Florida homeowners continue to face insurance affordability crisis, report says

A report finds that the “rebuilding” of Florida’s property insurance market after Hurricane Ian struck the state in 2022 has reproduced many of the same conditions that left homeowners exposed in the last crisis.

The Insurance Fairness Project released the report, Behind Florida’s Insurance “Comeback”: The Same Players, the Same Risks.

“Florida families are paying more than ever for property insurance,” said Kyle Herrig, spokesperson for Unlocking America’s Future, during a recent news conference. “Premiums are up 54% since 2019 - the highest in the nation. Florida insurers are posting record profits and multimillion-dollar executive payouts.

“Upward of 20% of all Florida homeowners are now going without insurance. Reforms passed by Gov. Ron DeSantis enabled unchecked legal system abuse by insurance companies, where they delay, deny and defend against policyholders’ legitimate claims. Florida's insurance recovery is less a comeback and more a packaging of failure. The system remains dangerously vulnerable to another wave of insurer collapses, leaving families to foot the bill.”

In 2022, Florida lawmakers passed a regulatory overhaul aimed at stabilizing insurance markets after Hurricane Ian. But an analysis of the new market entrants shows that Florida’s insurance market remains fragile and undercapitalized, the report said.

The Insurance Fairness Project alleges that many of the new insurers entering the Florida marketplace have political connections and ties to past market abuses.

“State leaders have pointed to the influx of new insurers since 2022 as evidence of recovery, but beneath that surface optimism lies a more troubling reality: a revolving door of executives and investors resurrecting failed firms under new names, aided by inflated ratings and weak oversight.”

Shifting risk from Citizens to private insurers

Florida’s property insurance recovery has largely depended on shifting risk from Citizens Property Insurance Corp., the insurer of last resort, to private firms that are often small, politically connected, or linked to previously troubled companies, the report said. This strategy has reduced Citizens’ exposure and temporarily relieved market pressure, but it has done little to address the systemic problems that drive high premiums, limited competition, and uneven claims handling.

This practice concentrates financial risk among a narrow pool of fragile insurers instead of creating a genuinely resilient market, according to the report. These practices give regulators, policymakers and the public a false sense of security while leaving homeowners exposed to premium shocks, denied claims or coverage gaps when the next major storm hits.

The report said Florida’s insurance market remains based on what it called “undercapitalized companies, opaque ratings and a regulatory system that prioritizes market optics over homeowner protection.

“These vulnerabilities leave the market ill-equipped to absorb major losses from hurricanes or other catastrophic events.”

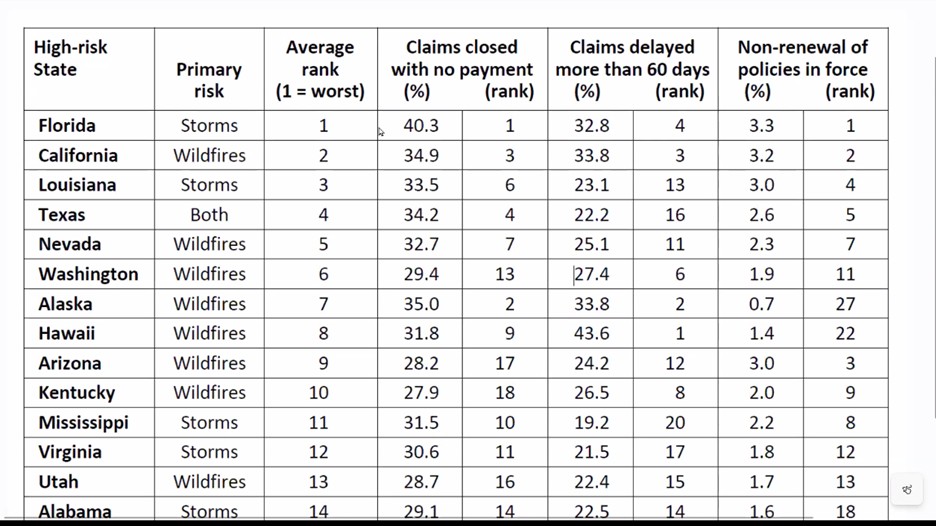

Florida is tops in unpaid claims

Martin Weiss, founder of Weiss Ratings, said Florida leads the nation as the state with the highest percentage of property claims closed with no payment (40.3%). Florida also ranks first in the percentage of in-force policies that are not renewed (3.3%) and fourth in the percentage of claims that were delayed more than 60 days (32.8%).

“The Florida P/C market was already in a state of collapse, and today, because of tort reform, our data shows it's worse,” Weiss said. “This leaves Florida and other states with two choices. They can let market forces play themselves out, driving the market into chaos, and then try to rebuild it from the bottom, or they can urgently implement preventative medicine to help avoid that outcome. The choice is theirs.”

Florida's insurance recovery is a 'mirage'

“Florida’s so-called insurance ‘recovery’ is a mirage – and one that will continue costing Floridians dearly,” said Lizzy Price, a spokesperson for the Insurance Fairness Project. “Weak oversight and political coziness have turned the state’s insurance system into a revolving door for industry insiders. Without independent ratings and real accountability, Florida isn’t preventing the next collapse, it’s paving the way for it.”

The report found the following:

- Recycling of failed firms: Four of the new insurers either appear to have been restructured from a company that became insolvent in the past decade, have strong ties to a company that became insolvent in the past decade, or have ties to a company that faced financial trouble and was on the brink of insolvency.

- Questionable claims performance: Five are among the 14 companies that Weiss Ratings found to have closed out more than half of their claims in 2024 without payment, or are led by executives whose former companies are on that list.

- Regulatory penalties: Four are among the eight companies recently assessed $2 million in fines by the Florida Office of Insurance Regulation over mishandling of hurricane claims.

The report called for Florida to move beyond cosmetic fixes in order to achieve true market stability. Independent oversight of insurers, transparent and reliable financial ratings, and enforceable accountability mechanisms are essential. Policies should prioritize the protection of homeowners and communities over the short-term benefit of private insurers or political expediency.

Without these reforms, the report said, Floridians will continue to shoulder the burden of the state’s fragile insurance system, paying some of the nation’s highest premiums while facing ongoing uncertainty about whether their coverage will hold when disaster strikes.

Two bills aimed at oversight, transparency

Florida State Sen. Carlos Guillermo Smith, D-17, has introduced two bills, Senate Bill 234 and Senate Bill 230.

SB 234 is aimed at oversight of property insurers through the state’s Office of Insurance Regulation. Smith said it will increase transparency on the use of managing general agent fees. It also will require the full public disclosure of all payments by those property insurance companies to their affiliates, alongside cost justifications for all of the services provided by those affiliates and the disclosure of profit margins that he said are often built into these affiliate transactions with their subsidiaries.

Smith’s bill caps managing agent fees at no more than 20% of gross written premiums, and it ensures that these fees are commensurate with market rates. The proposal also prohibits the payments of dividends and executive bonuses for those property insurance corporations who are claiming financial challenges and financial distress due to what Smith called “these exorbitant affiliate fee scheme structures.”

SB 230 would specify what information insurers may claim as so-called trade secrets when reporting financial information to the Office of Insurance Regulation.

“We know that insurers frequently hide what their true financial standing actually is, claiming that those numbers that they are shielding from regulation and accountability, are trade secrets,” Smith said. “With this proposal, we're clearly outlining what data may not be labeled as a trade secret, such as shareholder dividend dividends and profit sharing agreements.”

© Entire contents copyright 2025 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

Kyle Busch IUL lawsuit moved to federal court at PacLife’s request

‘Take this as a win’: NAIC creates new life insurance illustration group

Advisor News

- Transamerica and Advo(k)ate Advisors launch pooled employer plan

- ‘I wish I’d met him sooner:’ Karlan Tucker remembered for integrity, faith

- Why women must be more engaged in investing

- SEC moves to simplify electronic delivery of investor communications

- Nearly half of nonretirees doubt they will fully retire

More Advisor NewsAnnuity News

- LIMRA: Annuity sales set new quarterly record with $123.9B in Q2

- CANNEX names Gary Baker as its new CEO

- Corebridge adds options to its Power Series of indexed annuities

- Corebridge Financial enhances The Power Series of Index Annuities

- LIMRA predicts strong life and annuity sales for the rest of 2026

More Annuity NewsHealth/Employee Benefits News

- Employers are considering ICHRAs, but barriers to adoption remain

- AI belongs on your organizational chart, and that’s a good thing

- New dashboard tracks Kansas Affordable Care Act enrollment by legislative district, county

- ICYMI – CANDIDATE COOPER NOW TRYING TO BLAME HIS HEALTH INSURANCE PALS FOR GOVERNOR COOPER'S 57% INCREASE IN HEALTHCARE COSTS IN NC

- Business People: Edric Funk to take over as Toro Co. CEO

More Health/Employee Benefits NewsLife Insurance News

- LIMRA predicts strong life and annuity sales for the rest of 2026

- Best’s Market Segment Report: AM Best Maintains Stable Outlook on Vietnam’s Non-Life Insurance Segment

- AM Best Comments on Credit Ratings of Horace Mann Educators Corporation and Its Subsidiaries Following Announced Transaction with Medical Mutual of Ohio

- AM Best Affirms Credit Ratings of Hanwha General Insurance Company Limited

- Globe Life boosts Q2 earnings, eyes AI shift for long-term growth

More Life Insurance News