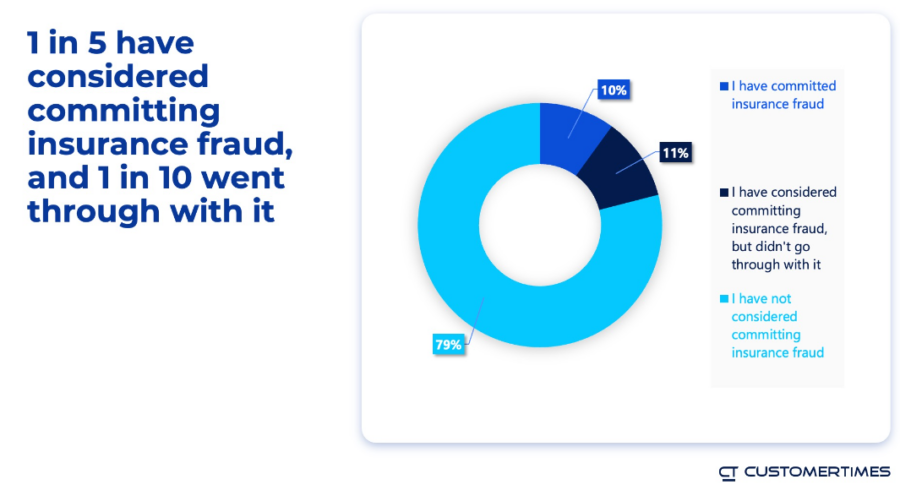

1 in 5 in study admit to considering insurance fraud

Insurance fraud is a pervasive issue in the U.S., with estimates suggesting it could cost the industry more $300 billion annually. But beyond the financial strain on insurers, it impacts consumers directly, leading to higher premiums and a sense of injustice among honest policyholders.

To delve deeper into this phenomenon, Customertimes conducted a survey of 2,000 Americans, shedding light on the prevalence of fraudulent claims and the underlying motivations driving them.

The findings reveal a concerning reality: one in five respondents admitted to at least considering committing insurance fraud, with 10% admitting to following through with their plans. Moreover, a significant portion of the surveyed population knew individuals who had either committed or contemplated insurance fraud.

The conclusions jibed with similar findings released last month by the Coalition Against Insurance Fraud, an organization of consumers, insurers, government agencies, prosecutors and others, all uniting to fight fraud.

“Consumer attitudes towards insurance fraud are concerning,” said Michelle Rafeld executive director of the coalition. “Studies show a significant portion of the population does not view it as a crime.”

Rafeld said that the same technology advancements that have made it easier for individuals to get their insurance, have also made it easier for sophisticated criminals to commit insurance fraud.

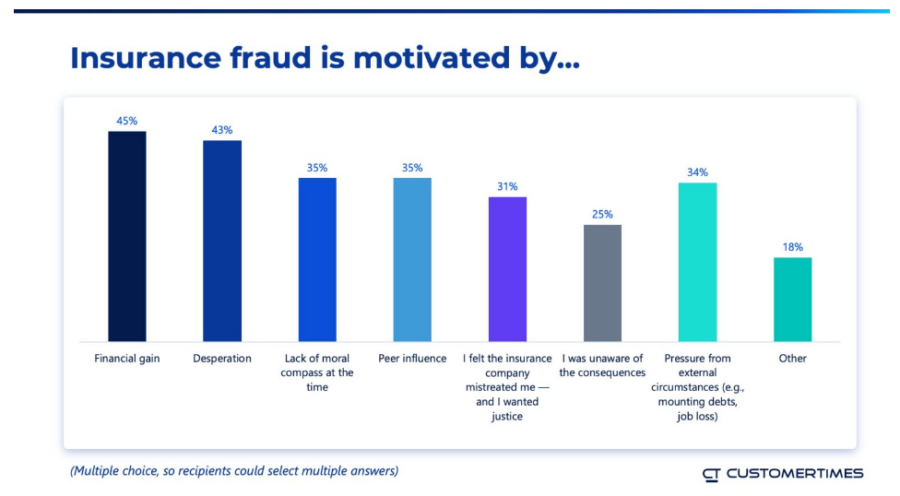

In the Customertimes survey, financial gain unsurprisingly emerged as the primary motivator for insurance fraud, cited by 45% of respondents. However, non-financial factors also played significant roles, including peer influence, a desire to address perceived injustices by insurers, ignorance of consequences, and desperation.

The study also highlighted consumers' perspectives on the role of policy loopholes and perceived unfairness in driving insurance fraud. Nearly half of Americans believed that loopholes in policies facilitated fraudulent activities, while a quarter considered insurance fraud justifiable when policies were deemed unfair. This subjective interpretation of fairness poses a challenge for insurers in crafting policies that are perceived as equitable by all parties involved.

Interestingly, consumers tended to view fraud committed by individuals as less serious than corporate fraud. While many expressed confidence in their ability to identify fraudulent cases, there was skepticism regarding insurers' capabilities in detecting and preventing fraud consistently.

Looking ahead, consumers expressed optimism about the potential of new technologies such as AI and data analytics to enhance fraud detection efforts. However, they also emphasized the need for insurers to prioritize consumer education and streamline communication processes. A majority felt that insurers were not doing enough to inform consumers about fraud prevention measures or adequately compensate fraud victims.

Moreover, consumers signaled a willingness to share more data if it contributed to fraud prevention efforts, underscoring the importance of transparency and collaboration between insurers and policyholders. Simplifying bureaucratic procedures and enhancing user experience emerged as key factors in building consumer trust and bolstering fraud prevention initiatives.

“If providers needed an additional incentive to improve the user experience, they should note that 80% of respondents said they would be more likely to trust insurance companies if they were less bureaucratic to deal with,” said Drew Sickler, VP salesforce for Customertimes. “If insurers can give consumers more confidence in their processes, then it could help provide valuable intelligence in preventing the scourge of insurance fraud.”

Addressing that scourge, he said, requires a multifaceted approach that encompasses consumer education, technological innovation, and a commitment to fairness and transparency within the industry.

“By heeding the insights gleaned from this study, insurers can take proactive steps to mitigate fraud risks and foster greater trust and accountability among all stakeholders involved in the insurance ecosystem,” he said.

Doug Bailey is a journalist and freelance writer who lives outside of Boston. He can be reached at [email protected].

© Entire contents copyright 2024 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

IRS again defers minimum distribution penalty for IRA beneficiaries

Revol One Financial retools with new annuity products, big goals

Advisor News

- Embracing a family-centric approach to financial planning

- Family communication: Financial planning’s growing blind spot

- Americans aren’t turning retirement plans into action, LIMRA finds

- Ashley Hinson ‘death tax’ story collides with truth

- How advisors can prepare clients for an uncertain retirement landscape

More Advisor NewsAnnuity News

- Cayman Islands premier to meet with U.S. reinsurance regulators

- Investigation finds deceptive sales, churning of annuities targeting postal workers

- Corebridge annuity sales slip ahead of Equitable marriage

- California teachers settle class-action lawsuit over in-plan annuity fees

- Jackson Financial CEO caps 40-year career with blockbuster Q2

More Annuity NewsHealth/Employee Benefits News

- Data on Managed Care Detailed by Researchers at Harvard Medical School (Geographic Access to Retinal Care in the United States): Managed Care

- New Hampshire fines Anthem and Matthew Thornton Health Plan

- $20M in long-term care money for WA immigrants to cover fewer than 200 people

- Arkansas Healthcare Providers Alarmed by Potential End of State's Medicaid Expansion

- Arizona, others sue feds over rule experts say cuts health care costs

More Health/Employee Benefits NewsLife Insurance News

- LIMRA: Individual life sales continue growth trend in Q2, led by whole life and VUL

- New York Life Awards 20 Golden Futures Scholarships, Expanding Student Support Through Financial Education and Career Development

- Built to Last: Winston-Salem—a quiet industrial powerhouse

- The silver economy ushers in a new era of life insurance growth

- Family communication: Financial planning’s growing blind spot

More Life Insurance News