A tax-advantaged solution for long-term care needs

As more adults enter retirement age, many have dreams of vacationing, seeing grandchildren, volunteering with their favorite charities or catching up with all of their bucket list items. After a lifetime of working and saving, many consumers are expecting to lead this relaxed life courtesy of their investment returns and accumulated retirement plans. Most have been taught the rule of 4% withdrawals and have done the back-of-the-envelope math to understand how much of a nest egg they need in order to relax in retirement. Unfortunately for these future retirees, many experts agree that the 4% rule in today’s environment could have dire consequences for many thanks to several factors including inflation, escalating health care costs and market volatility.

In addition to these issues, most Americans are unprepared for a long-term care event during their lifetime. According to the Aspe Research Brief presented to the U.S. Department of Health and Human Services in 2020, more than 50% of people over age 65 will require long-term care at some point, making this a huge pothole for half the population on their retirement road map.

Long-term care needs may be brief for some, but the average — a length of three years, and a cost of more than $120,000 - will have a significant impact on the portfolios of those impacted. It’s estimated that the U.S. population ages 65 and older will exceed 70 million by 2030. The vast majority of this age cohort is unprepared for this type of expense, since many are on fixed incomes.

Given this conundrum, there are several ways to solve this aging dilemma, one of which comes courtesy of the Pension Protection Act. When this was passed by Congress in 2006, it gave non-qualified deferred annuities some significant tax advantages. According to Internal Revenue Code 7702(b), long-term care benefits are generally treated as excludable accident and health insurance benefits and are income tax free. However, in order to qualify for these advantages, the taxpayer must be chronically ill. They must be certified by a licensed health care practitioner as being unable to perform at least two of six activities of daily living or have severe cognitive impairment. This ability to trigger tax-free payments from a tax-deferred vehicle is an enormous tax efficiency opportunity for those impacted by an LTC event.

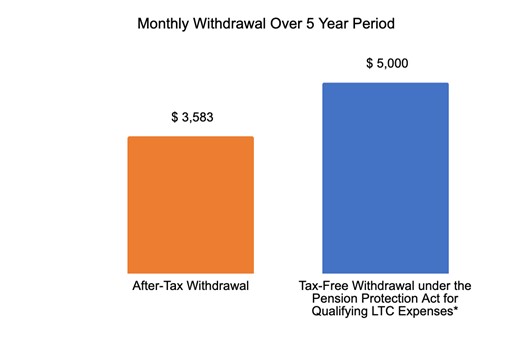

Let’s look at an example of how the taxable and tax-free withdrawals look: An annuity owner has accumulated $250,000 in a tax-deferred non-qualified annuity with a $50,000 cost basis. In the case of regular withdrawals and assuming a 34% income tax rate, the policyholder would receive $3,583 per month in benefits for a five-year period. That policyholder would receive $5,000 per month if they withdrew the same $250,000 to cover a qualified long-term care event, if the underlying annuity had a long-term care rider.

*Assumes 34% income tax rate. Based on $250k in accumulated gains on a $50k initial investment. Tax-free withdrawals are only available when an individual is deemed "chronically ill" (inability to perform 2 out of 6 activities of daily living or severe cognitive impairment) by a certified healthcare practitioner. The annuity contract must meet guidelines for qualified long term care insurance under IRC Section 7702(b).

The advantages of a fixed indexed annuity is that a policyholder can aim for more equity market-like returns and potentially drive greater accumulation. Add the long-term care rider to this and suddenly, the policyholder turns this accumulated, tax-deferred growth into a tax-free income stream, assuming they qualified under 7702(b).

Many annuity products also offer consumer-friendly features such as guaranteed underwriting approval, where every applicant is medically approved to purchase them. This allows all clients who desire tax-deferred growth and long-term care coverage needs to buy the product, irrespective of their health status. One of the major downsides of traditional long-term care insurance is that by the time a consumer is aware of the need for coverage, they often can’t qualify for it. With the guaranteed underwriting approval, all applicants are able to purchase (subject to suitability of the annuity purchase), regardless of their health. Some features include embedded wellness programs, aimed at helping policyholders age in place by staying active and engaged in their own healthy lifestyle.

Guaranteed underwriting approval and embedded wellness programs are just two of the more friendly features. You also can find annuity combination products that have multiple accumulation strategies, rebalancing and dollar cost averaging abilities and varied liquidity features among other consumer-centric design elements.

Retirement planning, even when done correctly, is still dependent on variable factors, such as inflation, rising health care costs and market volatility. Add to this the likelihood of needing long-term care assistance and the problem is more complex and even harder to solve. The good news is the introduction of new products that allow consumers to try to overcome these issues, while also protecting them from long-term care needs. This is an area that is growing and will have an impact on the aging populations of the future.

Larry Nisenson is the chief growth officer at Assured Allies. He may be contacted at [email protected].

© Entire contents copyright 2023 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

Worry about IRS refunds rises as refund amounts drop, survey says

Middle-income families offer opportunity for financial advisors, report says

Advisor News

- Poor money habits are a dealbreaker in a new relationship

- DC plan sponsors see opportunity in alternatives

- The American Dream: Redefined as financial stability

- Partial annuitization: How advisors can help clients balance income, growth

- Guide women along the walk through widowhood

More Advisor NewsAnnuity News

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Managing Director Joins ‘Target Topics’ Podcast to Discuss State of Delegated Underwriting Authority Enterprises Market

- KBRA Assigns Rating to TruSpire Retirement Insurance Company

- Partial annuitization: How advisors can help clients balance income, growth

- Guide women along the walk through widowhood

More Annuity NewsHealth/Employee Benefits News

- Atrium’s WakeMed acquisition faces new hurdle after State Health Plan decision

- Fewer members, more profit: UnitedHealth shares surge on Q2 earnings beat

- ARE SURVIVAL RATES FOR ADULTS WITH CONGENITAL HEART DISEASE LINKED TO SPECIALIZED CARDIAC CARE ACCESS?

- THIRTY-TWO YEARS, ZERO RESULTS: NRSC CHARGES SHERROD BROWN SOLD OUT TO BIG INSURANCE

- Employers weigh retention, costs in developing benefits strategies

More Health/Employee Benefits NewsLife Insurance News

- Globe Life Inc. (NYSE: GL) Records 52-Week High Thursday Morning

- AM Best Upgrades Credit Ratings of Sagicor Financial Company Ltd. and Most of Its Subsidiaries

- Trust, technology and the future of claims

- New York Life Launches an Indemnity Benefit for its Asset Flex Long-Term Care Insurance Solution

- AM Best Affirms Credit Ratings of DB Insurance Co., Ltd.

More Life Insurance News