Life insurance and annuity sales: What’s ahead for 2025?

Variable universal life and registered index linked annuities are expected to see the highest percentage of growth across life and annuity products in 2025, two LIMRA executives said during a recent webcast.

Bryan Hodgens, head of LIMRA research, and John Carroll, LIMRA senior vice president and head of life and annuities, provided a glimpse at what 2025 could bring to life and annuity sales while recapping what is setting up to be a record year for some product sales in 2024.

Life sees sustainable spike since COVID-19

The COVID-19 pandemic brought about a significant amount of growth in life insurance sales, and that spike has been sustainable for the past four years, Carroll said.

For 2024, life insurance new annualized premium is expected to increase between 1% and 2% year over year, to $15.9 billion.

Policy count has been flat, Carroll said, while premium has gone up. “But overall, it’s good news. We did see growth this year.”

Whole life and term life make up about 85% of life insurance sales. Carroll said LIMRA expects whole life sales to end 2024 down from 2023. But term life sales have been on the rise, he noted, and attributed the increase to more young consumers buying term insurance digitally.

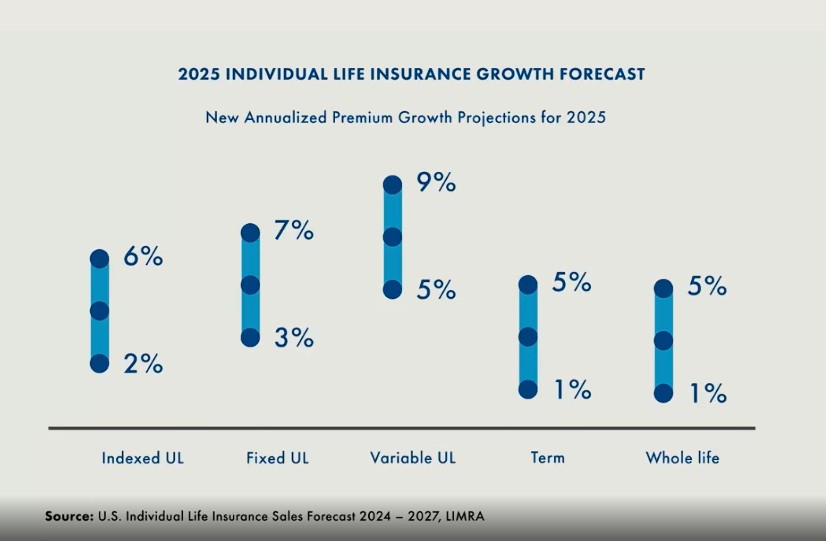

A big area of growth in life insurance will be VUL, Carroll predicted. LIMRA forecasts VUL sales for 2024 to be up between 12% and 16% over 2023. This year promises to be a strong year for VUL as well, he said, with sales expected to increase between 5% and 9% over 2024.

Indexed universal life carriers have been simplifying their products and processes, and sales figures are reflecting that, Carroll said. IUL sales are projected to grow between 3% and 7% from 2023 to 2024 and from 2% to 6% for 2025.

Conditions are ripe for annuity sales

Economic and demographic conditions combined to create a fertile environment for annuity sales, Hodgens said.

LIMRA estimates 2024 annuity sales to be $435 billion, up from $385 billion in 2023 and an increase of 70% since 2014.

Fixed rate deferred annuities represent the largest area of growth in 2024, he said, with RILA and fixed indexed annuity sales also on the rise. Single premium immediate annuities and deferred income annuities will have record sales in 2024.

“It has been a really good few years but things are changing,” Hodgens said. Consumer interest in fixed rate deferred annuities is expected to wane as interest rates fall.

Still, annuity sales are predicted to be robust in 2025 as an aging population seeks security and equity markets continue to be strong but volatile.

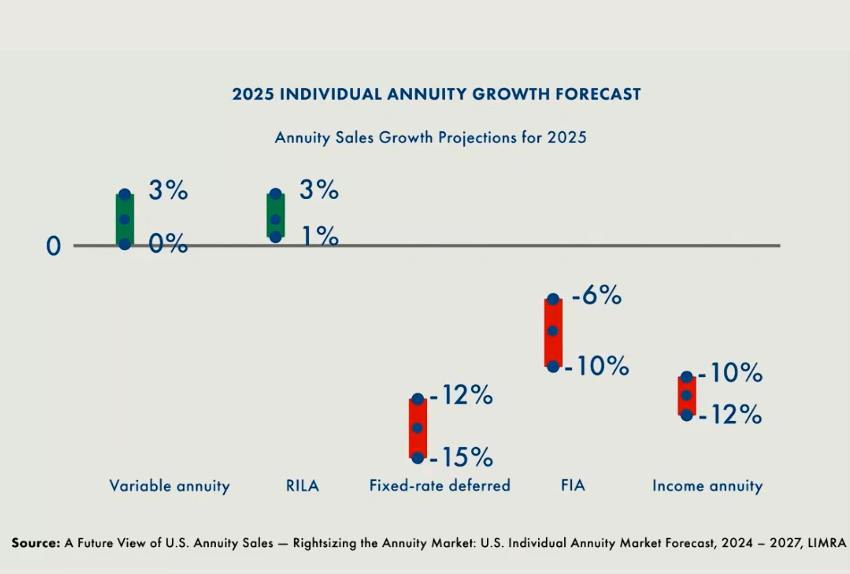

RILAs and variable annuities are expected to see growth of between 1% and 3% from 2024 and 2025. Fixed rate deferred, fixed indexed and income annuities are expected to see sales decline.

RILAs are expected to close out 2024 with between $62 billion and $66 billion in sales, Hodgens said, for an 11th consecutive year of record sales. This comes after RILA sales in 2023 totaled $48 billion.

For 2025, LIMRA projects RILAs sales will continue to lead growth among annuity products.

“This is the future,” Carroll said.

© Entire contents copyright 2025 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

In wake of fires, Calif. issues 1-year moratorium on insurance cancellations

Common myths and misconceptions about IUL

Advisor News

- Nearly half of nonretirees doubt they will fully retire

- How much could failure to fund Social Security cost average Americans?

- How can more Americans achieve financial independence?

- Savers vs. spenders: How money management attitudes impact financial confidence

- Demonstrating the value of life insurance to Gen Z

More Advisor NewsAnnuity News

- Jackson CEO Laura Prieskorn to retire at the end of 2026

- Has your annuity been reinsured in the Cayman Islands? Here’s why it matters

- DOL slams pension risk transfer lawsuit as ‘opportunistic’ litigation

- AM Best Affirms Credit Ratings of New York Life Insurance Company and Its Subsidiaries

- Advisors don’t have an annuity problem; they have an integration problem.

More Annuity NewsHealth/Employee Benefits News

- ICYMI – CANDIDATE COOPER NOW TRYING TO BLAME HIS HEALTH INSURANCE PALS FOR GOVERNOR COOPER'S 57% INCREASE IN HEALTHCARE COSTS IN NC

- Business People: Edric Funk to take over as Toro Co. CEO

- Insurers propose premium increases for ACA customers in Iowa

- How Does New CareScout Long-Term Care Insurance Policy Compare In Cost

- They harvest the nation’s food, but a new rule may strip them of health insurance

More Health/Employee Benefits NewsProperty and Casualty News

- Lenoir council to discuss flood insurance changes, cell tower

- 4 Myths about Insurance in California

- Connecticut Attorneys Title Insurance Company Trademark Application for “CATIC ACADEMY” Filed: Connecticut Attorneys Title Insurance Company

- Florida Democrats Annette Taddeo and Earle Ford compete to face CFO Blaise Ingoglia in November

- NEW MERKLEY BILL TACKLES DUAL CRISES OF WILDFIRE RISK AND INSURANCE AFFORDABILITY

More Property and Casualty News