How annuities can enhance retirement income for post-pension clients

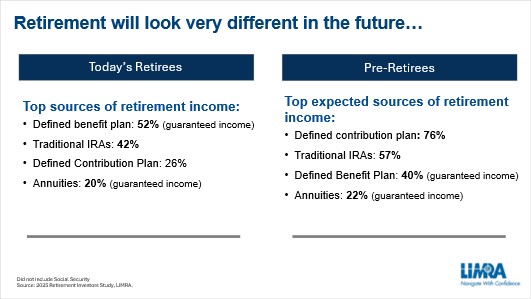

Today’s retirees are in a different situation than what future retirees will experience. Many current retirees have a defined benefit (or pension) plan while preretirees will need to rely more on personal savings and a defined contribution plan, such as a 401(k).

“LIMRA research shows more than half of current retirees (52%) with at least $100,000 in investible assets have access to a pension as part of their guaranteed lifetime retirement income. In contrast, just 40% of preretirees report having a defined benefit plan and expect to draw a pension,” Bryan Hodgens, senior vice president and head of LIMRA research, said in a recent LinkedIn Live discussion.

“Our research shows that 30% of today’s retirees feel very confident their income should be able to sustain them if they live to be 90 years old, where only about 19% of preretirees have the same confidence level,” he added.

Michael Finke, LIMRA retirement income institute fellow and professor of wealth management at The American College, joined Hodgens to discuss how annuities can replace bond and cash allocations to enhance retirement income security for current and future retirees.

“Ultimately, there are only two places for money can go in retirement. It can either go to our beneficiaries or we can spend it. So how do we put together an efficient plan for spending our money during our lifetime and then also transferring wealth at death in the most effective fashion?” he asked.

Transferring risk

Finke discussed how it’s important to build a retirement-focused portfolio that's not simply composed of stocks and bonds, but also includes insurance products when there are risks that are better addressed by an institution rather than being taken on by the individual.

Finke noted that for every dollar you have in bonds, you would be able to spend between 30% and 40% more if you had invested that money in an annuity or life insurance product that allows you to transfer longevity risk.

According to Finke and Hodgens, there is a record amount of money (more than $7 trillion dollars) sitting in certificates of deposit or some kind of money market or cash-equivalent type of account. Although that money is earning interest, the interest is taxed at your ordinary income tax rate annually.

Instead, Finke said, consumers can buy a future income through a deferred annuity where the growth is not subject to annual taxation until they pull the money out.

Using a birthday cake analogy to explain annuities

Since annuities can be an abstract concept that can often be difficult for a consumer to understand, Finke uses the analogy of a birthday cake for a child’s party to explain how they work.

He says to imagine you have a birthday cake, and you know there will be somewhere between five and 40 children coming for a birthday party. Maybe on average, there will be 20 children at the party, but you need to decide how big a slice you want to cut from the birthday cake.

Do you cut it into 20 slices? In this case, half of the time you're going to run out. Now, do you cut it into 30 slices? That can be a little risky, so maybe you cut it into 35 slices if you're risk-averse.

When the first child arrives, you cut them a tiny slice of cake. While they may be disappointed, you don’t want to run out. By the time the 13th child shows up, you start to get nervous and cut even smaller slices.

What if instead there was a bakery that makes thousands of cakes every year? The bakery agrees to make a deal that if more than 20 children show up, they will provide a second birthday cake. You just have to pay a little bit more for the birthday cake.

The bakery estimates, on average, how many extra slices of cake they will provide and charges a fair price that incorporates a little bit of profit for that added expense.

This allows people to cut the first birthday cake into 20 slices, and if more than 20 children show up, then the bakery provides a second birthday cake. And maybe you have to cut out another three or four slices of cake, because on average, you know, it's going to be pretty rare that they're going to have to use up all of the second birthday cake.

Doing this actually transferred an idiosyncratic risk of not knowing how many children will show up to the birthday party to an institution (a bakery).

The bakery can take on this risk because it can spread it over a thousand different birthday parties. Some birthday parties will be really expensive, while others won’t even get through the first birthday cake.

“You can do the same thing in retirement with an annuity, where the insurance company takes on the risk of you living longer in retirement,” Finke said.

“The annuity takes away that longevity risk and allows you to carve out a portion of your investment portfolio, and spend more from that portion of the investment portfolio,” he added.

Hodgens said retirees must take a more goals-based approach. “We need to educate consumers on how to build up their confidence level and plan for guaranteed income with annuities,” he said.

© Entire contents copyright 2026 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

Charitable giving planning can strengthen advisor/client relationships

Advisors in Texas and California banned for fraud scams

Advisor News

- The 3 things that shrink your Social Security income

- Proposed legislation takes aim at Social Security shortfall

- The overlooked retirement security risk that must be addressed

- What advisors should know about hedge funds in retirement planning

- Retirement control is top success measure for middle class, ACLI says

More Advisor NewsAnnuity News

- Trademark Application for “EMPOWER YOUR MONEY” Filed by Empower Annuity Insurance Company of America: Empower Annuity Insurance Company of America

- Built-in guaranteed annuities: What advisors should know

- Malibu Life Holdings Completes Acquisition of TruSpire, Establishing Malibu USA and Accelerating Entry into the U.S. Retail Annuity Market

- Why job boards are failing insurance agencies

- MassMutual Ranks No. 100 on the 2026 Fortune 500® List

More Annuity NewsHealth/Employee Benefits News

- Yorktown eyes budgeting options to cope with insurance rate spike

- New Managed Care Findings Reported from Harvard University T.H. Chan School of Public Health (Using prescription drug data for timely assessments of state insurance coverage rates: a validation study): Managed Care

- Reports from Michelle Cornette and Co-Researchers Add New Data to Findings in Managed Care (Enhancing Medicaid Behavioral Health Crisis Reporting: A Multisource Approach to Capturing Crisis Service Events): Managed Care

- New Managed Care Findings from University of California San Francisco (UCSF) Outlined (Medicaid patients have decreased access to urologic care: a nationwide cross-sectional study): Managed Care

- How Medical Bills Are Handled After a Personal Injury Accident in Atlanta

More Health/Employee Benefits NewsLife Insurance News

- Best's Review Leaders Issue Ranks Top Global Brokers and More

- Fortitude Re Announces $3.8 Billion Long-Term Care Reinsurance Agreement with Unum Group

- Unum Group Announces $3.8 Billion Long-Term Care Reinsurance Transaction with Fortitude Re

- Before you debate premium financing, understand the bigger picture

- NAIFA praises House committee approval of Clarity for Compensation Act

More Life Insurance News