Gen X? Make It Gen $: Boomers Set To Funnel Big Bucks To Heirs

Generation Xers may have grown up cynical and sneering as their baby boomer siblings consumed the environment, cheap real estate and all the pre-HIV free love, but the slackers will enjoy the last smirk as they reap trillions upon trillions of dollars in generational transfer.

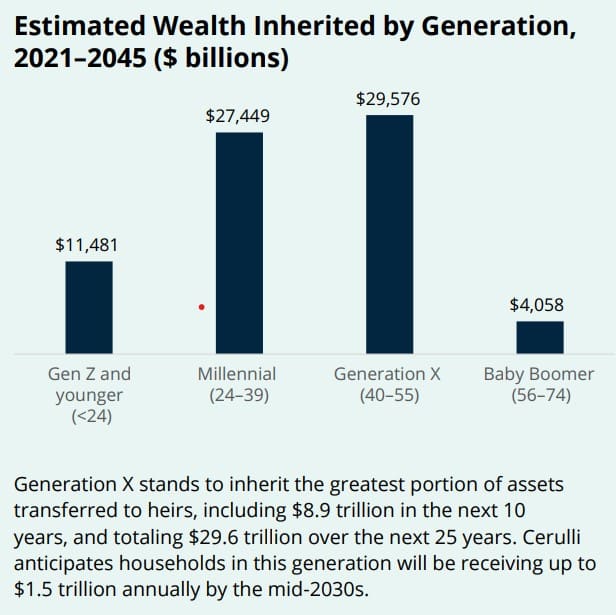

They will be the big winners with nearly $30 trillion between now and 2045, while boomers make do with their measly $4 trillion, according to Cerulli’s report “U.S. High-Net-Worth and Ultra-High-Net-Worth Markets 2021: Evolving Wealth Demographics.”

Over the next two decades, $84.4 trillion in wealth is expected to pass mostly (63%) from boomer hands, with $11.9 trillion of it going to charity.

The spigot of benjamins will open relatively slowly, with Gen Xers receiving $8.9 trillion over the next 10 years, but they will be seeing $1.5 trillion annually by the mid-2030s.

Boomer Jrs., or millennials, will be right behind their cool aunts and uncles with their own $27 trillion slice of America’s pie, according to the report. Although Millennials will be getting a relatively paltry $5 trillion over the next 10 years, they will surpass Gen Xers during the 2040s and by 2045 inherit more than $2.5 trillion annually.

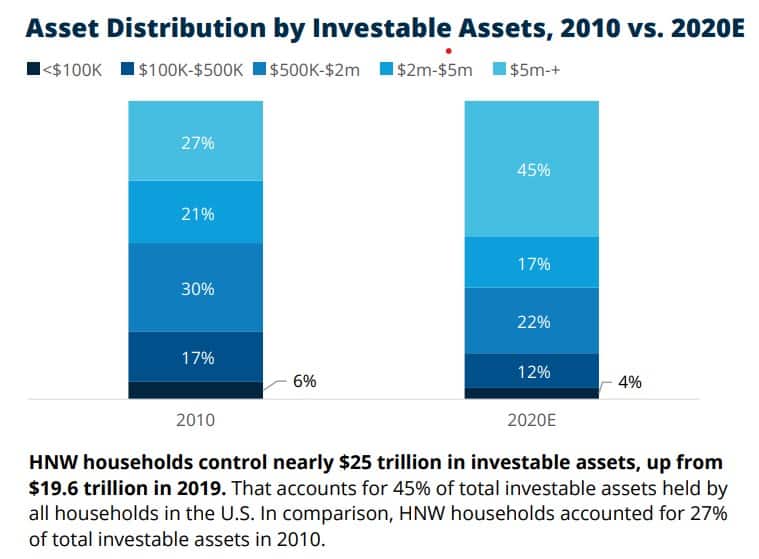

The rich will still be getting richer, with $35.8 trillion, or 42% of the transfers, to come from high-net-worth and ultra-high-net-worth households, which together make up only 1.5% of all households.

The Rich’s Riches

As of 2021, nearly 2 million high-net-worth households control nearly half of the total investable assets in the United States. The report’s authors warned advisors that they can’t expect to just wait for the money to find them.

“The need to deliver a differentiated advisory experience based on each client’s unique needs and expectations has become more important given the expanding number of wealth management options available to HNW investors,” according to the report.

Wealth begat significant wealth over the past few decades mostly through mutual and hedge funds, 54%, while 26% grew from individual securities.

That means they will need help managing the tax impact of transitioning to retirement and assistance in planning their estates. Clients will also be used to clicking their way through their financial services because 70% of all investors use self-directed providers, with nearly the same percentage of clients with more than $1 million in investable assets using those providers.

A quarter of HNW practices are considering adding an advice platform in the next three years, according to the report. And 40% will be adding services because their clients demand them, with 27% of HNW firms planning to add services to keep up with competitors.

Keeping Up

To remain relevant to the younger generations of investors, advisors will need to pay attention not only to tech, but also to ethical investing.

Key in the tech upgrades will be improving the firms’ operational efficiency. That means tech providers will be in demand by smaller financial firms, which will need seamless integration between the many tools that advisors need to serve the next generations.

The ethical part of the equation means environmental, social and governance investing. Already, 67% of HNW practices are using ESG investing standards with more expected to use them this year.

“While the broader retail market is still very much in the early phases of leveraging ESG,” according to the report, “this has long been part of wealth managers’ conversations with HNW clients.”

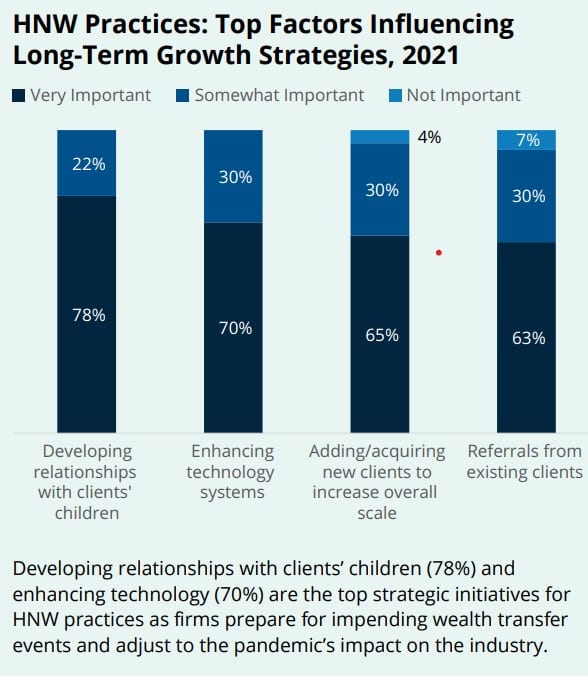

As wealth passes generations, those dollars often leave the original clients’ firms. But some HNW practices are trying to keep that wealth in-house, with 34% of the firms using younger employees in conversations with clients’ children.

“Having younger team members work with HNW households’ next-generation kin creates opportunities to develop emerging talent and can improve the stability of the overall client relationship,” according to the report.

The research showed that family meetings and regular communication (81%) is the most-effective wealth transfer planning strategy by HNW practices, followed by educational support (59%), and organized succession planning (31%), according to Cerulli.

Advisors should make family events a regular part of the process, said Cerulli analyst Chayce Horton.

To improve relationships across generations, Horton recommends making family events a regular part of the advisory process. Extending interfamily relationships beyond the original clients not only keeps the next generation with the practice, it also creates a greater sense of responsibility along with greater trust in the advisors.

Not having a strategy is a plan to lose business, Horton said: “Winners of walletshare will need to be prepared for changes to their business model and open to evolving with the needs of a younger demographic.”

Steven A. Morelli is a contributing editor for InsuranceNewsNet. He has more than 25 years of experience as a reporter and editor for newspapers and magazines. He was also vice president of communications for an insurance agents’ association. Steve can be reached at [email protected].

© Entire contents copyright 2022 by InsuranceNewsNet. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.

Finseca And Forum 400 Announce Merger

How The Industry Can Bridge The Income Gender Gap

Advisor News

- Embracing a family-centric approach to financial planning

- Family communication: Financial planning’s growing blind spot

- Americans aren’t turning retirement plans into action, LIMRA finds

- Ashley Hinson ‘death tax’ story collides with truth

- How advisors can prepare clients for an uncertain retirement landscape

More Advisor NewsAnnuity News

- Investigation finds deceptive sales, churning of annuities targeting postal workers

- Corebridge annuity sales slip ahead of Equitable marriage

- California teachers settle class-action lawsuit over in-plan annuity fees

- Jackson Financial CEO caps 40-year career with blockbuster Q2

- Lumos Insurance introduces the Immediate Care Plan to help families fund long-term care

More Annuity NewsHealth/Employee Benefits News

- New York Life Awards 20 Golden Futures Scholarships, Expanding Student Support Through Financial Education and Career Development

- Hinson unveils transparency bill amid scrutiny

- Genworth leans on mortgage unit, CareScout to offset Q2 LTC liabilities

- GeneDx Launches New Online Offering for Families to Improve Accessibility of Exome Testing for Children with Global Developmental Delay, Intellectual Disability and Epilepsy

- Govt Sets Ambitious Health Reform Agenda

More Health/Employee Benefits NewsLife Insurance News

- New York Life Awards 20 Golden Futures Scholarships, Expanding Student Support Through Financial Education and Career Development

- Built to Last: Winston-Salem—a quiet industrial powerhouse

- The silver economy ushers in a new era of life insurance growth

- Family communication: Financial planning’s growing blind spot

- Indiana eyes more oversight of insurance companies' exposure to private credit

More Life Insurance News