Rate Increase Bodes Well For Fixed Annuity Sales

The fixed annuity industry could harvest some happiness in the months ahead. That’s because new sales of fixed annuity products will likely increase in the wake of the 0.25 percent jump in a key interest rate the Federal Reserve announced Wednesday.

The growth actually will be a continuation of the strong sales seen in third quarter, well before the Fed’s rate announcement. That’s according to Jeremy Alexander, president of Beacon Research.

Carriers have been making gradual increases in their crediting rates in traditional fixed annuities and in their cap rates in fixed index annuities for several months, Alexander explained.

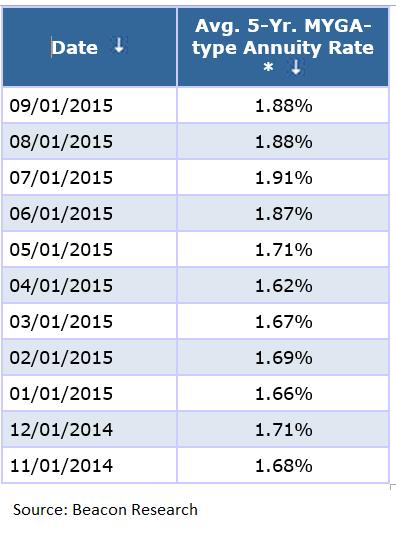

To illustrate, he provided InsuranceNewsNet with a chart showing the gradual rise in average crediting rates over the past several months. These were for five-year multi-year guaranteed annuities (MYGAs) sold by 94 percent of carriers in the market.

On Nov. 1, 2014, the average crediting rate for these products was 1.68 percent, the chart shows. The rates inched up and down after that and reached a high of 1.91 percent on July 1, 2015. On Sept. 1, the last date available, the average rate was down slightly, to 1.88 percent, but not back to the low.

The caps in fixed index annuities, the leading fixed product line by sales, also have risen since last August, he said.

Small increases have impact

The rate increases seem small, Alexander said. However, they can make a lot of difference to annuity buyers who, for instance, want to lock in a rate in MYGA as they dig out from the era of prolonged rock bottom interest rates.

He attributed the “strong growth” in third-quarter fixed sales in large part to those incremental increases. Total fixed sales rose by 15.9 percent to reach $26.5 billion for all types of fixed annuities, according to Beacon’s data.

The top selling line, indexed annuities, saw third quarter sales rise by 14.5 percent over second quarter to reach a new quarterly record of $14.4 billion. They also rose by 23.3 percent over third quarter last year.

MYGA sales volume, although substantially smaller at $3.4 billion in third quarter, shot up too. These sales rose 16 percent over second quarter, when they were up 26.4 percent from the previous quarter, he said.

This growth wasn’t all rate driven, Alexander said. This year’s volatility in the equity markets was a factor too. “We’ve always seen a flight to safety when equities markets are volatile and when fixed rates are rising.”

Now that the Federal Reserve has moved to increase its benchmark interest rate for the first time in nearly a decade, “we’re expecting continued gradual rate increases going forward,” Alexander said. He predicts that fixed sales will continue to be strong as a result.

In particular, he said he is expecting to see greater sales of MYGA products. “As rates rise, people typically prefer to ladder their annuities in MYGAs,” he said.

He also thinks index annuity sales will keep on growing. This growth will be thanks to the rising rate caps, dislike of volatility in the securities markets and the presence of lifetime income riders which many indexed annuities now offer.

“If consumers can get a high cap on the upside, living benefits for retirement income, and no downside all in one index annuity, that’s a deal-breaker for many who would otherwise purchase securities or variable annuities or just keep their money in cash,” Alexander said.

What to watch

Still, actual results may differ in surprising ways, he cautioned.

For instance, some clients might decide to put off buying a fixed annuity precisely because of the Fed’s action. “They may decide to delay buying a MYGA so they can lock in a higher rate later on,” he said.

Similarly, people who have been showing interest in purchasing immediate annuities may decide to delay the purchase for the same reason — “wait a little longer.”

On the carrier side, Alexander said, “Corporate profits typically decline when cost of capital goes up.” This could affect some company planning. However, he added, annuity carriers today tend to be well hedged for annuity rate increases - especially after all the downsizing and de-risking they did in the post-recession era - so producers can look to continued availability of products.

For those wanting to follow the rate trends of most significance to the industry, Alexander recommended keeping tabs on 10-year corporate bond rates. “These more closely represent insurance company portfolio holdings than do Treasury rates,” he said.

InsuranceNewsNet Editor-at-Large Linda Koco, MBA, specializes in life insurance, annuities and income planning. Linda can be reached at [email protected].

© Entire contents copyright 2015 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

SEC Bulletin Targets VA Charges, Expenses

Critical Illness Plans Become A Popular Voluntary Benefit

Advisor News

- Demonstrating the value of life insurance to Gen Z

- Poor money habits are a dealbreaker in a new relationship

- DC plan sponsors see opportunity in alternatives

- The American Dream: Redefined as financial stability

- Partial annuitization: How advisors can help clients balance income, growth

More Advisor NewsAnnuity News

- CA judge certifies class action in teachers’ lawsuit over in-plan annuity fees

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Managing Director Joins ‘Target Topics’ Podcast to Discuss State of Delegated Underwriting Authority Enterprises Market

- KBRA Assigns Rating to TruSpire Retirement Insurance Company

- Partial annuitization: How advisors can help clients balance income, growth

More Annuity NewsHealth/Employee Benefits News

- Coalition targets health insurance costs, calls for relief

- Arkansas Explained: What's happening to the state's Medicaid expansion?

- CT Congressman Wants Legal Support For Patients Denied Health Coverage

- Coalition targets health insurance costs, calls for relief

- Map: Where Obamacare Enrollment Is Falling

More Health/Employee Benefits NewsLife Insurance News

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Upgrades Credit Ratings of Sagicor Financial Company Ltd. and Most of Its Subsidiaries

- Trust, technology and the future of claims

- New York Life Launches an Indemnity Benefit for its Asset Flex Long-Term Care Insurance Solution

- AM Best Affirms Credit Ratings of DB Insurance Co., Ltd.

More Life Insurance News