical errors

- The insurance distributor that builds its own software will win the next decade

More Life Insurance News